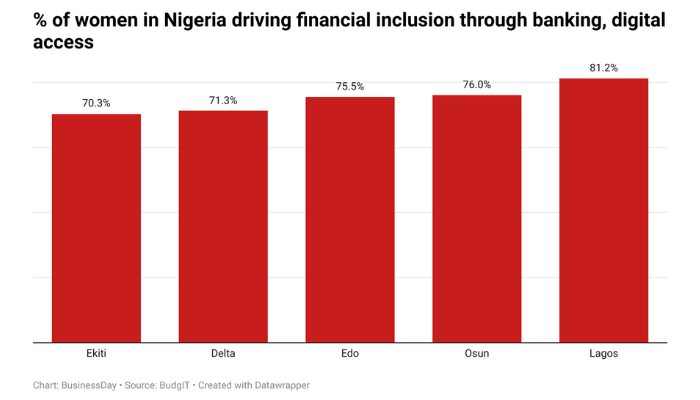

The model of Microfinance banking involves the provision of financial services to the poor and low-income earners. It is also a vehicle for the financial inclusion of a large number of people who operate in the informal sector of the economy. This makes micro-finance banks critical elements in the financial inclusion of the poor.

However, microfinance banks thrive more in times of economic growth. They are not like businesses that thrive in times of austerity. They deal with the poor. They are engaged in a battle with poverty. So anything that accentuates poverty weakens these banks. The current recession and stagflation are having an adverse effect on these banks and putting them under extreme pressure.

When the going gets tough, loan repayments become difficult and delinquency will escalate and bad loans will mount, creating huge problems for the banks and their customers alike. In August 2016, the Central Bank Governor, Godwin Emefiele announced that non-performing loans (NPLs) in the banking sector rose by 78 percent year-on-year to N649.63 billion. Generally, non-performing loans in the banking system have been put at 20 percent as against a best practice threshold of under 5 percent.┬Ā If this is the situation with the deposit money banks, with all their machinery for loan processing, disbursement and management, then one can only imagine how terrible microfinance banks are faring. It is therefore not unlikely that some of these banks may begin to take panic measures and apply stringent loans and recovery measures that may worsen the plight of the industry, the poor and very small businesses and entrepreneurs, and ultimately, harm efforts to ensure financial inclusion of the unbanked in Nigeria.

Even in normal times, micro-finance banks in Nigeria put high and sometimes unscalable barriers before their customers could access loans, usually at very high-interest rates. That worsened with the economic recession. Although we are gradually exiting the recession, the business outlook is still not rosy and the banking industry is still groaning under the weight of non-performing loans. The result is that only very few people can now access loans from microfinance banks as they demand collaterals in forms of land, vehicles, and even house items and electronics.