Nigeria is placed among the top nations with the least conducive environment for financial inclusion, the Economist Intelligence Unit’s (EUI) 2019 Global Microscope revealed. This is coming seven years after adoption of the National Financial Inclusion Strategy (NFIS).

Africa’s most populous nation performed poorly in the survey even though the overall enabling environment for financial inclusion improved globally, according to the financial inclusion report released Thursday.

The largest economy in Africa scored lower than the war-torn Parkistan (55). Out of 100 points, Nigeria scored 43 points; this is 23.21 percent lower than the 56 points it reported in 2018.

“Nigeria experienced the largest score decrease in the 2019 Microscope, in the Government and Policy Support domain. Its scores also decreased in the Consumer Protection domain and the Products and Outlets domain,” the report read.

BusinessDay analysis of the EUI report revealed that the 43 points score reported by Africa’s most populous nation was also lower than the 48.2 points it recorded in 2013, almost the same time the NFIS was adopted.

After seven years of policy drive by the Central Bank of Nigeria (CBN), the 2019 EUI report hinted that the regulator may not have achieved as much as it expected.

The Central Bank adopted the NFIS in 2012. The strategy was launched to reduce the percentage of adult Nigerians who do not have access to financial services from 46.3 percent in 2010 to 20 percent in 2020. Also, the strategy stipulates that 70 percent of those to be included in the financial system by 2020 should be in the formal sector.

“Though financial inclusion numbers improved in 2018, effective implementation of the strategy (NFIS) was constrained as it did not give room for innovation and changes in the financial services landscape,” the apex bank said in the 2019 NFIS annual report.

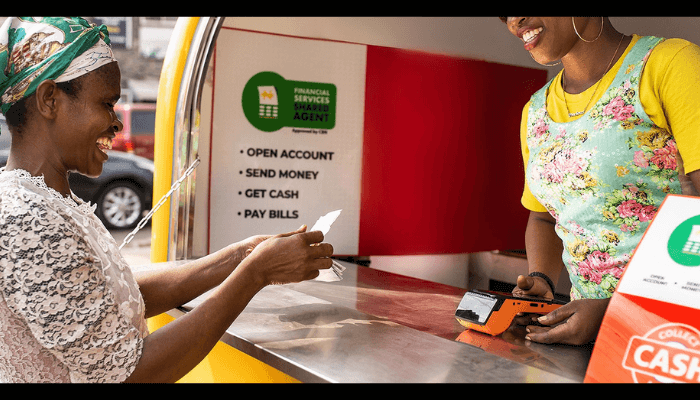

The latest figures by EFInA put Nigeria’s financial inclusion rate at 63.2 percent, meaning as much as 36.8 percent of adults still lack access.

According to the EUI report, some of the reasons why Nigeria did record a high score in the 2019 global microscope include the fact that “Nigeria does not incorporate a gender approach in its financial inclusion or financial literacy strategies, does not collect data on financial services for low-income populations and does not have a digital literacy strategy.”

The World Bank’s 2017 global Findex database put Nigeria’s financial inclusion gender gap at 24 percentage points. Also, the latest figures by EFInA revealed that 55.9 percent of the financially excluded 36.6 million adults are women; this is 11.8 percentage points higher than the male population at 44.1 percent.

“As financial inclusion policy shifts its focus towards the promotion of digital financial services, regulators and policymakers must address this digital gender gap or risk contributing to even greater disparities in access to financial services between women and men,” the EIU said.

Further analysis of the EUI report revealed that Nigeria lagged its Africa peers in the scored recorded in 2019. South Africa attracted 63, followed by Kenya at 54. Ghana also made the list of top countries in Africa with conducive environment for financial inclusion as it reported 48, 5 points higher than Nigeria’s score of 43.

Nigeria’s central bank is optimistic that it will achieve the 80 percent inclusion target by next year. In the quest to achieve the 20 percent exclusion target, the apex bank on the 5th of October 2018 released an exposure draft guideline in which it proposed Payment Service Banks (PSB) aimed at deepening financial inclusion.

Since inviting Telcos and other industry players to apply for the mobile money licence over a year ago, the industry regulator has only granted Approval-In-Principle (AIP) to Hope, Money Master, and 9PSB to operate as payment service banks.

According to EUI, four basic enablers are required in promoting digital financial inclusion. The report identified – “allowing non-banks to issue e-money, presence of financial service agents, proportionate customer due diligence and effective financial consumer protection.”

In the 2019 report, only four countries – Colombia, India, Jamaica, and Uruguay – scored perfectly across all four parameters. Latin America remained the region with the most conducive regulatory and policy environment for financial inclusion.

The 2019 Global Microscope analysed the policies used by governments and regulators around the world to increase financial inclusion among their populations. Informed by the vision of the Centre for Financial Inclusion at Accion (CFI), the Microscope defines financial inclusion as access to a full suite of quality financial services for customers who possess financial capability, provided via a diverse and competitive marketplace.

Endurance Okafor