From inside its grey corporate headquarters in Aschheim outside Munich, Wirecard projects an image of one of Germany’s leading business success stories, a fintech champion to rival software giant SAP. After a decade of breakneck growth, Wirecard has become a favourite among investors, with a market capitalisation greater than Deutsche Bank, placing the company in the prestigious Dax 30 index.

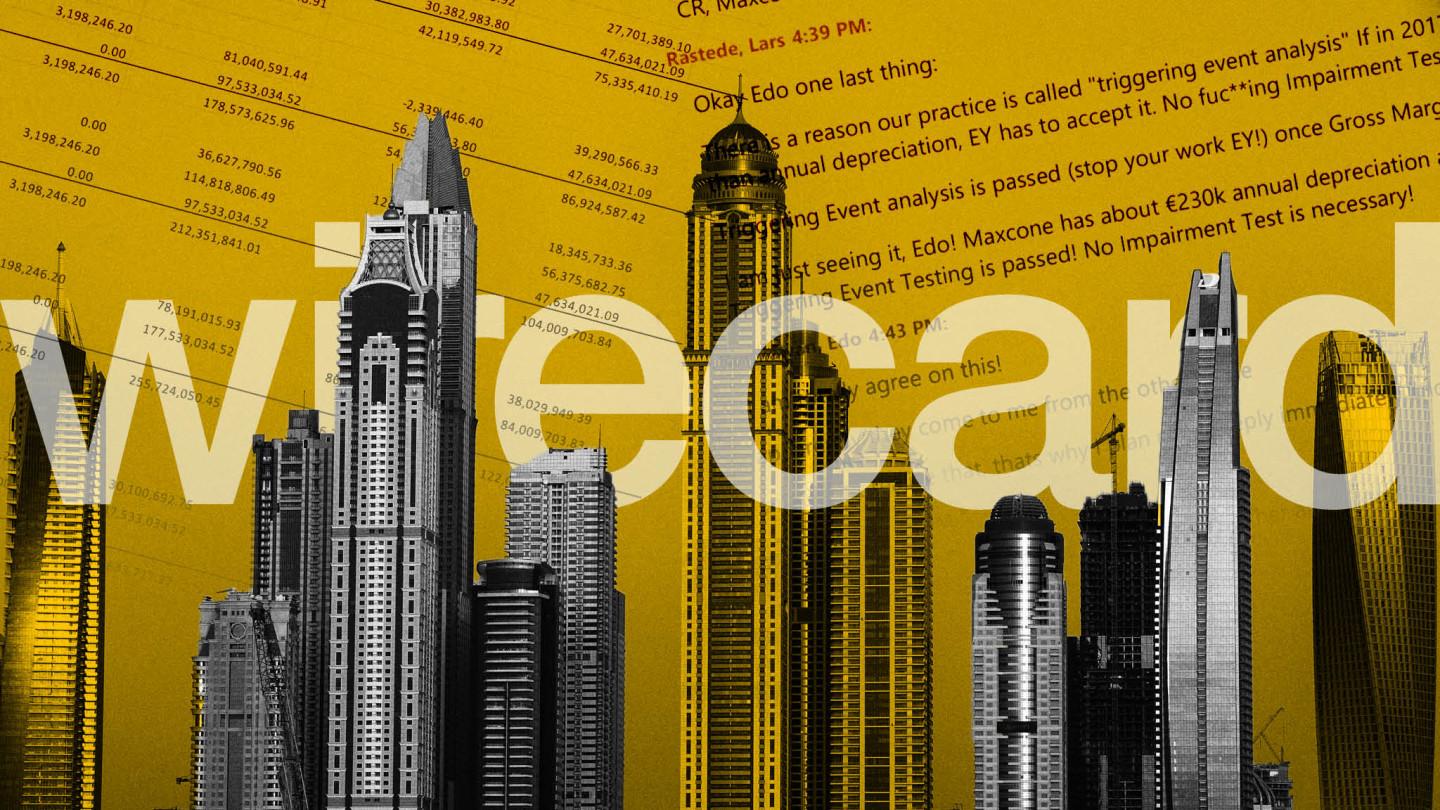

Yet Wirecard’s seemingly irresistible rise has been plagued by intermittent controversy about its accounting and business practices. Earlier this year, white-collar crime investigators raided Wirecard’s offices in Singapore multiple times in connection with allegations that sales and profits were invented at numerous subsidiaries across Asia. Edo Kurniawan, the company’s head of international reporting, was named among six suspects.

In response, Markus Braun, Wirecard’s Austrian chief executive, dismissed the problems as a local difficulty with scant financial impact. He blamed the payment processing company’s fast growth and outlined a dozen measures to improve compliance, including the appointment of a new chairman of the supervisory board in 2020. Wirecard’s stock price, which initially fell 40 per cent to €97, has since recovered to about €140, giving it a €17bn market capitalisation.

Today, the Financial Times is publishing documents which cast further doubt on Wirecard’s accounting practices. Internal company spreadsheets, along with related correspondence between senior members of Wirecard’s finance team, appear to indicate a concerted effort to fraudulently inflate sales and profits at Wirecard businesses in Dubai and Ireland, as well as to potentially mislead EY, Wirecard’s tier-one auditor.

The decision to publish these documents follows repeated charges by Wirecard that the FT is relying on fake material and that its own journalism is corrupt and suspect. The documents, provided by whistleblowers, give the clearest picture to date of Wirecard’s questionable accounting practices and business model.

In its defence, Wirecard has claimed that FT reporters have facilitated market manipulation in collusion with short sellers. These allegations have been widely circulated in the German media and are the subject of a legal complaint in Germany, an investigation by Bafin, the German financial regulator, and a probe by prosecutors in Munich.

The FT categorically rejects Wirecard’s allegations on all counts. A recently concluded two-month review conducted by an external law firm, RPC, found no evidence of collusion between FT reporters and market participants.

Established in 1999, Wirecard has been a pioneer in the processing of digital payments. In Germany, where consumers prefer to pay in cash, it caught the imagination of investors looking for a blue-chip European digital champion to match those in Silicon Valley.

Initially known for processing payments for online gambling markets and porn sites, Wirecard purchased a bank in 2006 and evolved into a full-service payments operation, providing the software and systems to plug online businesses into the global financial system.

With trillions of dollars of transactions up for grabs as consumers abandon cash, Wirecard is jostling with giant rivals such as Vantiv in the US and China’s Alipay for a share of the fast-growing market. It says it processed €125bn in transactions last year, a rise of 37 per cent. It is projecting 40 per cent growth in underlying earnings this year.

Over the past decade Wirecard has fuelled its expansion by buying smaller payment processing businesses and groups of customers around the world, including a 2017 move to take on 20,000 merchant clients of Citibank, spread over 11 Asia-pacific countries. The deal was intended to make the company a household name across the region.

Wirecard has also said its geographic reach has expanded by working with hundreds of partner processing companies, which fill in gaps when Wirecard lacks the expertise or local authorisation to process payments itself.

A focal point of the FT’S inquiries into Wirecard is one of these partner companies, a Dubai-based intermediary called Al Alam Solutions, which documents indicate contributed half of the German company’s worldwide profits in 2016.

Wirecard staff have described Al Alam as a “third-party acquirer”, payments jargon for a business licensed by the big payment networks, such as Visa and Mastercard, to help retailers accept credit card transactions. Al Alam was purportedly the spider at the heart of an international web, processing vast sums for 34 of Wirecard’s most important and lucrative clients in the US, Europe, Middle East, Russia and Japan.

Yet when the FT visited Al Alam’s Dubai office this year it became clear this was a threadbare operation. A former employee told the FT it had just six or seven staff.

Neither Visa nor Mastercard have any record of a relationship with Al Alam, deepening the mystery of why Wirecard would refer business to the partner company, given the German fintech group already has Wirecard Processing, its own payment processing subsidiary employing scores of staff, nearby in Dubai.

Internal financial reports from 2016 and 2017, shared between members of Wirecard’s finance team and obtained by the FT, detail the business which has supposedly flowed through Al Alam. The documents record about €350m of payments from 34 key clients as passing through Al Alam, on behalf of Wirecard, each month during the period.