|

Getting your Trinity Audio player ready...

|

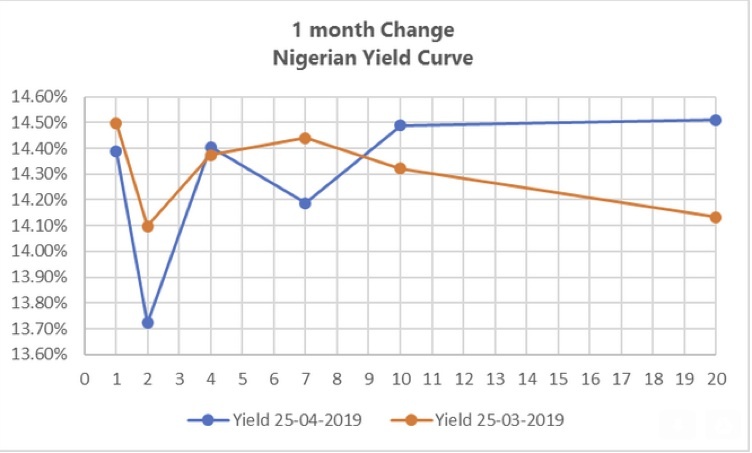

Nigerians can breathe easy as a key economic metric of impending recession lessened with the long-term vs short term yield environment in the country transitioning from an inverted yield curve after the recently concluded OMO auction.

A month ago, yields on long-term debt notes issued by the Federal Government of Nigeria where lower than the yields on short-term maturities but with the new market closing rates after the OMO auction last week Thursday, the inversion of the yield curve turned to normal convexity.

Obinna Uzoma, a Lagos based economist told BusinessDay that “the economy is looking good as threats to the financial position of Nigeria weakens on higher crude oil prices and a direct policy implementation path. Political opposition has also been quiet which gives a general sense of calm and confidence for investors who tend to take long term bets on countries.”

The yield on the most sought-after short-term maturity, the 12 months treasury bills, declined to 14.3 percent from 14.49 percent last month while the longer term 10-year and 20-year bonds improved from 14.32 percent to 14.48 percent and 14.13 percent to 14.51 percent respectively.

An inverted yield curve is an interest rate environment in which long-term debt instruments have a lower yield than short-term debt instruments of the same credit quality. This type of yield curve is the rarest of the three main curve types and is considered to be a predictor of economic recession.

Although the yield curve is still inverted in short term maturities with the 2-year FGN bond rate 66.7 basis points below the 12-month treasury bills, the outlook on economy is trending upwards as crude oil prices and GDP forecast of the IMF portends that the economy is out of the likelihood of another recession.

Ifeanyi John