|

Getting your Trinity Audio player ready...

|

Nigeria often speaks about growth, as most emerging economies would, but are we really growing as we ought to? That’s the million-dollar question. We debate interest rates, inflation figures, exchange rate volatility, and fiscal deficits as key determinants of growth. These are important conversations to explore. But beneath them sits a quieter problem, one we rarely name with urgency: unrecovered debt.

Not disputed debt. Not restructured debt. Not loans under active engagement. I am speaking of silent defaults that remained unrecovered. Obligations that simply fade into the background. No repayment. No resolution. No accountability. Just silence, fading into complete oblivion.

In many economies, silence is not neutral. It is corrosive.

Unrecovered debt is not a private inconvenience between a lender and a borrower. It is an economic leak, a huge loss and a saboteur to any system. Left unattended, it drains trust from markets, weakens institutions, and quietly strangles productive capacity. The damage does not announce itself with headlines. It shows up months later, after it has eaten into the fabrics of the system, through tighter credit, stalled expansion plans, delayed salaries, and jobs that never get created.

The hidden cost of silence

Every unrecovered obligation sits somewhere on a balance sheet, distorting reality. For banks, it inflates non-performing loans (NPLs) and forces conservative lending behaviour, and large provisions are made for these NPLs, reducing the capital available to fund the real sector and depriving customers of this financial support. For businesses, it freezes cash flow that should have been reinvested into operations, staff, and growth. For investors, it introduces uncertainty that cannot be priced accurately.

According to the Central Bank of Nigeria, credit to the private sector remains shallow relative to GDP when compared with peer economies. Whilst macroeconomic factors are often blamed, the micro-foundation of this problem is trust. Capital flows where financial obligations are honoured or, at a minimum, resolved.

When debts go unrecovered, lenders respond rationally. They raise collateral requirements. They shorten tenors. They increase pricing due to an increase in risk factors seen in borrowers’ behaviours. Small and medium enterprises, which already operate on thin margins, are the first casualties, as they are unable to absorb these huge costs into their operations. This pattern is well documented in development finance literature and echoed by institutions such as the World Bank and the International Monetary Finance Corporation in their assessments of emerging markets.

The irony is that the economy pays twice: first, through the default itself, and then through the contraction of credit that follows.

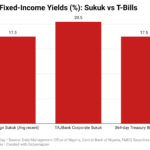

Comparative Analysis of Non-Performing Loans (NPLs) – FUGAZ Banks (Q3 2025)

Why unresolved debt is worse than disputed debt

There is a misconception that debt recovery is inherently hostile. In truth, the most dangerous situation is not conflict but disengagement.

A disputed obligation still implies dialogue. It suggests records are being examined, positions clarified, and outcomes negotiated. Silence, however, signals abandonment of responsibility. It removes the moral and legal anchors that keep financial systems functioning. In jurisdictions with strong credit cultures, unresolved debt is treated as an anomaly. It triggers processes and investigations. Structured recovery. Not because lenders are aggressive, but because the system itself values clarity, transparency and credibility.

Nigeria’s challenge is not that disputes occur. Disputes are natural in commerce. The challenge is that too many obligations drift into limbo, unchallenged and unresolved. Over time, this normalises default behaviour and punishes compliance. Research in institutional economics, from scholars like Douglas North, consistently shows that economies grow not merely on capital availability, but on enforcement mechanisms that make commitments credible. Without enforcement, contracts lose meaning.

Debt recovery as economic hygiene

We need to reframe debt recovery, not as punishment, but as sanitisation of a messy system – hygiene.

Just as audits keep organisations honest and procurement rules reduce waste, recovery processes keep markets clean. They ensure that access to credit remains tied to responsibility. They protect compliant borrowers from subsidising defaulters through higher costs of borrowing, especially those in the real sector who cannot afford the lower rates extended to blue-chip companies.

In many mature economies, debt recovery operates quietly alongside risk management, compliance, and corporate governance. It is not performative. It is procedural. It is designed to restore flow, not create spectacle.

Nigeria’s financial system has made progress in regulation and supervision, especially in recent times. Institutions like the Asset Management Corporation of Nigeria (AMCON) exist precisely because unresolved debt, when allowed to accumulate, becomes a systemic threat and hinders banks from performing their lending obligations to customers. The lesson from that experience is clear: ignoring defaults does not make them disappear. It merely transfers the cost to the broader economy, mainly the real sector.

The governance gap we rarely discuss

One of the least discussed aspects of unrecovered debt is its governance implications. Persistent default often signals deeper issues: weak internal controls, related-party abuse, diversion of funds, or poor corporate discipline.

When financial obligations are not pursued, these underlying failures remain hidden. Boards are not challenged. Management behaviour is not corrected. Borrowers use the court to delay sound justice due to the weakened judicial system in Nigeria. The same patterns repeat, often across multiple institutions.

From a corporate governance perspective, recovery is feedback. It tells the truth about how capital is deployed and whether or not stewardship obligations are being honoured. This is why serious recovery work often requires strategic private investigation, documentation, and legal clarity, not just demand letters.

The OECD Principles of Corporate Governance emphasise accountability, transparency, and responsibility. These principles cannot coexist with a culture of silent default.

Where institutional recovery fits in

Every system requires accountable institutions to ensure recovery is achieved timely and efficiently. This is where structured recovery institutions matter.

In functional economies, recovery is not outsourced chaos. It is handled by disciplined actors who understand law, finance, investigation, and negotiation. Their role is to restore equilibrium, not escalate conflict.

In Nigeria, firms like KREENO Consortium, representing the private sector-driven model, similar to AMCON in the public sector, represent a shift toward this institutional model. By combining debt recovery with private investigation and corporate governance advisory, this approach recognises a simple truth: many defaults are not purely financial problems. They are also fundamental organisational failures and misalignments.

When recovery is done properly, it clarifies facts, separates inability from unwillingness, and creates pathways for resolution that preserve value where possible and foster relationships. This is not aggression. It is system maintenance.

Why this matters now

Nigeria is at a moment where every unit of capital must work harder and optimally. Public finances are stretched. Businesses are adjusting to new realities. Investors are now more cautious. In such an environment, allowing capital to remain trapped in unrecovered obligations is not just inefficient; it is irresponsible. Growth cannot be financed on optimism alone. It requires discipline.

Countries that rebuilt after suffering financial crises did so by restoring trust in the system and thereby contracts. An example is South Korea after the Asian Financial Crisis. The United States after the savings and loan crisis. In each case, recovery mechanisms were strengthened, not softened, and confidence in the system was restored.

“The lesson is consistent: economies do not heal by avoiding hard conversations. They heal by resolving them.” Dr Ohio O. Ojeagbase of KREENO Debt Recovery.

Restoring flow, not assigning blame

The objective of recovery should never be humiliation. It should be a resolution.

When financial obligations are clarified and settled, relationships can reset. Credit can flow again. Businesses can plan with confidence. Jobs can be created on stable foundations. Nigeria does not suffer from a lack of entrepreneurial energy. It suffers from broken loops. Money goes out but does not return. Trust is totally eroded with friendship destroyed but not restored.

Until we treat unrecovered debt as a macroeconomic issue, not a private dispute, we will continue to chase growth whilst bleeding quietly underneath. The work ahead is not glamorous. It is procedural. It requires records, patience, firmness, and integrity. But it is necessary. Because economies do not collapse only from shocks. Sometimes they weaken because too many promises were left unresolved, and silence was mistaken for peace.

For more information, clarifications and support, contact Prof. Prisca Ndu on +234 902 148 8737 or priscan@kreenoholdings.com.