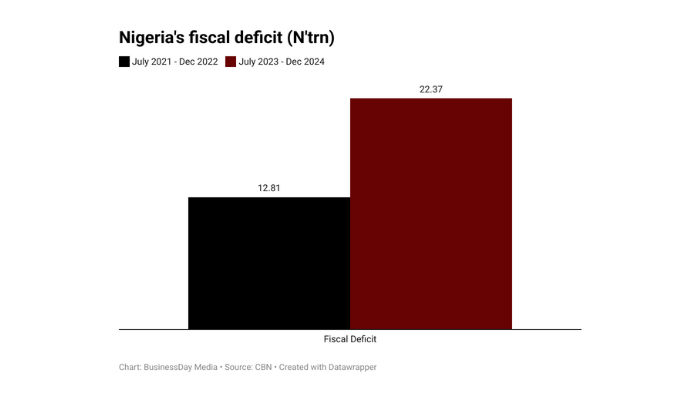

The federal government’s fiscal deficit grew to N22.37 trillion in the first 18 months of President Bola Tinubu’s administration (July 2023–December 2024).

This marks a 74.6 percent increase from the N12.81 trillion deficit recorded between July 2022 and December 2023(under Muhammadu Buhari’s administration), according to new data from the Central Bank of Nigeria (CBN).

A fiscal deficit occurs when government expenditure exceeds its revenue. Experts warn that high deficits can limit investment in capital projects and human development, key drivers of economic growth, job creation, and poverty reduction.

Read also: Nigeria’s revenue machine roars to life under Tinubu

Revenue gains but spending increases

Despite a 59.41 percent growth in revenue to N12.64 trillion from N7.93 trillion, the government expenditure jumped by 68.82 percent to N35.02 trillion from N20.74 trillion in the corresponding period.

In this period, the federal government spent $6.99 billion on foreign debt and N9.61 trillion on domestic debt servicing.

This represents a 161.21 percent increase from the N3.68 trillion spent on domestic debt and 127.90 percent more on the $3.07 billion spent on foreign debt servicing in the previous period.

In 2024, Muhammad Abdullahi, a member of the Central Bank’s Monetary Policy Committee, warned that the government was spending more money than it was making, pushing deficit financing to 7.5 percent of GDP as of August 2024.

“The Federal Government’s fiscal operations resulted in a budget deficit of 7.6 percent of GDP as of August 2024. Monetary policy must thus remain proactive in dampening the likely consequences of the deficit, especially when the implementation of the new minimum wage gains traction,” Abdullahi stated.

However, in his May 29, 2025, speech, President Tinubu said, “Our fiscal deficit has narrowed sharply from 5.4 percent of GDP in 2023 to 3.0 percent in 2024. We achieved this through improved revenue generation and greater transparency in government finances. In the first quarter of this year, we recorded over N6 trillion in revenue.”

He credited this to his reforms, including the removal of petrol subsidies in 2023 and the liberalisation of the foreign exchange market. He added that the government had saved $20 billion from the fuel subsidy removal.

According to the World Bank, the federal government’s fiscal deficit narrowed to N10.5 trillion (3.8 percent of GDP) in 2024 from N11.9 trillion (5.1 percent of GDP) in 2023.

Read also: Nigeria, S’Africa among biggest losers as Africa forgoes $125bn in tax revenue

The improvement was attributed to revenue gains from foreign exchange (FX) reforms, stronger tax administration, and increased transparency in the remittances of government-owned enterprises and MDAs.

However, the bank also noted a rise in expenditures due to wage increases and new initiatives like the presidential metering project.

Unlike his predecessor, Tinubu has not resorted to Ways and Means financing to fund his deficit. “In a crucial positive step toward restoring fiscal discipline and reducing inflation, the authorities have ceased resorting to deficit monetisation through ways and means,” the World Bank stated.

The federal government’s debt stock with the CBN (including securitised ways and means of N22.7 trillion in Q2, 2023) stood at N28.04 trillion at the end of 2024, a N2.13 trillion increase from the N25.90 trillion seen at the end of 2023. However, the federal government’s borrowings from deposit money banks rose to N21.98 trillion at the end of 2024, a 54.31 percent increase from N14.24 trillion at the end of 2023.

Under former President Muhammadu Buhari, the federal government’s debt stock with the CBN grew by 335.98 percent to N9.33 trillion in 2022 from N2.14 trillion in 2016. In 2023, Zainab Ahmed, former finance minister, acknowledged the government’s revenue shortfall.

“We needed to borrow to be able to build these projects that will ensure that we are able to develop on a sustainable basis. Nigeria’s borrowing has been of great concern and has elicited a lot of discussions. But if you look at the total size of the borrowing, it is still within healthy and sustainable limits,” she said in 2022.

Nigeria’s total debt stock climbed to N144.67 trillion in 2024, and the federal government’s new borrowing plan could push that figure to N183 trillion by 2026.

Read also: We remain on track with our fiscal targets, says Tinubu

Challenges ahead

At the end of 2024, Fitch Ratings warned that if Nigeria failed to meet its deficit reduction targets, it could face currency depreciation, higher inflation, and costlier borrowing, all of which could undermine the government’s economic reform agenda.

The global credit rating agency emphasised that a larger-than-expected budget deficit in 2025 might increase pressure for further naira depreciation and push up prices and interest rates.

Echoing this, Dele Oye, national president of the Nigerian Association of Chambers of Commerce, Industry, Mines and Agriculture, said, “The reason the naira is crashing is because the government is running a deficit budget. The naira will start appreciating if the government’s expenses are cut down.”

He added that fiscal discipline could reduce inflation and restore macroeconomic stability

According to the World Bank, Nigeria’s 2025 budget of N54.9tn has ambitious macroeconomic assumptions and revenue forecasts that could increase deficits if not met. “Borrowing limits may be insufficient, which poses a risk of reverting back to deficit monetisation,” it said.

Wale Edun, coordinating minister for the economy, noted that the budget deficit of about N13 trillion for 2025 would be financed through borrowing.

On its part, Fitch questioned key assumptions in Nigeria’s 2025–2027 Medium-Term Expenditure Framework, including an oil price of $75 per barrel and production of 2.06 million barrels per day, higher than its estimates of $70 per barrel and 1.77 mbpd.

Read also: CBN holds MPR at 27.5%, urges fiscal push on export earnings

“Reducing the deficit in line with the MTEF would provide further credibility for the government’s reform agenda, but if the deficit target is missed, it may increase the pressure for further naira depreciation, as well as putting upward pressure on prices and interest rates,” it said.

It added that raising fiscal revenues, particularly from less volatile non-oil sources, remains a critical priority for improving the country’s credit profile and achieving macroeconomic stability.