There is need to shrink the gender gap in financial inclusion, as it seems like one that will not budge in the nearest future.

The World Bank in its Global Findex database shows a global gender gap of 7 percentage points, a gap that has remained in same level since 2011. This is happening despite the increase in the number of women who have been opening bank accounts in the same period.

“The financial freedom is still elusive to 980 million women around the world; worryingly, this does not seem to be improving,” the World Bank said in a statement.

Nigeria is seen as one of the very troubling countries in terms of persistent gender gap in financial inclusion.

Africa’s largest economy currently have 24 percentage points gap between the male and female adults who have access to basic bank accounts.

The data from the World Bank Findex database shows that 51 percent of Nigerian male adults had a bank account in 2017 compared to the 27 percent recorded for female.

This gap is however bigger than the 20 percentage points gap that was recorded in 2014 when the total male with accounts was at 54 percent with female at 34 percent. Morocco, Mozambique, Peru, Rwanda, and Zambia are other countries that also have double-digit differences between men and women.

Meanwhile, countries that had gender gaps in 2011 generally which are still having them today include; Bangladesh, Pakistan, and Turkey, the gap in account ownership between men and women is almost 30 percentage points in these countries.

This is different for some countries like Bolivia, Cambodia, the Russian Federation, and South Africa, where account ownership is equal for both men and women, as compiled from the World Bank.

In Argentina, Indonesia, and the Philippines, the gap recorded is the reverse, as women have more accounts than men.

A BusinessDay survey shows low earning as one of the main reasons why both men and women do not have a financial account. The median income of low earners in the country is about N10000 to N20000 per month.

Nigerian adults who responded to the question of why they do not have a bank account said they earn too little to open and operate a bank account, considering the cost of opening an account and charges that comes with having one is quite high.

The banks on the other hand said they incur high cost in running their operations, as the basic amenities that could have aid in delivering financial services at a lower cost are not available.

There are however some reasons that keep women specifically from opening accounts and this can be traced back step by step through unequal opportunities, laws, and regulations that put an extra barrier on women’s ability to even open that simple bank account.

“I opened my first bank account as a new student in a university in 1990. This seemingly small act meant that I could manage my own finances, spend my own money, and make my own financial decisions. It meant freedom to decide for myself,” Ayo Balkis said.

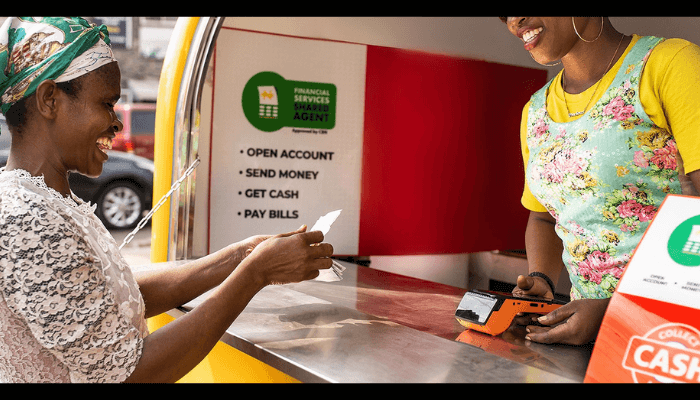

The World Bank however suggested ways to help bridge the financial inclusion gap in Nigeria and other parts of the world; with the use of technology and mobile banking, removing of discriminatory laws and the focus on financial capability.

On the use of technology, the lender cited moving routine cash transactions into financial accounts could shrink the number of unbanked women , as this is already working in both Europe, Central Asia, the Middle East and North Africa, where 1 in 5 women who have an account opened their first account to receive digital transfers of public sector wages, government social benefits, or public pensions. In Latin America and the Caribbean, the share is 14 percent.

At the same time, programs like M-PESA, the ground breaking mobile money transfer service in Kenya, have demonstrated the power of mobile banking. Drive through even the most rural area in the country.

This is a game-changer for rural poor who have generally had scarce access to financial institutions, and for whom the trip to the nearest bank has too high a cost in terms of travel or lost time at work.

Recent research showed that because of M-PESA, around 185,000 women in Kenya moved from subsistence farming to business or retail sales, and their savings went up as a result. As mobile phone ownership grows, this may be a way to jump past the traditional ways to access a financial institution and bring access to people where they are.

Although, an initiative of this kind has however not seen light in Africa’s largest economy, as there is yet to be collaboration between the telecom companies and the financial service providers.

In removing of discriminatory laws the World Bank said there were only three countries remaining where married women needs permission to open a bank account. This is progress, and yet this is also three too many.

Nigeria can be classified to be in this category, as A’isha, a lady from the Northern part of Nigeria said she is not permitted to go open a bank account or even leave the house to go do anything for herself, that she depends on her husband for everything and she was married to take care of the house and the children. This she also said is the culture and the believe of the people from her community.

“Even in places where women face often insurmountable odds, it is possible to change the laws that hold them back. In the Democratic Republic of the Congo—a country that performs at the bottom in nearly all aspects of gender equality—the World Bank Group worked with the ministries of Gender and Justice to change the country’s family law, which previously prevented married women from opening bank accounts, obtaining loans, signing contracts, or registering companies without the permission of their husbands. This led to the adoption of a new Family Code in 2016 that lifted these restrictions,” the World Bank said.

While on the focus on financial capability, boosting financial literacy among girls and women was cited by the bank, as this is not just improving their reading and writing skills, but also teaching them how to use a transaction account, how to manage and budget money, and how to save.

At the same time, the social, emotional and psychological aspects of financial decision-making can be just as important as basic technical skills.

Endurance Okafor