African markets are sending mixed but increasingly stabilising macro signals: South Africa has paused its rate-cut cycle despite easing inflation, more economies are returning to single-digit price growth, ratings actions are reshaping risk perception around sovereigns and multilaterals, and cross-border bank expansion is drawing closer scrutiny from credit agencies.

Here’s what matters this week across finance in Africa.

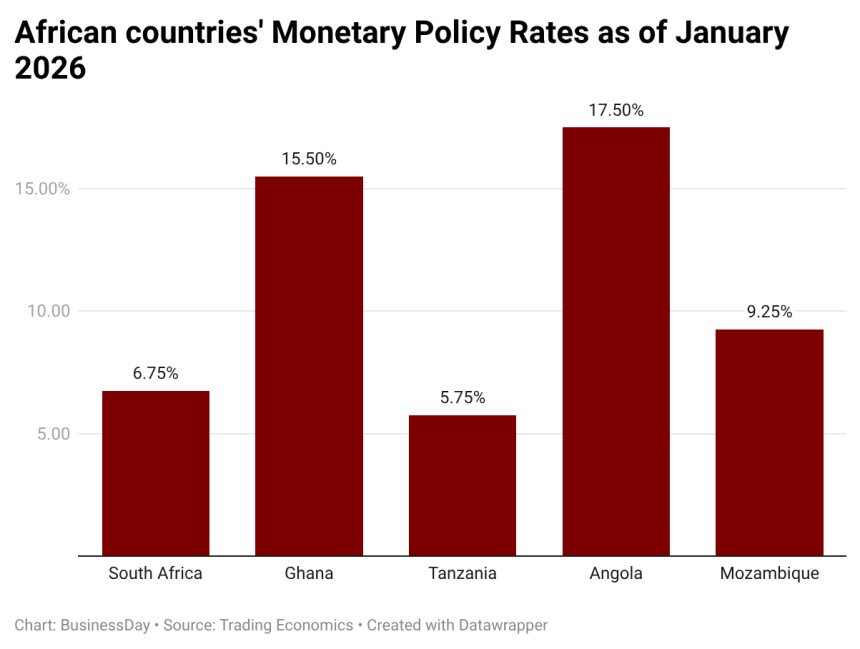

South Africa holds rates as inflation outlook improves

Unlike African peers such as Ghana and Angola that have moved more aggressively to loosen policy, the South African Reserve Bank kept its benchmark interest rate unchanged at 6.75 percent, pausing its easing cycle as inflation risks moderate but global uncertainty remains elevated.

The Monetary Policy Committee voted 4–2 in favour of a hold — the first pause since September 2025 — after cumulative cuts of 100 basis points over the past year from 7.75 percent. Governor Lesetja Kganyago said the decision reflects a slightly improved inflation outlook and a firmer currency, while signalling a more cautious forward stance.

Signal: Policy patience is taking priority over rapid easing in Africa’s most developed financial market.

Fitch withdraws Afreximbank ratings, cuts credit assessment to junk

Fitch Ratings has withdrawn all ratings on African Export-Import Bank for commercial reasons after ending its rating relationship with the Cairo-based lender.

Alongside the withdrawal, the global rating agency downgraded its credit assessment to BB+ (junk) from BBB-, with a stable outlook, following a dispute with the bank. The move comes as Afreximbank plays a larger role in sovereign debt workouts and trade finance support across the continent.

Signal: The action complicates investor risk benchmarking for one of Africa’s key multilateral lenders.

Single-digit inflation returns across more African economies

A growing number of African economies are re-entering single-digit inflation territory, marking a gradual macro stabilisation shift after years of price shocks.

Over the past five months, Ghana, Ethiopia, Zambia and Zimbabwe have all returned to single-digit inflation, driven by tight monetary policy, currency stabilisation and reform programmes backed by multilaterals. They now sit alongside relatively stable peers such as South Africa, Kenya and Tanzania.

Signal: Disinflation is reopening room for selective rate cuts and improving local bond market sentiment.

Nedbank’s $856m NCBA deal raises risk exposure — Moody’s

Moody’s says Nedbank Group’s planned R13.9 billion ($856 million) acquisition of a 66 percent stake in NCBA Group will increase the lender’s exposure to higher-risk African markets.

According to Moody’s, the deal raises sensitivity to macro volatility, SME credit risk and foreign-exchange movements in jurisdictions with weaker intrinsic credit profiles than South Africa.

Signal: Pan-African banking expansion continues — but with higher capital and risk-weight consequences.

Kenya upgraded by Moody’s as default risk eases

Moody’s upgraded Kenya’s sovereign rating to B3 from Caa1, its highest level since July 2023, citing reduced near-term default risk and stronger external liquidity.

The outlook was revised to stable, supported by higher foreign-exchange reserves, a narrower current-account deficit, improved exchange-rate stability and better market access. The upgrade comes ahead of a planned up to $2bn Eurobond issuance following liability-management operations.

Signal: Rating momentum is improving for reform-aligned sovereigns regaining market access.