Nigeria’s telecommunications operators are facing a deepening margin squeeze as average revenue per user (ARPU) continues to decline, even as subscriber numbers grow and operating costs remain largely flat, underscoring a structural challenge confronting the industry across sub-Saharan Africa.

A new report by PwC, presented at a Nigerian Communications Commission (NCC)-organised stakeholder workshop on competition in the voice and data market segment in Lagos, shows that the traditional growth model of adding subscribers is no longer translating into proportional revenue gains. Instead, telcos are grappling with eroding pricing power in an increasingly commoditised market for voice, SMS and basic data services.

PwC attributes the sustained decline in ARPU to a combination of aggressive price competition, weakening consumer purchasing power and the rapid shift in user behaviour away from traditional telecom services toward over-the-top (OTT) platforms. While operators have expanded network coverage and customer bases, revenue per customer has trended downward since 2020.

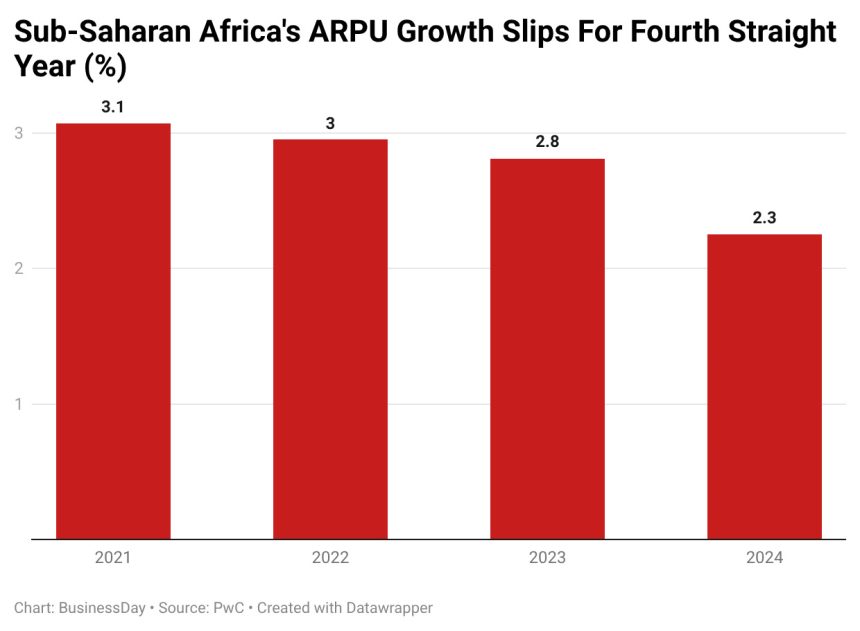

Comparative data in the report highlight the scale of the challenge. In 2020, ARPU growth in sub-Saharan Africa stood at just 2.95 per cent, far below the 28.23 per cent recorded in Asia Pacific and 7.19 per cent in the Middle East and North Africa (MENA). The gap has persisted, with the region recording ARPU growth of 3.07 per cent in 2021, 2.95 per cent in 2022, 2.81 per cent in 2023 and 2.25 per cent in 2024, consistently trailing other global markets.

Globally, the outlook offers little relief. PwC projects telecommunications revenue growth of only 2.9 per cent compound annual growth through 2028, bringing industry revenues to about $1.31 trillion. That pace remains below projected global inflation of between 3.7 per cent and 5.8 per cent annually over the same period, implying continued real-terms pressure on operator margins. “The industry’s core offerings which are fixed and mobile connectivity, are increasingly commoditised, limiting pricing power and squeezing margins,” PwC said in the report.

In Nigeria and across the region, inflation and low disposable incomes have further constrained consumers’ willingness to pay for premium telecom services. Operators have found it increasingly difficult to raise tariffs without risking customer churn in a highly competitive market.

At the same time, consumer behaviour is undergoing a fundamental shift. According to PwC, subscribers are now digital-first, favouring app-based self-service channels over physical customer care centres. Electronic KYC onboarding, mobile apps, chatbots and digital top-ups have replaced paper recharge cards and in-person transactions, reshaping how operators interact with customers.

Data consumption is also being driven less by generic browsing and more by social interaction and entertainment, particularly among younger users. Platforms such as TikTok, WhatsApp and streaming services now account for a growing share of mobile data usage, reducing the relevance of traditional voice and messaging revenues.

This shift has forced telecom operators to rethink how data is priced and packaged. Rather than selling connectivity as a standalone product, operators are increasingly positioning data as an enabler of digital experiences.

To arrest the decline in ARPU, Nigerian and global telcos are turning to bundled offerings that integrate third-party services such as streaming platforms, fintech solutions, utilities, health and telemedicine services.

PwC noted that telecom operators now account for about 77 per cent of streaming partnerships worldwide, reflecting their strategy of using content and lifestyle services to drive customer retention and engagement.

As of 2024, around 20 percent of the global streaming market is distributed through telco bundles, highlighting the growing role of operators as aggregators of digital services rather than mere connectivity providers.

“Telcos must design entertainment-first bundles and partner with OTT platforms to stay relevant,” PwC said.

Fifth-generation (5G) technology is also being positioned as a potential medium-term revenue stabiliser, though adoption has been slower than initially anticipated. PwC forecasts that 5G will account for about 64 per cent of global mobile subscriptions by 2028 and become the dominant mobile standard by 2026, with subscriptions projected to reach 7.51 billion.

In sub-Saharan Africa, however, 5G uptake remains constrained by infrastructure gaps, limited investment in research and development, and the slow penetration of 5G-enabled devices. Short- to medium-term adoption in the region is projected at just 14 percent to 17 percent, well below the global average.

Fixed Wireless Access (FWA) has emerged as a key 5G use case, offering operators an opportunity to expand broadband access in underserved urban and rural areas while creating new revenue streams beyond traditional mobile services.

According to Akolawole Odunlami, director, strategy at PwC Network, the challenges facing Nigeria’s telecom sector are part of a broader global shift. “Consumers no longer just buy connectivity; they buy experiences powered by connectivity,” he said, noting that data has become the backbone of communication, entertainment and digital services.

Regulators are also responding to the changing landscape. The NCC-commissioned study aims to assess market dynamics, competitive behaviour and barriers to entry, while ensuring that market leadership is driven by innovation and investment rather than anti-competitive practices.

PwC warned that long-term sustainability in the telecom sector will depend on how quickly operators can move beyond basic connectivity and integrate advanced networks, content and lifestyle services into coherent value propositions.

“Success will depend on who can move fastest from being connectivity providers to becoming digital service platforms,” the report said.