NigeriaŌĆÖs biggest banks are seeing a fresh resurgence in customer lending, with combined loans nearing N42 trillion in the first nine months of 2025, driven largely by a more accommodative monetary policy stance and early signs of renewed credit appetite across key sectors of the economy.

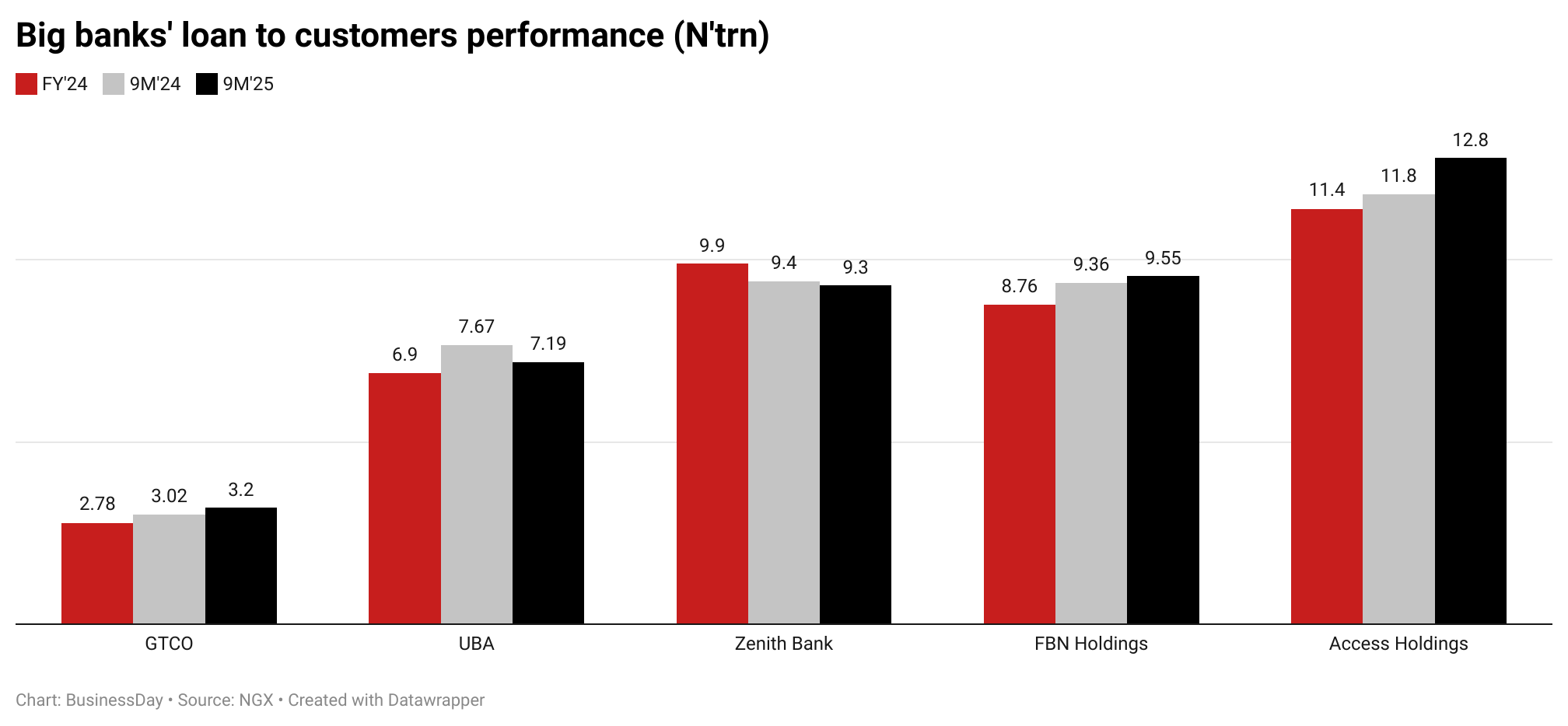

BusinessDayŌĆÖs analysis of the financial statements of Zenith Bank, GTCO, FBN Holdings, UBA, and Access Holdings shows that aggregate customer loans rose 2 percent from the N41.3 trillion recorded in the same period of 2024 and 5 percent above the full-year 2024 lending position.

The modest but notable uptick comes after nearly two years of tight liquidity conditions and elevated interest rates that slowed loan origination and forced banks to rely more on FX revaluation gains and investment securities for earnings growth.

Access Holdings led the expansion with customer loans rising to N12 trillion, the highest among its tier-one peers, reflecting its aggressive retail push, expanded pan-African footprint, and stronger appetite for corporate lending in infrastructure-linked sectors.

FBN Holdings followed with N9.5 trillion, supported by continued loan book diversification and improved asset quality. Zenith Bank ranked third at N9.3 trillion, driven by selective growth in manufacturing, trade, and digital services.

The loan growth coincides with the Central Bank of NigeriaŌĆÖs (CBN) first benchmark interest rate cut in five years. In September, the Monetary Policy Committee (MPC) reduced the Monetary Policy Rate (MPR) by 50 basis points to 27 percent, reversing a long cycle of tightening that pushed the MPR to historic highs.

The monetary authorities also adjusted the asymmetric corridor to +250/-250 basis points from +500/-100 and lowered the Cash Reserve Ratio for commercial banks by 500 basis points to 45 percent, freeing up liquidity and signalling a broader policy intent to support private-sector lending.

For banks operating in an environment of slowing yields on government instruments and easing inflationary pressures, the policy shift represents an inflection point in their earnings model.

Read also:┬ĀNigeriaŌĆÖs biggest banks top AfricaŌĆÖs 300 finance champions

Analysts at Meristem, in their October banking sector update, noted that the industry is transitioning into a phase of ŌĆ£earnings normalisationŌĆØ as the extraordinary FX revaluation gains that boosted profits in 2024 dissipate and banks gradually pivot back to traditional lending activities.

ŌĆ£Loan growth is likely to strengthen as expansion-focused sectors take advantage of a more favourable lending environment,ŌĆØ the analysts wrote, projecting a steady recovery in interest income over the next few quarters.

FX gains fade, exposing banksŌĆÖ core earnings

The shift in monetary conditions is occurring against the backdrop of a more stable currency market. The naira, which opened the year at N1,660 per dollar, traded within a tighter band through 2025, closing October at N1,427.50 at the Nigerian Foreign Exchange Market (NFEM). The narrower volatility drastically reduced opportunities for valuation gains, which had inflated banksŌĆÖ 2024 profit bases.

According to Meristem, banks that benefited heavily from FX revaluation reaped fewer gains in 2025, and in some cases recorded negative FX effects, weighing on non-interest revenue and overall sector performance.

This outcome was anticipated, given that the bulk of the 2024 revaluation windfall stemmed from reforms that allowed the naira to adjust sharply following years of currency suppression.

ŌĆ£The combination of lower interest rates on investment instruments, absence of one-off FX gains, and softer trading income made a decline in non-interest revenue unavoidable compared with the inflated 2024 base,ŌĆØ the analysts wrote, emphasising that 2025 is a corrective year for bank earnings.

For lenders, the return to a more traditional income structure means a heavier reliance on interest-earning assets, especially customer loans and advances. With yields on OMO and treasury instruments moderating and the CBN signalling additional policy easing in 2026, banks are increasingly recalibrating their balance sheets to favour loan expansion in industries with strong demand prospectsŌĆömanufacturing, infrastructure, energy, telecommunications, and the creative economy.

Credit risk management enters new territory

Parallel to the evolving earnings landscape, banks are contending with rising impairment charges. The CBNŌĆÖs revised forbearance framework, designed to ensure earlier recognition of non-performing exposures and enhance asset quality transparency, has prompted lenders to reassess credit risks more aggressively. This has led to higher provisioning across the industry, particularly among banks with large exposures in oil and gas, trade, and small business lending.

While this has pressured short-term profitability, analysts argue that higher impairment recognition will improve long-term balance sheet resilience. It also positions banks more favourably for the anticipated credit cycle, as stricter provisioning today reduces the risk of future earnings shocks.

Meristem notes that the rising impairments were widely expected, especially with the gradual removal of pandemic-era regulatory accommodations and increased scrutiny of restructured loans. The combination of normalised earnings, stable currency dynamics, and improved provisioning discipline suggests the sector is shifting towards a more sustainable performance model, even if near-term returns appear softer.

Read also:┬ĀNigeriaŌĆÖs banks talk sustainability, but are they walking the walk?

Monetary easing to set the tone for 2026

Expectations around further monetary easing in 2026 are strengthening, with analysts forecasting deeper cuts to the benchmark rate if inflation continues its downward trajectory. Lower ratesŌĆöpaired with moderated CRR levelsŌĆöwould create a more accommodating environment for banks to expand credit to the real economy.

For corporates, a lower cost of borrowing could spur investments, particularly in sectors where high financing costs have constrained expansion plans. For banks, the anticipated rise in working capital lending, project finance transactions, and retail loans could support a recovery in net interest margins (NIMs), provided asset quality risks remain contained.

The financial system could see a healthier alignment between interest-earning assets and risk management practices, reversing the distortions created by the 2024 FX-driven profit cycle. The focus is shifting from extraordinary gains to operational fundamentals: loan pricing efficiency, digital banking expansion, cost control, and capital adequacy.

A cautious but improving outlook

While the uptick in customer loans to N42 trillion signals improving credit conditions, analysts warn that the pace of growth remains modest relative to NigeriaŌĆÖs economic needs. Banks remain cautious due to elevated default risks, persistent macroeconomic uncertainties, and thin capital buffers at some lenders.

However, the shift in monetary policy, improved FX stability, and declining inflation provide favourable tailwinds for stronger credit expansion in the coming year. The banking sectorŌĆÖs transition into a more normalised earnings terrain is expected to yield more predictable, stable, and risk-balanced growth.

For now, the data shows an industry cautiously returning to its core function: providing credit to the economy. And with monetary easing poised to continue, NigeriaŌĆÖs biggest banks may be gearing up for their most active lending cycle since before the pandemic.