|

Getting your Trinity Audio player ready...

|

Nigeria’s upstream oil and gas companies Seplat and Oando are paying down their debt and creating a healthy balance sheet, giving them the leeway to approach banks for more loans and finance acquisitions of more fields.

A company finances its operation with a combination of debt (money borrowed from financial institution) and equity (money contributed by shareholders). But rising obligation could be a burden as it undermines earnings, which makes it a risky investment.

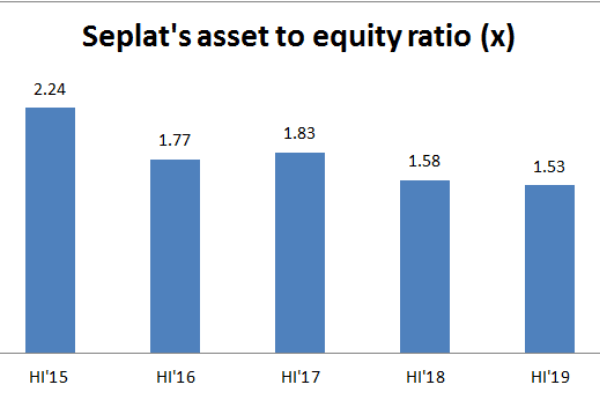

A five year industry average equity multiplier of asset which is a financial leverage ratio that measures the proportion of company’s asset that is financed by shareholders’ equity of Seplat and Oando is 2.60 times in June 2019, an improvement from 30.30 times recorded in 2015.

A lower equity multiplier implies Seplat and Oando are not incurring excessive debt to finance its assets. Instead, they issued stock to finance the purchase of assets they need to operate their business and improve their cash flows. It is calculated by dividing a company’s total asset value by total net equity.

Read also: Seplat targets top spot in Nigeria’s oil & gas with Eland acquisition

If a business has a high ratio, it is more susceptible to pricing attacks by competitors, since it must maintain high prices in order to generate the cash flow to pay for its debt.

Analysts attribute am improved equity ratio to aggressive cut in capital expenditure spend and sale of assets to bolster cash flow, and that financial institutions will be reluctant extending credit to a highly indebted entity with poor credit history.

“Beyond raising more equities, the Eland’s deal for Seplat is an indication of how strong the company have bounce back while the Market awaits what Oando next move,” Charles Akinbobola, energy researcher at Sofidam Capital.

Seplat and Oando have a combined cashflow from operating activities of N90.80 billion as at June 2019, little wonder they have the cause to acquire companies, settle obligation, and pay dividend.

Further analysis of equity ratio shows Seplat’s ratio was 1.53 times as at June 2019, from an all-time high of 2.24 times in 2015 which implies Seplat has raised substantial equity to remain in business.

The total bearing loans and borrowings in the books of Seplat fell by 21.45 percent to N136.87 billion as at June 2019, while finance cost dipped by 40 percent to N12.66 billion.

Recall, through a combination of cash and debt, Seplat Petroleum Development Plc announced a cash deal to acquire fellow London-listed independent exploration company Eland Oil & Gas for $484 million few days ago.

The acquisition of Eland oil and gas Exploration Company could raise Seplat’s oil production by 30 percent to about 64,000bpd by 2020 according to data from Bloomberg.

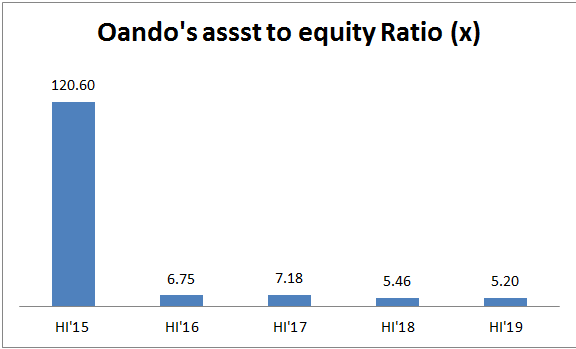

Similarly, Oando’s asset to equity ratio stood at 5.20 times in the period under review, from 120.60 times in 2015, when the external auditors raised concerns about its going concerns.

The major players in the upstream oil and gas industry were exposed to financial risk following the precipitous drop in crude oil price of mid 2014 that sent a shiver across the global market. A lot of them had borrowed money to acquire more fields before the volatile periods.

Seplat felt the pinch in 2016 when Forcados Terminal, which transports crude oil to pipelines – was vandalized by militants in the Niger Delta region while Oando had borrowed money to fund a $1.2 billion of Conoco Philip, a failed investment that exposed it to financial risk.

However, a rebound in crude oil price and a relative in the Niger Delta region was a boon to oil majors as cash flows began to improve, but they will have to drill more oil when all prices are high.