It is clear that insurer’s return on equity are ebbing, with added pressure from low investment returns, and premium growth that is failing to keep pace with cost trends all impacting the profitability of the sector.

Additionally, the combinations of rising claims expenses brought on by the effect of pricing and exposure to the oil and gas and a low yield environment have contributed to slim margins.

For instance, insurers’ investment income gets a boost when yields on treasury bills are high, and such increases help augment underwriting income, further adding impetus to the bottom line.

Of course firms operate in tough and unpredictable macroeconomic environment, as lingering apathy toward insurance driven by religious and cultural beliefs, low purchasing power among consumers, and an economic lethargy continues to undermine growth.

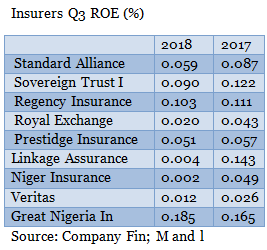

Markets and Intelligence data shows that the cumulative average return on equity of 19 largest listed insurers fell to 7.47 percent in September 2018 from 7.78 percent as at September 2017.

The Return on Equity ratio essentially measures the rate of return that the owners of common stock of a company receive on their shareholdings.

Return on equity signifies how good the company is in generating returns on the investment it received from its shareholders.

A higher ratio means a firm is efficient in utilizing owner’s assets in generating higher returns. On the other hand, a lower ratio could be a reflag that a firm has weak financial strength.

“Insurance is indeed the business of risks, lower return on equity could result in particular years, nonetheless some insurance companies have been able to posts higher ROE,” said an actuarial analysts, who doesn’t want his mentioned.

“That said most insurance companies’ poor governance structures, and this is seen in their poor results and poor decision making. The harsh operating environment affects insurance companies more than any other some other sectors. Insurance is sold, not bought. Insurance penetration is still very low here in Nigeria. Government as the biggest buyer is known to owe,” said the analyst.

Nonetheless the industry remains attractive to investors because it is in its embryonic stage, which means there are more room for people to take up a cover, albeit there has to be improvements in economic fundamentals- lower unemployment rates, low inflationary environment, and favourable foreign exchange environment.

Drilling down the figures shows some insurers have bucked the trend as they were able to grow return on equity while contemporaneously exceeding industry average.

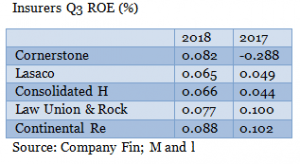

For instance, Consolidated Hall Mark Insurance’s return on equity increased to 6.58 percent as against 4.43 percent the previous year. This means for every N1 invested in the company investors get N6.58.

Lasaco Insurance’s return on equity rose to 6.48 percent in the period under review as against 4.91 percent the previous year while net income was up 35.25 percent in the same period.

Cornerstone insurance’s return on equity moved to 8.24 percent in September 2018 as against negative figure 0.28 percent the previous year as the company returned to profit in the period under review.

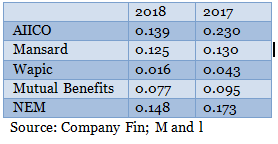

On the flip side, Aiico Insurance’s return on equity fell to 13.88 percent in September 2018 from 22.97 percent the previous while net income dipped by 24.80 percent same period.

Linkage Assurance return on equity reduced to 0.40 percent in the period under review from 14.31 percent as at September 2017 while net income dipped by 97.30 percent in the period under review.

Analysts say insurers will have to cut costs, introduce more innovative product to the market, and engage in fair pricing to remain efficient.