Of all the momentous changes sweeping across southern Africa, the least noticed — though perhaps the most significant — are those in Angola. Understandably there has been great focus on Zimbabwe, where Robert Mugabe was pushed out by the military and a new leader installed and subsequently elected. In South Africa, too, the ousting of Jacob Zuma and his replacement as president by Cyril Ramaphosa has raised lavish expectations that the rot of the Zuma years can be extinguished. But it is events in Angola, sub-Saharan Africa’s third-largest economy and its second-largest oil exporter, where arguably the greatest drama is taking place.

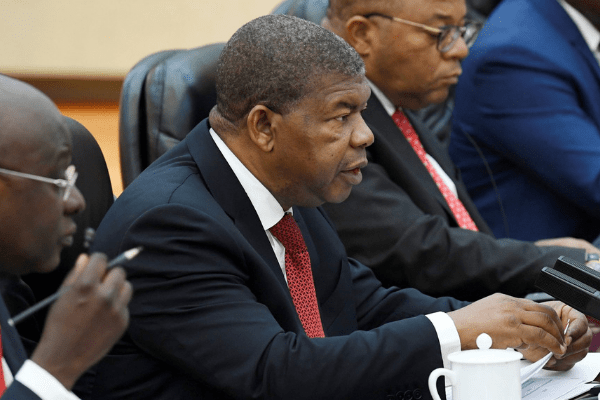

It all began in August 2017 with what looked like a routine — if generational — changing of the guard. After 38 years as president, José Eduardo dos Santos nominated João Lourenço as his successor. Angola had been one of the most tightly controlled economies in Africa, with much of the country’s considerable wealth centred around a coterie of well connected people. During her father’s reign, Isabel dos Santos — the “princess of Angola” — had become the richest woman in Africa, with an estimated net worth of $2.2bn. One of the president’s sons, Filomeno, considered less astute in business than his sharpshooter sister, was given a $5bn sovereign wealth fund to play with.

Most Angolan observers assumed that little would alter. Although Mr Lourenço would be president, Mr dos Santos would remain chairman of the People’s Movement for the Liberation of Angola (MPLA), the party that has dominated Angola since independence in 1975. Many expected Mr Lourenço to be a puppet. Instead, he has grabbed hold of the strings.

Change began almost immediately. In his inauguration speech, Mr Lourenço — or JLo as he is known — hit out at the monopolies in telecoms and cement controlled by the dos Santos family. He fired the governor of the central bank, later alleging there had been a plot to spirit $500m of the country’s reserves abroad in the final weeks of the dos Santos era.

These turned out to be just the opening shots. Subsequent events have had Angola-watchers gasping. Filomeno was ousted as head of the sovereign wealth fund. Isabel — whom many had regarded as untouchable — was sacked as head of Sonangol, the state oil company cum cash machine. Filomeno was then arrested in connection with the missing — now recovered — $500m. His close associate, Jean-Claude Bastos de Morais, whose Zurich-based Quantum Global was given the mandate to manage the $5bn sovereign wealth fund, is also in custody. The government accuses him of mismanaging the funds and charging excessive fees, allegations he denies. Quantum Global also denies involvement in the alleged $500m fraud.

Last month, Mr Lourenço replaced Mr dos Santos as MPLA chairman, earlier than expected. The new central bank governor has begun to clean up a banking sector riddled with bad loans, many linked to cronies of the old regime. Angola has begun to woo foreign investors, to talk of private-sector led growth and of diversification from oil, which accounts for 95 per cent of exports.

What happens in Angola matters. Though inequality is entrenched, it is an upper middle-income country with a gross domestic product of about $125bn, six times the size of Zimbabwe’s. It produces 1.7m barrels of oil a day, making it the world’s eighth-largest exporter. Reserves, which have been dwindling, could rise again if Mr Lourenço persuades multinationals to step up their investment. Angola is also a locus of the new “scramble” for Africa, a country where China has made huge inroads. In the past three years alone, Angola’s debt has ballooned by $23bn, much of it money from Beijing. Mr Lourenço has shown signs of wanting to tilt back to the west, repairing relations with western oil companies and seeking help — and therefore scrutiny — from the IMF.

Still, there are reasons to pause. The anti-corruption drive may not lead to genuine change. So far, the campaign has been targeted tightly around close associates of the previous dos Santos regime. It is easy to pin all Angola’s woes on the leader of the past four decades. It is harder to put something coherent in its place. As with China’s president Xi Jinping, Mr Lourenço may be motivated more by consolidating power and shoring up the ruling party than by a genuine overhaul of the political economy.

Nor is it clear what impact changes will have on 28m ordinary Angolans. Many are desperately poor in spite of the country’s obvious wealth. If the economy is managed better, their lot could improve. But only if it is managed radically differently can it be transformed. The curtain is closing on the old era. The hope — still only a hope — is it will open on a new one.

Luigi Di Maio, deputy prime minister and head of the anti-establishment Five Star Movement, told Italian media this week that the budget would still be imposed even if the spread were to rise above 400bp.

However, Credit Suisse analyst Carlo Tomaselli was sceptical about the government’s position, saying: “The sovereign spread above 400bp is not sustainable.”

Mr Tomaselli estimated that a 200 point widening versus the end of June would reduce Italian banks’ common equity tier 1 ratio — a key benchmark of balance sheet strength — from 12.5 per cent to 11.9 per cent, on average.

A hit to equity buffers of that scale would trigger a string of fresh capital raisings, he forecasted.

Having loaded up on so much government debt, there was little Italian banks could proactively do to try to sever the doom loop, said Mr Codogno. “They can either cross their fingers and hope this goes away, or they can reduce their exposure to Italian bonds and recognise the losses,” he said.

Marina Brogi, a professor of banking at the Sapienza University of Rome, said there were reasons to be more optimistic now than in 2011, when Italy’s borrowing costs surged to post-crisis highs and raised alarm bells about the dangers of the mutual embrace of banks and government. Banks now have more liquidity and the Italian economy is showing “signs of life”, she said.

Yet Mr Alloatti said that if spreads were to stay at current levels, banks would still face a slow-motion crisis given that their cost of funding would rise.

“If in one month’s time the difference between the BTP and the Bund goes back, then we’re all fine, and we can go and enjoy a skiing holiday,” he said. “But if spreads remain where they are, we are facing the worst scenario: a credit crunch.”

Mr Codogno said that would leave banks with “no choice” other than to reduce lending to consumers and businesses, which would imperil the Italian recovery.

A crisis in Italy would raise fears that financial stresses could spread to neighbouring eurozone economies like Greece, where investors have also been dumping bank shares dragging them to record lows this week.

Yannis Stournaras, governor of the Athens central bank, on Wednesday tried to calm fears that Greek banks could see a renewed flight of deposits similar to that in 2015, which resulted in the imposition of capital controls that have yet to be fully lifted.

“The share price developments of recent days have no relationship with the health of Greek banks,” he said. “They derive from purely external factors, specifically the rise of interest rates internationally, especially in neighbouring countries to Greece [such as Italy and Turkey].”

Any contagion would increase pressure on the ECB, which has faced calls in Rome to delay the end of its massive €2.5tn sovereign bond-buying programme, dubbed quantitative easing.

The central bank’s senior officials insist they plan to start winding down QE by the end of the year, but add that they are monitoring the situation in Italy closely.

The ECB’s banking watchdog — the Single Supervision Mechanism — thinks that the widening spread between BTPs and Bunds could force Italian banks to tap markets for extra cash.

Those concerns were also expressed by the Bank of Italy’s deputy director-general Luigi Federico Signorini at a parliamentary hearing on Tuesday.

The worry for the banks is that if market conditions do not improve in the coming months, such capital raisings are likely to be at best hard to pull off and extremely costly.