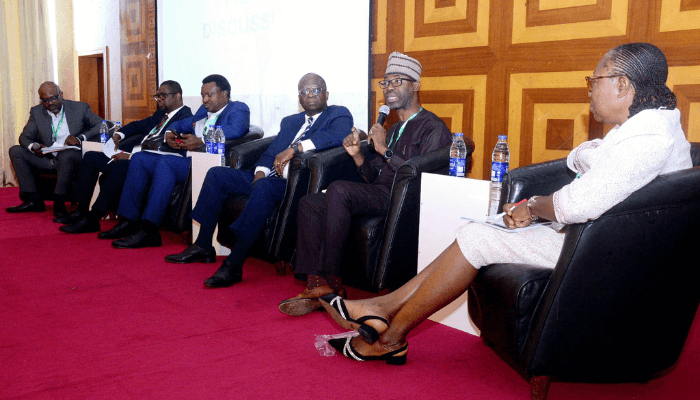

Stransact Chartered Accountants, in collaboration with the Nigeria Revenue Service (NRS), on Wednesday, enlightened corporate taxpayers and business owners on how to navigate Nigeria’s new tax landscape.

At a one-day seminar/workshop for corporate taxpayers and business owners held in Lagos with the theme, “Navigating Nigeria’s New Tax Landscape: Understanding the 2025 Tax Reform Acts and Mandatory E-Invoicing for Taxpayers”, speakers also deep-dived into the 2025 Tax Reform Act, looking at key changes and implications.

The event, which has over 250 physical and virtual participants, offered opportunity for networking. Stransact Chartered Accountants is one of Nigeria’s leading audit, tax, and consulting services firms. Its strong affiliation with RSM International, one of the largest global networks of accounting firms, gives Stransact access to the resources of a network of 64,000 employees in 120 countries.

In furtherance of improving revenue generation and making Nigeria more investor-friendly, President Bola Ahmed Tinubu, on June 26, 2025, signed into law four tax bills passed by the National Assembly. These include the Nigeria Tax Act (NTA), the Nigeria Tax Administration Act (NTAA), the Nigeria Revenue Service (Establishment) Act (NRSA), and the Joint Revenue Board (Establishment) Act (JRBA).

Read also: Tax Administration in Nigeria – A review of the 2025 Nigerian tax reform laws

The Tax Laws aim to simplify tax collection, reduce the tax burden on compliant businesses, and reposition the country as a more attractive investment hub, while boosting revenue through a wider and fairer tax net.

While the effective date of the Tax Laws is set for January 1, 2026, seminars/workshops like offered opportunity for participants to look at key changes and implications.

“The event opened my eyes to reliefs that come with the new tax laws, as HR manager, I have learnt of the rent relief, some on mortgages, and I can sensitise my colleagues on them and they can earn more when the law comes into effect,” said Ifeanyi Ndukwe, HR specialist at Lekoil.

Also at the event, the three-session panellists discussed: Mandatory E-Invoicing: Understanding the FIRS Electronic Fiscal System (EFS) and Merchant Buyer Solution (FIRSMBS); 2025 Tax Reform Act: Navigating Compliance Challenges and Future Outlook; and Practical Aspects of E-Invoicing Compliance: Integration, Data, Requirements, and Transaction Models.

In a major transformation of digital tax administration, the Federal Inland Revenue Service (FIRS) recently commenced an electronic invoicing solution (e-invoicing) aimed at revolutionising tax payment in the country. The e-invoicing system, also known as the Merchant-Buyer Model, is aimed at making tax compliance easier, faster and more transparent for all categories of taxpayers.

In less than two weeks of the initiative going live, no fewer than 1, 000 companies, representing 20 percent of over 5, 000 eligible firms, have so far embraced the solution and commenced integration with FIRS MBS platform.

The e-invoicing solution went live on 1 August, following a successful pilot phase which began in November 2024.

Large taxpayers, which are companies with an annual turnover of N5billion and more, are expected to be the first to be onboarded on the platform. The remaining large taxpayers are expected to come on board on or before November 1, which is the deadline for all the firms in the category to finalise their onboarding and integration processes.

During one of the panellists’ sessions, they noted that the 30 percent fund required by the new tax law to be deposited in a Nigerian bank escrow account is no additional cost for oil and gas companies, but to ensure the funds are kept.

Read also: 99% of informal sector in Enugu don’t remit taxes- Govt

“The extra cost is just a misconception in my own opinion, the new law is to ensure that 30 percent of the fund is kept with a Nigerian bank which can develop our country,” Gabriel Ogunjemilusi, former FIRS director.

He explained that the 30 percent is from existing funds mostly kept in foreign escrow accounts by the companies.

Under the new tax law, decommissioning/abandonment costs are deductible only if at least 30 percent of the fund is deposited in escrow with an accredited Nigerian bank.

In the Petroleum Industry Act 2021, the establishment of a Decommissioning Fund was enacted.

Operators are obligated to establish a dedicated Decommissioning and Abandonment Fund with an independent financial institution. The purpose of this fund is to ensure that sufficient resources are available exclusively for decommissioning activities in Nigeria.

“It was assumed that they could take it offshore. So, all of them then that way the law is given, making them make provision and take the money offshore and keep it in other countries’ banking sectors,” Ogunjemilusi said.

As Nigeria currently experiences a wave of divestments by international oil companies (IOCs), increased attention is being directed towards the decommissioning of ageing infrastructure.

“The PIA already provided that it should be funded, but by insisting on Nigerian banks, you are able to trace if it’s actually been funded. And in practice, many Nigerian players who are now predominant are struggling to fund it,” Kehinde Kajesumo, deputy director, head treaties & international tax policy, FIRS said.

Kajesumo explained that the law is to ensure the security of the environment of oil production, and also to ensure that the money will be available when it is needed in the future.

Read also: Tax reform to address challenges in informal sector, increase compliance – Coker

Also, discussions on the rent relief of 20 percent of annual rent paid, subject to a maximum of N500,000, sparked questions on who gets it between married couples who pay rent together.

Kajesumo said that the FIRS will provide more clarity on the rent relief provision, including how it applies when couples jointly pay rent.

The seminar workshop was set up for corporate taxpayers and businesses to enlighten them on how to navigate the new Nigerian tax laws.

Committed to helping its clients create value in their transactions, the growing professional services firm which is part of a global organisation, RSM International, specialises in delivering tailored financial consulting solutions that drive success and foster growth.

Stransact Chartered Accountants team of experienced professionals provides a full suite of services in audit & assurance, tax and consulting, with insights and strategies that meet the demands of today’s dynamic financial landscape.