|

Getting your Trinity Audio player ready...

|

Tim Sloan is stepping down immediately as Wells Fargo’s chief executive after struggling for two and a half years to contain scandals that led to public criticism by US bank regulators and calls in Congress for his departure.

Mr Sloan, 58, who will officially retire from the bank in June, will be replaced on an interim basis by the bank’s general counsel, C Allen Parker, who joined Wells in March 2017 after leading the Wall Street law firm Cravath Swaine & Moore.

Mr Sloan’s exit came only hours after the San Francisco-based bank’s largest shareholder, Warren Buffett, had expressed support for him in a television interview following widespread rumours Mr Sloan would be replaced.

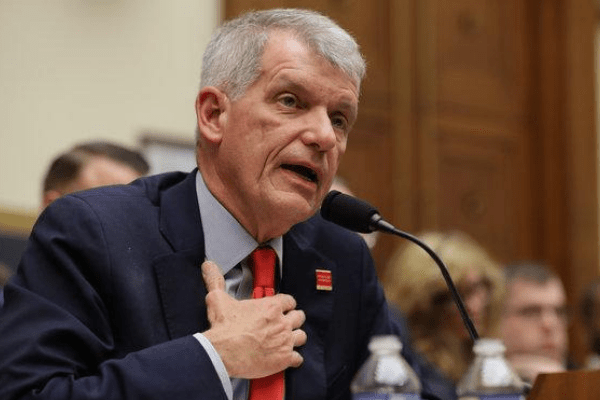

Only weeks before, Mr Sloan had faced withering criticism during an appearance before a committee of the US House of Representatives, and the Office of the Comptroller of the Currency expressed its “disappointment” with Wells’ “performance under our consent orders and its inability to execute effective corporate governance”.

In a call with analysts on Thursday, Mr Sloan said: “I’m confident in my ability to lead the work that needs to be done [but] it has become apparent that my presence has become a distraction.”

Elizabeth Warren, the Massachusetts senator and Democratic presidential candidate who has repeatedly called for Mr Sloan to be replaced by a leader from outside the bank, reacted to his departure by tweeting: “About damn time. Tim Sloan should have been fired a long time ago.”

Betsy Duke, the bank’s chair, said the next leader of Wells would come from outside the bank. “The board has concluded that seeking someone from the outside is the most effective way to complete the transformation at Wells Fargo,” she said.

Wells shares rose nearly 3 per cent to more than $50 each during after-hours trading after the announcement. That compares with a high of almost $60 last year.

Mr Sloan, a 31-year veteran of Wells, became chief executive in 2016, succeeding another longtime executive of the bank, John Stumpf, who was forced out in the aftermath of biggest mis-selling scandal in the history of US retail banking.

Wells branch employees, working under an incentive scheme that rewarded them for selling additional products to customers, opened accounts without customer consent. The total number of fake accounts has not been conclusively established but the total could be as high as 3.5m, according to one estimate.

In 2018, the Federal Reserve, in an unprecedented move, capped the bank’s balance sheet at $2tn until it was satisfied adequate controls were in place. Wells also entered into consent orders with the Consumer Finance Protection Bureau and the OCC.

Despite replacing virtually all of the bank’s senior leadership and much of its board, and overhauling its compliance, incentive compensation and reporting systems, the bank under Mr Sloan has been hit with a series of additional scandals in its mortgage, auto insurance and wealth management divisions.

“Getting fired shouldn’t be the end of the story for Tim Sloan,” Ms Warren said on Twitter. “He shouldn’t get a golden parachute. He should be investigated by the SEC [Securities and Exchange Commission] and the DoJ [Department of Justice] for his role in all the Wells Fargo scams.”

Wells’ shares have risen just 8 per cent since Mr Sloan was appointed. During the same period, shares in rivals Bank of America and Citigroup have gained 70 per cent and 30 per cent, respectively, as US banks benefited from a strong economy.

Wells, however, struggled to increase deposits or loans at its formerly industry-leading rate after the scandal broke. Its investment banking unit has lost market share as new clients proved hard to win.

“Though I am disappointed to see him go, because I thought highly of him personally and professionally, you can’t say that it is a shock,” said Scott Siefers, an analyst at Sandler O’Neill. “There was such intense pressure from politicians and regulators. Ultimately the steady drip of bad news caught up with the bank.”

Mr Sloan has spent most of his career in Wells’ commercial banking division, rather than it the retail division where the fake accounts scandal originated. But the political and regulatory pressure on him rose nonetheless, particularly after Democrats took control of the House in last November’s midterm elections.

Last month, Mr Sloan was repeatedly cut off as he tried to speak at a hearing of the House financial services committee. The chair of the panel, Maxine Waters of California, said: “He doesn’t get it.”