Nigeria fought hard to break free from the chains of slavery and colonial rule. Gaining independence was supposed to mean freedom, the power to make our own choices and build a future on our own terms.

But today, Nigeria finds itself caught in a new kind of trap. This time, there are no visible chains, just heavy debts to foreign lenders, tough repayment terms, and growing dependence on outside help to keep the economy afloat.

This is what many now call the ŌĆ£slavery paradoxŌĆØ: a situation where, despite being politically free, a country remains economically tied down by foreign influence, not through force, but through financial pressure.

Read also:┬ĀFederal Government Loan: 7 Easy Steps to Apply

In place of colonial masters, we now have creditors. And instead of being told what to do by foreign rulers, weŌĆÖre often left with little choice but to follow the conditions set by international lenders and financial institutions.

The challenge now is to break this new cycle to build a stronger, more self-reliant economy that doesnŌĆÖt depend on borrowing to survive.

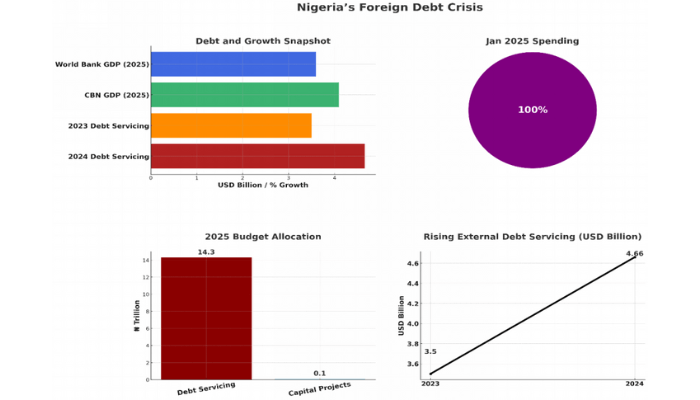

Recent fiscal data paints a stark picture. As of September 2024, NigeriaŌĆÖs external debt soared to $43 billion ŌĆō the highest since the countryŌĆÖs celebrated debt relief in 2006.

The 2025 national budget allocates a staggering Ōé”14.3 trillion to debt servicing, an amount that overshadows capital expenditure and signals the extent to which debt repayments are crowding out critical investments in infrastructure, education, and healthcare.

In January 2025 alone, the entire Ōé”696 billion spent by the federal government went to debt servicing, leaving nothing for capital projects. This trend is not just alarming; it is unsustainable.

The fiscal strain is exacerbated by the sharp depreciation of the naira. Although Nigeria completed principal repayment on a $3.4 billion IMF loan in April 2025, the local currency cost of external debt has doubled, making repayments ever more burdensome.

ŌĆ£While external borrowing, in theory, can stimulate growth if channelled into productive investments, NigeriaŌĆÖs current pattern of borrowing has failed to generate the transformative impact needed.ŌĆØ

In 2024, external debt servicing reached $4.66 billion, up from $3.5 billion the previous year, with multilateral creditors accounting for the majority. This growing debt burden is undermining the governmentŌĆÖs capacity to respond to urgent developmental needs, as more revenue is diverted to service past loans rather than build the future.

Read also:┬ĀNigeria fully repays $3.4bn IMF loan ŌĆō Minister

Economic growth projections remain modest. The Central Bank of Nigeria forecasts GDP growth of 4.1 percent in 2025, but the World Bank offers a more cautious estimate of 3.6 percent, citing persistent structural weaknesses and the drag of high debt servicing. While external borrowing, in theory, can stimulate growth if channelled into productive investments, NigeriaŌĆÖs current pattern of borrowing has failed to generate the transformative impact needed.

Inflation, particularly in food and energy, continues to erode household welfare, further limiting the benefits of any debt-financed development.

The slavery paradox is thus not merely a metaphor but a lived reality for millions of Nigerians. The countryŌĆÖs reliance on foreign loans to finance development has created a vicious cycle: as debt servicing consumes an ever-larger share of government revenue, the ability to invest in sectors that drive inclusive growth is diminished.

This pattern mirrors the extractive dynamics of the colonial and slave eras, where the fruits of local labour and resources were syphoned off to serve external interests.

To break this cycle, Nigeria must embrace a bold new policy direction. First, the government should prioritise domestic resource mobilisation by expanding the tax base, improving tax collection efficiency, and curbing illicit financial flows.

Second, borrowing should be strictly limited to projects with clear, measurable returns ŌĆō especially in infrastructure, agriculture, and technology ŌĆō that can generate the revenue needed to repay loans without mortgaging the countryŌĆÖs future.

Third, greater transparency and accountability must be enforced in both the negotiation and management of foreign loans, with regular public reporting and independent audits.

Read also:┬ĀSun King secures $80m naira-for-solar loan to power Nigerian homes

Fourth, Nigeria should actively pursue debt restructuring and renegotiation with creditors to extend maturities, lower interest rates, and create fiscal space for critical investments. Finally, the government must invest in human capital ŌĆō education, healthcare, and skills development ŌĆō to lay the foundation for sustainable, endogenous growth.

Only through such decisive reforms can Nigeria hope to escape the slavery paradox, reclaim its economic sovereignty, and build a future where the promise of independence is finally fulfilled for all its citizens.

┬Ā

Olajide Dahunsi is a Lecturer, Sustainability Advocate and Senior Fellow Higher Education Academy (SFHEA) in the UK. He specialises in accounting, finance, economics, entrepreneurship, and national development strategy.