| Nigeria’s Sovereign Investment Authority (NSIA), operators of the Nigerian Sovereign Wealth Fund (the Fund), was created to protect oil wealth for the country’s posterity by being a ballast to fiscal volatility. However, information from the latest annual report show that the Fund may have rather become a costly bureaucracy and a masterclass in misallocation with operational costs ballooning amidst thinned earnings. Established in 2011 with a take-off grant of $1 billion, NSIA appears not in a rush to ramp up profits as Abuja’s unfettered resolve to always infuse capital holds.

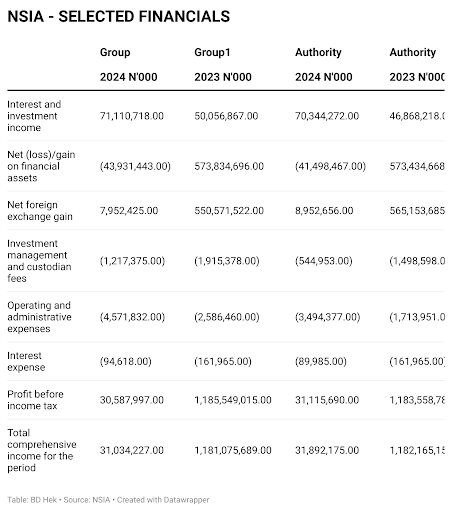

NSIA’s financial report for the First quarter ended March 31, 2025, reveals a troubling contradiction as staff and other personnel costs hiked while profits tumbled. Personnel costs jumped by 38.62 per cent from N1 billion to N1.39 billion and the cost incurred to service non-executive directors spiked by a whopping 444 per cent. Yet, profits were almost wiped out, crashing from N1.2 trillion to just N31 billion. Yet, the Petroleum Industry Act (PIA) gave it N247 billion in 2024 and the Government gave it a further N207 billion as Nigerian Government’s contributions leaped 33.65 per cent from N615 billion in March 2024 to N822 billion in March 2025. But despite subdued performance, managers of the Fund will still expect more capital injections from Abuja that is looking to stabilize finances and the Naira amidst burgeoned debt burdens that have exceeded 40 per cent of GDP. |

|

| NSIA’s performance picture becomes concerning from the efficiency view. ROA plunged by over 26 percentage points, from 26.81 per cent as March 2024 to 0.65 per cent as at March 2025 as profits failed to keep up pace with assets.

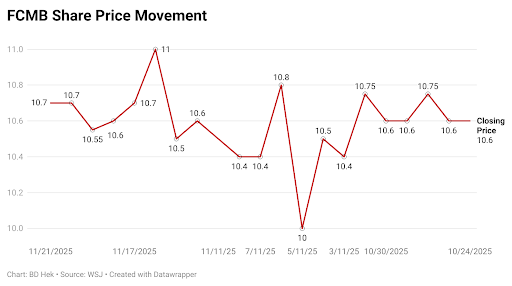

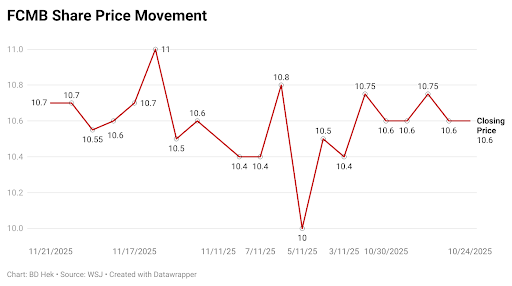

NSIA’s Stabilisation, Future Generations, and Infrastructure Funds now manage diversified portfolios that incorporate instruments ranging from Eurobonds to private equity, so overheads must be incurred, but not to the to the level of eclipsing asset returns and wasting value. Moreso, lavish spending within a fund designed for future generations, in a country where public sector wages are a sensitive political issue, poses optically horror and financial doubts. Analysts contend that NSIA’s mandate is valid, as the Fund has garnered over a trillion Naira in third-party investments and backing infrastructure like the Second Niger Bridge. But as oil revenues remain shaky and government debts rise, prodigal infusions mean subsidising inefficiency. Thus, Whilst NSIA totters on the profits track, it should maintain cost discipline or risk turning a supposed wealth guardian into a wealth raven. Dangote’s Delayed Debut: Retail Investor Fears and Market Opportunities The colossal 650,000 barrels per day refinery, the largest in Africa, and the 3-million-ton urea powerhouse had been slated for an initial public offering (IPO) early this year. Now, Dangote’s body and oral language says that none of this will happen until 2026. The reason is simple – the companies must ramp up operations and contain market volatility. But a greater reason borders on Dangote’s circumspect steps to unlocking value from his $19 billion refinery venture. Having revealed in October 2025 that he would sell between 5 per cent and 10 per cent of his present holding in the refinery on the NGX in one year, investors saw progress. For Dangote, the indicative valuation was enthusing as it would propel his value close to $100 billion. But this triggered grumblings that only HNIs and institutional investors will be invited to the full IPO match retail investors are relegated to spectators stands. Such exclusivity would leave a legion of crestfallen retail investors, who have come to see the refinery as not just a company, but as a heritage. Whilst managing a blockbuster listing is simpler with fat cheques from a few dozen investors, the rational is exclusionary. It violates the spirit of the new Investment and Securities Act (ISA) 2025, which seeks to democratise the capital market and capture more Nigerians in the formal financial system’s net. What is more, retail inclusion would allow the average citizen to have a real stake in Nigeria’s economic transformation where the market is deep and resilient. Thus, as we approach the corridors of 2026, investors and analysts will scrutinise how Dangote IPOs are allocated and how their valuations unfold. Nigeria’s capital market seeks must graduate from bouts of sporadic rallies to sustained development. Hence, its biggest listings must reflect national opportunities rather than elite fundraisings. It should lead Nigeria on its march to shed its image of entrenched inequality. This choice matters, much as does the refinery itself. FCMB’s N400 Billion Capital Scheme: A Warrant to Boom or a Test of The Market? FCMB holds an international banking licence that permits cross-border operations. Having already tugged in N144.6 billion from a 2024 public offer that was oversubscribed beyond its N110 billion mark, the bank had earlier planned to raise N150 billion. It later increased the capital raise size to N340 billion, then to N370 billion, and now N400 billion. This happened under 18 months, reflecting a frenetic drive across the bridge to N500 billion. Success of this gambit will allow the mid-tier lender to keep its international licence and retain its cross-border business; failure will herald a downgrade that will humble its operational scope, curtail its ambitions, signal weakness, and ultimately diminish its stature in the competitive arena. |

|

| The bank’s voyage reflects a broader banking overhaul in Africa’s leading economy, where regulatory reforms by the central bank seek to bolster the sector against economic shocks. Global rating agency Fitch says that most leading banks like Zenith and Access are on course, diminishing the prospect of forced mergers, while mid-tier banks like FCMB and Fidelity face craggy hurdles, requiring bigger injections. The economy will be the biggest beneficiary of banking recapitalisation success. Deeper capital could stimulate increased credit to vital sectors with the potential to make the $1 trillion economy dream of the present administration a reality.

The size of the venture will test investor appetite in an unstable economic weather. Management, led by Group Chief Executive Ladi Balogun, peddles a tale of strength and future foray into fintech and new markets. Investors are cautious, rightly questioning whether the frequent visits to the equity fountain evidence ambitious planning or a lack of it. Thus, a wave of earnings per share dilution spooks the process, but success of the offer will be a critical gauge of confidence.

Overall, the shade of the ultimate judgment will depend on the bank’s capacity to deploy the new capital efficiently. If it lifts cent return on equity from the miserable 0.16 per cent to industry-wide levels, the dilution will be tolerable. otherwise, it will tell cautionary tale of overshoot. |