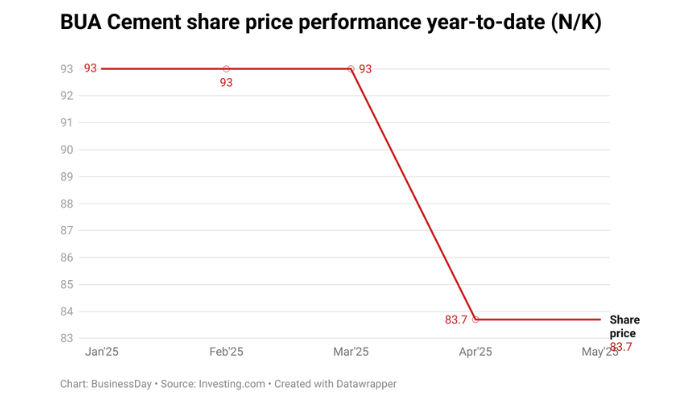

On May 23, the share price of BUA Cement Plc fell by 10 percent year-to-date despite the company reporting solid growth in its first-quarter profits, raising questions among analysts and investors about underlying market sentiments and broader macroeconomic pressures.

The cement giant, one of Nigeria’s leading manufacturers, announced a 351.4 percent year-on-year increase in profit after tax, driven by improved production efficiency, cost management, and stronger local demand.

Revenue also rose by 80.5 percent, supported by infrastructure expansion and government-backed construction projects.

Despite its improved earnings, BUA Cement also faces rising input costs, especially in energy and imported materials. The potential erosion of future margins may have triggered bearish sentiments among shareholders.

Read also:¬ÝBUA Cement proposes N2.05 final dividend as FY profit hits N73.9bn

The dip in BUA’s share price from N93 to N83.7 follows a broader pattern seen across Nigeria’s industrial sector, where high-interest rates and unstable forex conditions have overshadowed corporate earnings growth.

Cost of sales rose by 31%

Cost of sales rose 31.2 percent YoY to N152.4 billion, driven by increases in material costs (34.8 percent) and energy costs (48.8 percent). However, cost growth was tempered by improved efficiency by the management and a high base from the prior year.

Analysts at CardinalStone Research said in a report that OPEX grew 73.8 percent YoY to N20.2 billion, largely due to a significant rise in distribution expenses (112.8 percent YoY to N10.5 billion).

“Despite these cost pressures, robust top-line growth more than offset the increase in expenses, resulting in a 20.2 ppts expansion in EBIT margin to 40.9 percent,” it said.

FX pressure eased by 91.7%

The FX volatility that significantly impacted BUA Cement’s performance in FY’24 eased considerably in Q1’25. The company reported a lower FX loss of N836.8 million, compared to N10.1 billion in Q1’24, highlighting the positive impact of naira stability during the period.

“We have revised our FX loss assumptions downward, resulting in a higher projected PBT margin of 35.4 percent for FY’25E (previously 20.5 percent) and a PAT margin of 27.6 percent (vs. 15.2 percent previously),” CardinalStone Research disclosed.

Read also:¬ÝBUA Cement, others fuel market‚Äôs N275bn loss ahead of T-Bills auction

Earnings per share rose

BUA Cement EPS rose to N239.56 in Q1 from N53.65 in Q1’24.

Cardinal Stone attributes the rise to BUA Cement’s strong start to the year, with earnings per share (EPS) settling at N2.40—already surpassing the full-year 2024 EPS of N2.18.

“Consequently, we now expect EPS to print at N9.76, representing a 333.2 percent YoY increase,” it said.

Spike in income tax

BUA Cement paid N18.8 billion in tax for the first three months of the year, compared to N3.3 billion in the corresponding period of last year.

“Effective tax rate rose 3.1 ppts to 18.7 percent due to increased deferred tax charges,” CardinalStone disclosed in a report.