In the insurance industry, some firms that are sweating owners’ money in taking on more risks have seen liability balloon and are rewarded with huge

premium income compared to c0mpetitors that allow such money lie fallow.

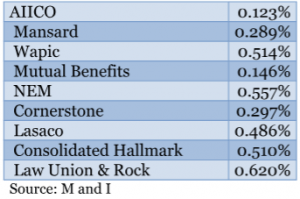

Analysts are of the view that companies with low leverage and high liabilities may have underwritten annuity products. After all, the kind of risk undertaken determines the asset and liability side. Nigerian insurers such as AIICO Insurance Plc, the country’s largest quoted insurer by assets, as well as Mutual Benefit Plc have financial leverage ratio-which simply divides equity by asset- between 12 percent and 15

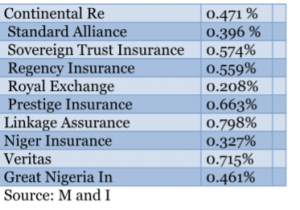

percent, this compares with Linkage Assurance Plc; 79.87 percent, prestige Assurance, 66 percent; Wapic Insurance; 51, Law Union and Rock; 62

percent, NEM Insurance Plc; 55 percent, Regency Assurance; 56 percent and Sovereign Trust Insurance Plc 57 percent.

“Equity is a liability to the organization and owners expect a return for taking the risk. The low ratio could be that these firms have annuity in their books,” said Moronfola Monsuru , actuarial analyst – Wapic Insurance Plc “Because these firms are sweating their shareholders’ fund, it is

unsurprising they have huge liabilities in their balance sheet,” said Monsuru.

Every insurer is taking in premium and paying out claims. Every insurer should ensure that they strike a balance between returns and leverage. It is generally acceptable finance principle that a highly geared firm might not be able to meet financial obligations when a large catastrophic event

occurs. Indeed there is a correlation between leverage ratio and the size of premium income as firms that utilize assets generates more revenue. AIICO Insurance with a leverage ratio of 12 percent, has gross premium written of N27.67 billion as at September 2018, this compares with Linkage

Assurance, a firm with a leverage ratio of 79.87 percent, and gross premium written of N4.53 billion. Similarly, Mutual Benefit Assurance with a leverage ratio of 14 percent, has gross premium written of N11.30 billion in the period under review, this

compares with prestige Assurance leverage ratio of 66 percent and gross premium income of N3.79 billion. The business of an insurance company is to underwrite risk. This means they have more shareholders’ funds than equity. The ones that have a high

ratio are not sweating their asset enough. They are lethargic, according to an industry expert who doesn’t want his name mentioned.

Insurers have continued to lose huge premium to foreign firms due to lack of capacity to take on lore risk despite regulators efforts in ensuring that players in the industry maintain strong capital base. For instance, the cumulative shareholders fund of 19 largest quoted insurers was N191.95 billion as of September 2018; this is less than Tier 2 lender Fidelity Bank’s total equity of N192.38 billion.

Nigeria loses a whopping N2.8 trillion annually to foreign insurance companies due to low capacity of local insurers to absorb huge risks,

LEADERSHIP Newspaper investigations have revealed.

Investigation by LEADERHIP reveals that foreign insurers control more than 80 per cent of risks in the country, owing to the fact that only about 15

to 20 per cent are retained locally. Most airline owners prefer they have assets insured by foreign firms as the

local players continue to grapple with weak capital base.

Insurers equity to asset ratio Q3’18

Insurers equity to asset ratio Q3’18