|

Getting your Trinity Audio player ready...

|

Nigeria’s Micro Pension Plan (MPP) expected to drive penetration of the country’s pension scheme is dragging due to economic hardship facing individual and businesses.

While individuals and households are struggling to meet basic needs following high cost of living and rising inflation, small businesses that are supposed to key into the MPP are struggling to remain afloat as result of declining purchasing power of consumers.

All of these put together are affecting enrolment in micro pension plan, as well as remittance by individual and small businesses, according to potential participants who shared their feelings about the scheme.

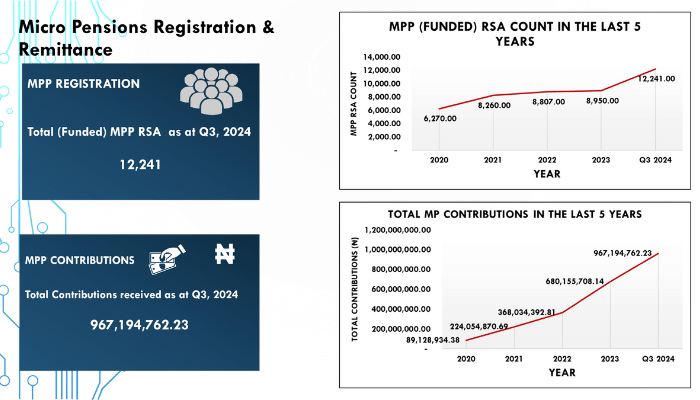

Data from the National Pension Commission (PenCom) shows that out of a total of N164, 031 Retirement Savings Account (RSA) holders registered since inception of the MPP in 2019, only 12, 241 of the them are fully funded.

The MPP, launched in 2019 is a retirement savings scheme specifically created for individuals in the informal sector (business owners, artisans) and organisations with less than three employees.

It allows contributors to save towards their retirement or in case of incapacitation.

Uche Obasi, chief executive officer of UC International Electronics at Alaba International said, he could have considered registering his two employees because he understands the benefits of savings, but stated that business has been dull for past years now.

“I have two staff that qualify for micro pension, my secretary and my admin manager. The other boys you find around are serving me, so that are not on a salary scale.” But, I feel pained that I am not able to enrol them in MPP because of drop in cash flow, he said.

On whether Pension Fund Administrators (PFAs) have come to market them, Obasi said, “yes, they have been here on many occasions. My neighbour that enrolled his three workers is not remitting yet because business is slow”.

From 2020 to Q3 2024, the number of funded RSA registration increased by 5,971.

The total amount saved in the RSAs of Micro Pension Participants stood at N967, 194,762.23 as of third quarter 2024, which represented a growth of N878, 065, 827.85 from the 2020 figure of N89, 128,934.38.

Kunle Omololu, an architect said he cannot save for pension now when he is yet to stabilise, particularly for the fact that business in not stable.

“I could have thought of saving, but my income has not been enough to do the things pressing now, let alone saving”. May be with time I will consider it, he said.

Omolola Oloworaran, director-general, PenCom said the Commission is poised to drive the Micro Pension Plan (MPP) with healthcare incentives and operational flexibility that makes it attractive to informal sector workers and other self-employed professionals.

She said this has become necessary to make sure that many people in the informal sector as well as professionals in organisations having less than three employees take advantage of the window to save for their old age.

Babatunde Alayande, head of Micro Pension Department at PenCom speaking during an interview session in Lagos explained that Micro Pension Plan is not just for the informal sector, but also for self-employed professionals such as the accountant, lawyers, town-planners, engineers working in for themselves or in organisations that are less than three employees.

He said PenCom will intensify its awareness and sensitization programmes on micropension.

According to him, “Part of what the commission is looking at is create awareness by letting people know that micro pension is not just for informal sector workers alone, but for processionals.

“The commission is working assiduously to make sure that there are incentives for people participating in this micro pension plan, especially, incentives for the informal sector.

“Part of the focus of the commission in this respect is the need to incentivise the informal sector participants with basic health insurance plans to encourage them, so they do not just bring money and save, but have other benefits.

“The commission has ensured that contribution into Micro Pension Plan is flexible in the sense that you can contribute daily, weekly, monthly or quarterly, depending on the type of work you are doing.”

Ibrahim Garba Buwai, head of Corporate Communications, PenCom, said, micro pension is about financial inclusion, providing a platform for savings so that workers can have something to fall back onto, especially in the time when they are no longer active.

He said, “The micropension takes care of the peculiarity of this particular sector in the sense that we know that they have ongoing needs. The 40 per cent of their RSA is for contingency, meaning if you have needs, emergency, to pay medical bills, children school fees, and you can withdraw from the RSA, while the remaining is set aside for the purposes of pensions.