Nigeria’s economy has been in a ditch in the last five years. Nigerians grew progressively poorer, as economic growth remains too slow to create sufficient opportunities for a rapidly rising population.

Read Also: Buhari sets record as Nigerians grow poorer for sixth straight year

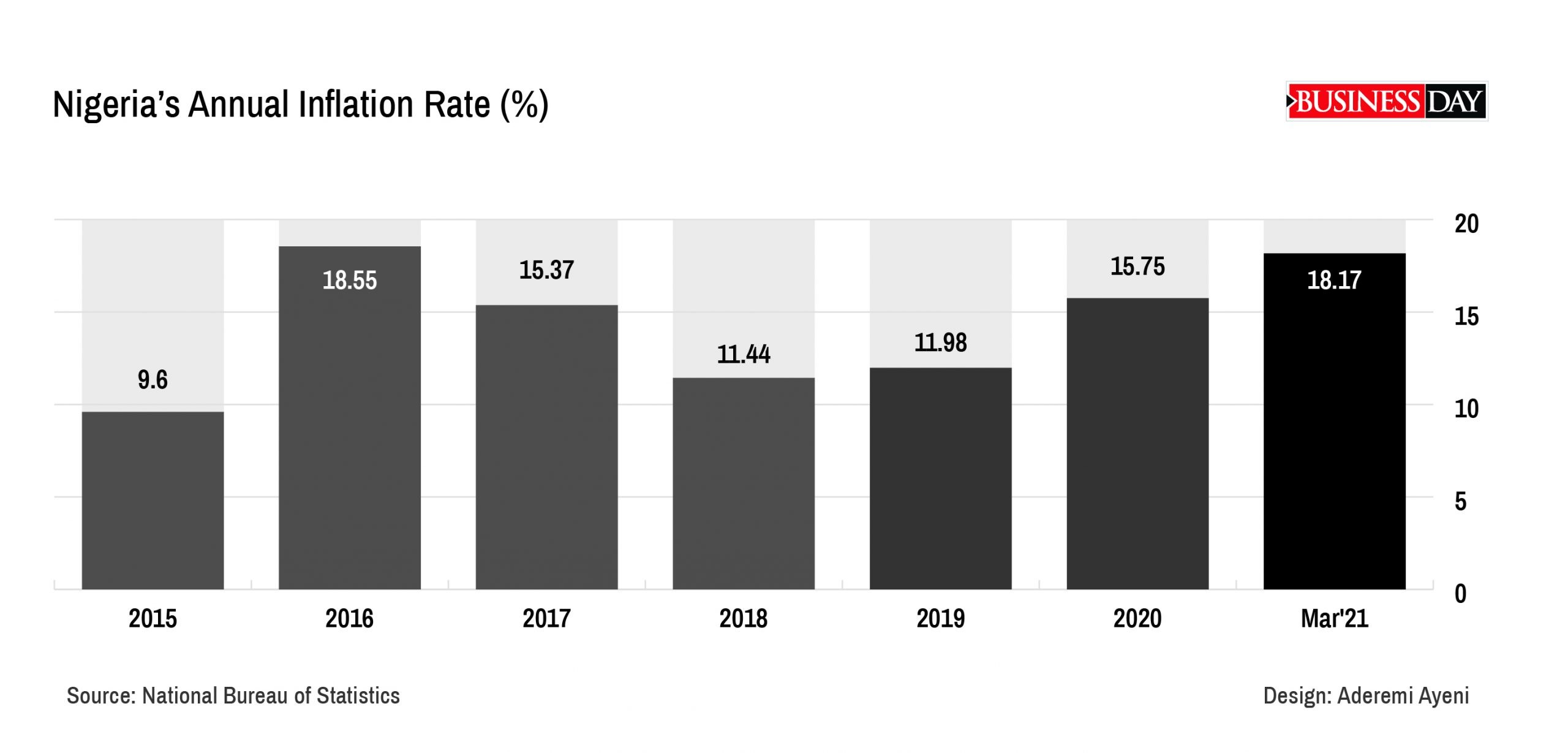

From a four year-high inflation rate, rising level of joblessness to per capita income that has been on the decline since 2015, Nigeria’s economic fundamentals point to the fact that the largest economy in Africa is stuck in a rut and is in dire need of rescue.

“We are in a very difficult economic and social situation right now in Nigeria and it is going to take real effort to recover from it,” Andrew S Nevin, Partner, chief economist at PwC Nigeria, said adding that Nigeria is not a poor country.

The current realities in Nigeria mean there is more hardship for many of the country’s citizens. What Nigerians can buy today is three times less of the usual consumption basket they could afford five years ago.

“This is the worst Ramadan celebration I have seen in the history of my business,” an attendant at a local spot that serves as both restaurant and pub, said while packing to close for the day, three hours before her closing time.

For Joy Amandi, a foodstuff vendor, the high cost of her food items are reasons why her “customers don’t buy much anymore.” According to her, “rising transportation cost and the hike in food prices,” by her suppliers are why the end buyers are paying more.

With a low earning capacity that is far below the rising cost of living, Nigeria’s misery index, an indicator that is used to determine how economically well off the citizens of a country are, jumped to 50.48 percent in March 2021 from 14.75 percent in 2015.

“It is the reality,” Ayodeji Ebo, Head, Retail Investment, Chapel Hill Denham, confirmed.

While 1 in every 3 Nigerians is unemployed, those that have been able to pin a job spend ~65 percent of their income on food, the main driver of the country’s inflation rate (18.17 percent in March). Food prices accelerated to the highest level in 15 years at 22.95 percent in March.

“Climbing misery index implies declining economic activity and reduced consumption,” Charles Akinbobola, an analyst at Sofidam Capital said.

Before covid-19 about 80m of Nigeria’s 200m people lived on less than the equivalent of $1.90 a day. The pandemic and population growth could see that figure rise to almost 100m by 2023, says the World Bank.

According to analysts, Nigeria’s economy can now be best described as one that is stagflated, a situation of poor Nigerians getting poorer in real terms, and the middle class getting thin out.

The reverse would have been the case if the economy of the top crude exporting nation in Africa expanded above the paltry 0.1 percent it reported in the fourth quarter. Though out from the recession, Nigeria’s gross domestic product (GDP) growth has been narrow and not broad-based.

Economic growth means a rise in real GDP. This enables a rise in living standards and greater consumption of goods and services. It also makes it possible for governments to cater for any increases in population without having to lower the standard of living. It can also help to reduce government borrowing as a booming economy creates higher tax revenues.

Economic growth in Africa’s most populous nation averaged 1.2 percent between 2015 and 2020. The problem with that is the population grew two times faster at an average of 2.6 percent per year.

If President Muhammadu Buhari would be willing to redirect Nigeria’s economy away from the path it has treaded without positive result in the past few years, he would have to take seriously some of the recommendations by the Presidential Economic Advisory Council (PEAC) to take Nigeria to economic prosperity.

Clarity and consistency in petrol pricing policy

While the Council explained that its understanding of government policy is that the regime of subsidy has ended, it said current petrol pricing, however, does not reflect the removal of the subsidy.

“Higher crude oil prices mean that the cost of imported petrol should be higher than the N167/litre being paid at filling stations. In other words, there is a subsidy,” it said.

In March last year, when the international price of crude oil was low, the federal government announced that it had deregulated the downstream sector, which meant that the pump price would be determined by market forces.

That policy was implemented for months until crude oil prices rose again, and the eventual return of subsidies’ payment, which the NNPC has put at about N120 billion monthly.

“As there is no provision for subsidy payments in the 2021 budget, such payments will have to be done by NNPC thereby further reducing revenues accruing to the Federation Account,” PEAC said in its recent report, adding that the restoration of subsidy would mean that the solvency of many state governments will worsen – this could take us back to 2015 when the Fed Government had to provide ‘bailout’ funding to the States, it said.

Structural policies to address insecurity

Defeating Boko Haram decisively, as a decisive defeat is necessary to keep the insurgency at bay forever, the Council said.

It explained the need to also re-strategize on the way forward, looking at all options, including seeking the assistance of external powers.

The higher cost faced by Nigerian companies on account of insecurity feeds through the economy. The report by the PEAC puts the economic cost of insecurity at 2.6 percent of GDP in 2020, or $10.3 billion.

Boko haram and other ethnoreligious conflicts – mostly caused by suspicion and distrust among various ethnic groups and herders-farmers clash- largely as a result of open cattle grazing and its impact of crop destructions are top of some of the insecurity challenges that have largely dragged the Nigerian economy.

Exchange rate unification

Nigeria, unlike it African peers, has continued to operate multiple exchange rate window.

Nigeria’s Central Bank adopted multiple exchange rates in a bid to avoid an outright devaluation last year. The official rate used as a basis for budget preparation and other official transactions differs from a closely controlled exchange rate for investors and exporters known as Nafex, a rate that is different from the parallel market, considered illegal by the central bank.

The volatile exchange rate has eroded the purchasing power of Nigerians with the naira going through two devaluations last year alone.

Realising the naira is not an efficient store of value, many Nigerians are increasingly holding dollar-denominated assets from cryptocurrencies to foreign stocks but the government is now also trying to stifle those markets with unfavourable regulations.

“Continuing pressure on the Naira at the foreign exchange market suggests our external trading account remains weak – despite the increase in oil prices,” PEAC said.

Though Interest rates are now rising, the Council said the value of returns to savers and investors remain negative because prices are rising faster than interest.

“In consequence, savers and investors are actually losing money by holding the Naira. This continues to provide an incentive for Nigerians moving money into foreign currency,” the advisory council said.

Meanwhile, in the time since the economic advisory council was formed, Africa’s largest economy has slipped in and out of a second recession in five years, albeit pandemic-induced, the jobless rate (33.3% in Q4, 2020) is now the second-highest globally, only behind Namibia, and poverty is fast deepening.

Three years, six meetings with the President and several recommendations later, the economy is in even worse shape and it is not for a lack of putting forward sound economic advice before the President.

Rather, their recommendations have gone largely unheeded and the economy has bled with Nigerians paying the ultimate price.