A 12-month clock, capital floors of N10bn–N35bn, and a sector that must raise, merge or fade.

Nigeria’s insurance industry is set for a shake-up as the Nigeria Insurance Industry Reform Act (NIIRA) introduces tougher capital requirements. Insurers now need N15 billion to operate non-life business, N10 billion for life, and N35 billion for reinsurance, or risk losing their licences within 12 months.

The move mirrors the Central Bank’s recent banking recapitalisation drive, which pushed many lenders to the capital market through public offers and rights issues. Investors who bought into those bank offers have already seen value growth, and analysts say insurance may be the next sector to deliver similar opportunities.

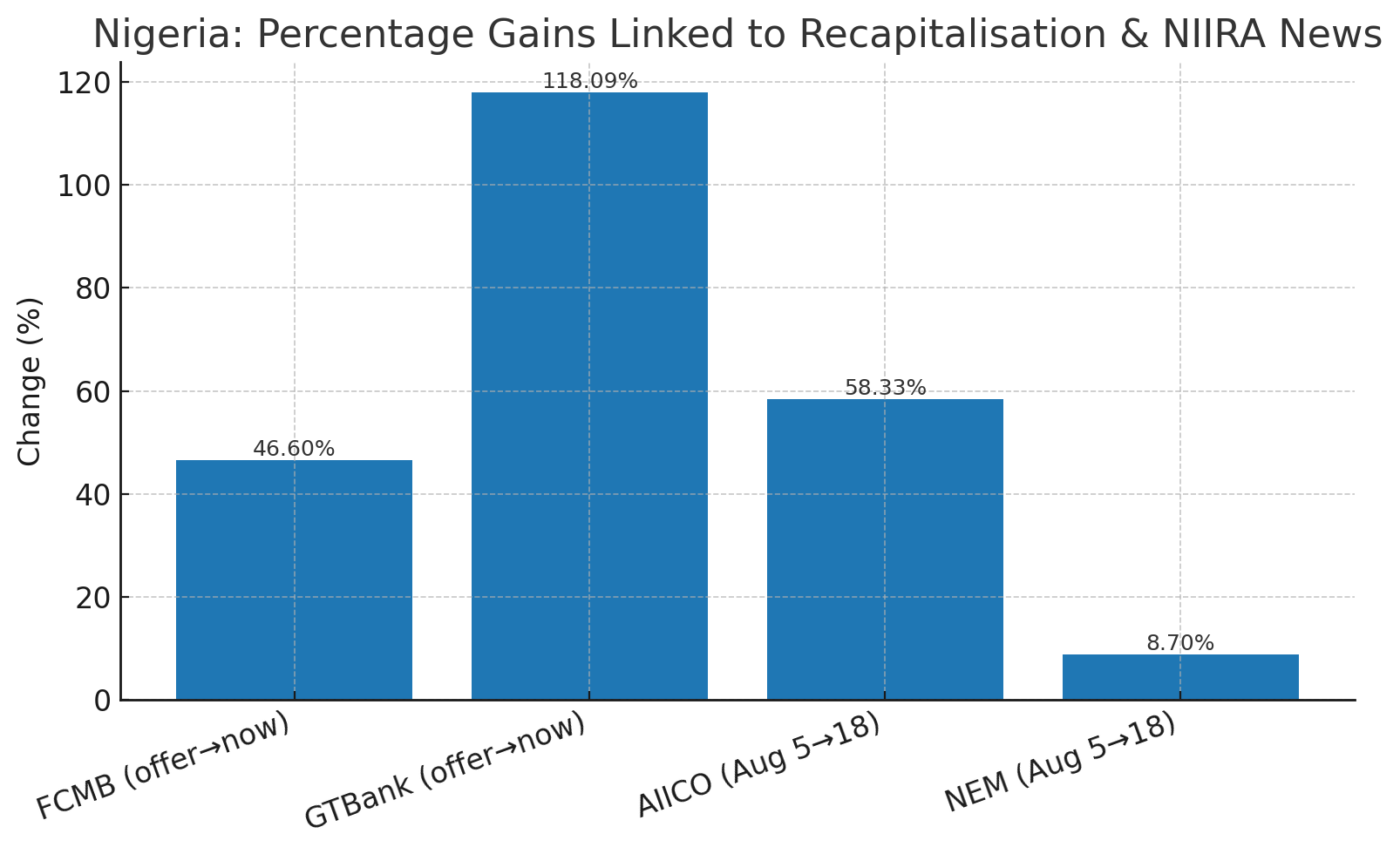

For instance, when the CBN announced the new capital requirement for commercial banks, it increased from N50 billion to N500 billion. FCMB engaged in a public offer at N7.30 per share to raise capital, while GT Bank, on the other hand, issued a public offer at N44.50 per share to both existing shareholders and the general public.

As of today, both FCMB and GTBank’s share price have increased by 46.6 percent and 118.09 percent, respectively, to N10.7 and N97. This means that anyone who participated in the GTB public offer would have gained N52.50 for every share owned; that is, N200,000 invested then would be N435,955.06 today.

That kind of payoff could be repeated in insurance if recapitalisation drives a similar rush of offers.

Already, insurance stocks have shown a glimpse of what is likely to happen. When the NIIRA bill was signed by President Bola Tinubu, insurance companies’ shares began to rise. AIICO, for instance, rose from N2.64 on August 5, 2025, to N4.18 on August 18, 2025, a 58.33 percent gain within just 14 days. Similarly, NEM Insurance climbed from N27 to N29.35, an 8.7 percent increase.

Though there is no clarity yet on how this capital will be raised, if insurers are required to turn to the capital market, the general public must be alert.

Olusoji Oluwole, President of the Association of Senior Staff of Banks, Insurance and Financial Institutions, told BusinessDay on BDTV that the reform is long overdue and could transform the industry if properly managed. According to him, the law is expected to “create a stronger insurance industry in Nigeria, an industry that is trusted, and one that will be able to expand beyond the shores.”

He acknowledged that the new thresholds may be steep, but mergers and acquisitions are likely, and investor appetite already appears strong.

“The moment President Tinubu signed the law, we saw insurance stocks rally, with many hitting the daily 10 percent limit. That tells you people are already taking positions. If these companies go to the markets, they are probably going to be over-subscribed,” he said.

According to industry experts, recapitalisation is more than a compliance story; it is a capital-formation play with real-economy spillovers. Rights issues will channel household savings into equities, while larger insurer balance sheets add a steadier bid for FGN and investment-grade corporates, supporting the long end of the curve. Stronger local capacity should lift risk retention in naira and trim FX outflows on reinsurance and claims.

Expect some near-term premium resets as solvency is rebuilt; over time, scale and competition ought to stabilise rates and broaden cover. With improved solvency, insurers can expand guarantees, surety and trade-credit products that de-risk bank lending to SMEs and infrastructure.

For investors, that optimism signals not just compliance pressure on insurers, but also a chance to buy into an industry that could finally awaken its long-touted potential.