Nigerian banks were the exception to soaring bad loans and declining profits at African banks in 2020 when the COVID-19 pandemic brought widespread economic disruption to the continent.

The financial reports of the 15 largest banks in South Africa, Nigeria, Kenya and Morocco analysed by global credit ratings agency, MoodyŌĆÖs, show nonperforming loans (NPLs) at most African banks surpassed their 10-year averages in 2020 while profits slumped.

KenyaŌĆÖs three largest banks, Co-operative, Equity and KCB, recorded the sharpest rise in NPLs, up 345 basis points to 12.5 percent of total loans.

The deterioration in loan performance was more moderate among South AfricaŌĆÖs four largest banks- ABSA, First Rand, Nedbank and Standard Bank, which recorded a combined rise of 193 basis points. Same for MoroccoŌĆÖs three largest banks ŌĆō Attijariwafa, Bank of Africa and GBCP, which recorded a combined rise of 90 bps.

Read Also:┬ĀBanksŌĆÖ cheap funds donŌĆÖt reflect in loans to customers

In Nigeria, however, the NPL ratio of the five largest banks, which include Access, Guaranty Trust Bank, Zenith, United Bank for Africa and First Bank, fell by 81 basis points as widespread loan restructuring masked loan deterioration.

Outlook for 2021

Analysts at MoodyŌĆÖs however expect NPLs in Nigeria to rise in the months ahead and NPL ratios to remain above their 10-year averages in Kenya, South Africa and Morocco.

The analysts also expect a partial recovery in profitability over the next 12-18 months for African banks that have suffered a decline in profits.

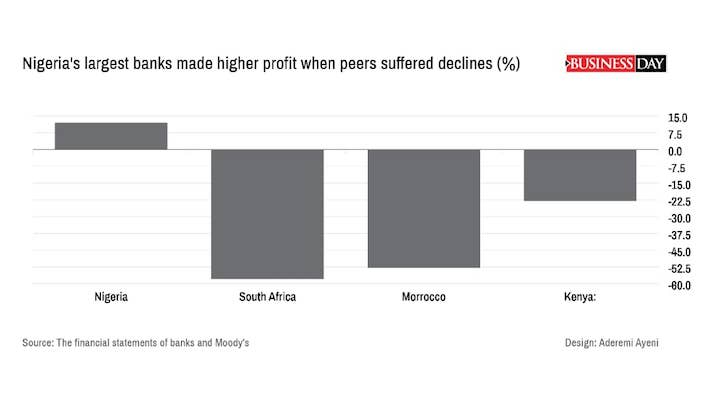

Barring Nigeria, profitability collapsed at most banks, mainly because of an unprecedented increase in provisions.

South African banksŌĆÖ profits fell by 58% in 2020 and return on assets (ROA) was below its 2010-2019 low. For Morrocan banks, profits dipped 53%.

Profitability at Kenyan banks declined by 23%, although average ROA remained the highest at 2.2%. Lower provisioning meant profits increased by 12 percent at Nigerian banks.

MoodyŌĆÖs analysts however expect lower provisions in South Africa, Kenya and Morocco to boost profitability this year, although provisioning costs will remain higher than their 10-year averages.

For Nigerian banks, the outlook is different.

The analysts expect provisioning costs to increase towards their long-term averages as bad loans increase and require more provisions.

ŌĆ£This will pressure profitability, although a recovery in government bond yields this year will support banksŌĆÖ pre- provision income and enhance their ability to absorb loan losses,ŌĆØ the analysts said.

The ROA of NigeriaŌĆÖs largest banks is also forecast to fall as provisions increase towards 2.0% of gross loans.