Africa’s venture capital market is undergoing a structural transition, as fresh data for the first nine months of 2025 points to a landscape where early-stage dealmaking is rebounding strongly while large, late-stage funding rounds continue to dry up.

The latest quarterly update from the African Private Capital Association (AVCA) shows a market finding its footing through volume rather than value, with start-up activity returning to pre-winter vibrancy even as cheques shrink at the upper tiers of the investment ladder.

Across the continent, investors closed 122 deals in Q3 2025, a 17 percent year-on-year jump, reinforcing the steady recovery that began earlier in the year. Cumulatively, Africa recorded 362 deals between January and September, a level closely aligned with the average seen across 2022–2024, signalling that investor appetite, particularly for Seed and Early-Stage ventures, has largely normalised after the downturn.

Yet beneath this resurgence lies a more complicated picture. Disclosed equity value fell sharply to $0.2 billion in Q3, compared with $0.6 billion apiece in the first two quarters of the year, bringing the total disclosed equity raised so far to $1.4 billion.

The report warns that the headline decline likely understates true activity because a significantly larger share of deals were undisclosed this quarter, reflecting greater investor caution and a preference for lower-visibility transactions.

Even with the subdued capital totals, the market is showing signs of qualitative resilience. The median equity deal size climbed to $3 million, a 20 percent rise compared to 2024. This suggests that while investors are writing fewer large cheques, they remain willing to back high-quality early-stage founders with stronger fundamentals and clearer paths to profitability. Seed deals are the clearest expression of this trend. By Q3, Africa had already recorded 107 Seed-stage transactions, representing 85 percent of 2024’s full-year total.

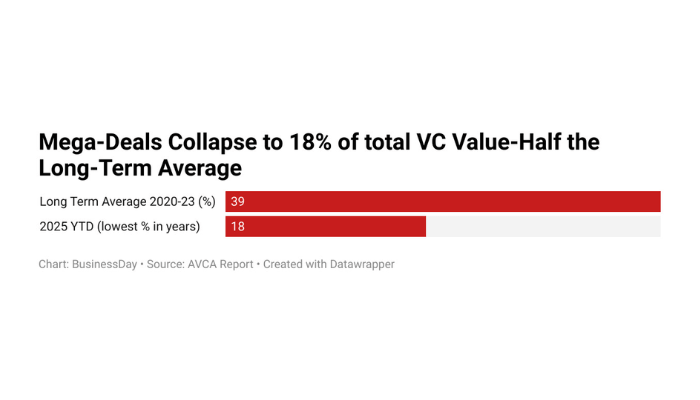

In contrast, late-stage investment has thinned to a trickle. Only two late-stage equity deals were recorded in the third quarter. Mega-deals, typically multi-country or pan-African expansions, have all but vanished from the landscape. Multi-region transactions now account for just 18 percent of total deal value, less than half their long-term average of 39 percent, underscoring how investors have shifted away from capital-intensive, scale-driven plays.

Read also: MTN Group’s service revenue rises 26% on Nigeria, Ghana growth

The geographic map of funding is also being redrawn. Southern Africa now leads the continent in funding value with a 26 percent share, overtaking traditional hotspots, while West Africa remains the most active region by volume. But smaller cheque sizes dominate this activity as the median deal in West Africa stands at $1.9 million, among the lowest across the continent.

Sectorally, the gravitational pull of fintech, long Africa’s engine of venture excitement, is weakening. Financials accounted for 31 percent of total value in 2025, down sharply from 59 percent in 2024. In their place, Industrials, Information Technology, and essential-economy sectors such as Consumer Staples, Energy, and Utilities have grown their collective footprint to nearly a fifth of total funding.

Investors appear to be prioritising predictable demand cycles, clearer margins, and infrastructure-driven plays that align with Africa’s economic fundamentals.

Another defining aspect of this emerging landscape is the lengthening gap between funding rounds, a shift that mirrors global reset trends but carries sharper implications for African ventures.

Data from Africa: The Big Deal latest report showed that data from post-2023 activity revealed the rapid fundraising cadence of the 2021–2022 boom, when start-ups moved from Pre-Seed to Seed in under a year—has now slowed considerably. Founders today are spending between two and three years advancing from one stage to the next, with Series A to Series B timelines stretching past 36 months. The slowdown reflects investor caution, tougher valuation expectations, and fewer active late-stage players, even as early-stage momentum remains comparatively strong.

Venture Debt Becomes Safety Net

If early-stage equity has kept Africa’s start-up pipeline alive, venture debt has become the shock absorber that is holding growth-stage companies together.

According to AVCA, venture debt financing has exploded to 55 deals worth $1.6 billion so far in 2025, already more than double the entire debt value recorded in 2024. Six debt megadeals alone contributed $1.1 billion, highlighting the extent to which lenders, not equity investors, are now supplying the bulk of expansion capital. The median debt ticket, at $7 million, is substantially higher than typical equity cheques this year.

This pivot to debt reflects a global shift in risk pricing, but it has particular resonance in African markets where founders often contend with currency volatility, rising operating costs, and limited local follow-on capital.

Venture debt offers a lifeline, preserving runway without forcing down valuations through dilutive rounds, but also introduces new risks. As AVCA notes, higher leverage could pressure cash flows in an environment where interest rates remain elevated and capital markets uncertain.

A New Normal Defined By Selectivity, Structure

Taken together, the trends point to a new normal in Africa’s venture ecosystem. More deals, smaller cheques, fewer late-stage bets, and a heavier reliance on structured financing. Investors are favouring disciplined growth, stronger business fundamentals, and clearer paths to revenue, a shift that, while painful for some scale-ups, may ultimately produce a more sustainable market.

For founders, the message is to diversify funding strategies early, build capital efficiency into product design, and prepare for more structured deals as venture debt cements its place in Africa’s financing architecture.