Addressing issues around financial inclusion and financial literacy Ugo, founder of Nairametrics said the type of financial inclusion growth expectation needed for a country cannot be achieved without commensurate financial literacy so, before getting someone to maybe want to do transactions on the internet they have to at least have a little bit of financial literacy or a bit of a financial background about why they have to do transactions on the internet.

“If you want to teach somebody how to probably save towards the future, that person has to have a little bit of financial literacy. So they have to go hand in hand and that is where the government has to take it a bit seriously, so you cannot do financial inclusion without financial literacy so, programs like what ‘Financial Inclusion Today’ is doing currently is quite great because what it means is that you are gradually getting people’s attention and then finding a way to introduce financial inclusion through financial literacy. So they really go hand in hand,” the guest explained.

When the CEO of Nairametrics was asked to share his views on the major bottlenecks to deepening financial inclusion in Nigeria, he said there are a number of them. He cited trust issues, as although it may be surprising to many Nigerians, that there are still a lot of trust deficit when it comes to financial inclusion.

“When I say financial inclusion I mean adopting most of the financial products out there that can help them save better, I will give you an example, I was on one of my shows and we had this debate on whether to use one of the Fintechs apps you have to save money, and regular people like us, the 9-5 guys were calling in to say they will rather use the traditional “kolo” than use the Fintechs. So, there is trust deficit, people want to jealously hold on to their wealth or cash, we need to break that down”.

On other barriers that are preventing the inclusion of many excluded Nigeria into the financial cycle the guest said there are also the structural issues, especially in the villages or the remote areas of Nigeria where they have issues of the internet, without very good internet access which makes it really difficult to get access to financial inclusive products.

“They have issues of transportation, we also have disposable income issues – people are really poor, a guy who earns by the day actually has nothing to save and does not have the need for financial inclusion,” he mentioned.

Other points deliberated on were how financial inclusive products are also not that cheap, people who are into financial inclusion also at some point have to recover some of their money.

Projects like the Bill and Melinda Gates foundation are seen to bridge and soften or help at least a lot of people in the remote areas get access to financial inclusion.

“There are regulatory issues as well, a lot of the start-ups and companies that have gone into and trying to help financial inclusion, they have also had challenges scaling, it is very difficult serving population in remote areas because you have to have infrastructure, people, training in those areas and also the ease of doing business issues around those areas, there has been a lot of challenges but so far so good, we are seeing progress, there is a lot more awareness and if you look at data from the CBN or NBS, ATM adoption is increasing, people rely less on cheques, internet penetration is doing better, people are doing a lot more transactions over the internet also the USSD applications that people use. So we are seeing a bit of progress but then our challenges remain,” Ugo explained.

When Ugo was asked if Nigeria should follow in line of Kenya which has made tremendous success in the area of financial inclusion using the MPESA,

He said “I am not one of the great converts because of MPESA, I mean, MPESA has done great things but that is for Kenya. Nigeria is totally different and our payment infrastructure gateway is completely different, in fact I actually think we are more advanced but what MPESA and Kenya has done is that they have been able to rely on telecommunication infrastructure like GSM to spur financial inclusion,”

“Initially, the CBN felt like the best way to go about financial inclusion was to promote branch expansion so you had a lot of branches all over the country. There was a race to open branches from local banks and then at some point they realised that you are closer to the people but we are not seeing a lot more adoption and the world is changing as it is. We now had the internet boom, although was a bite difficult at the beginning , smartphones were expensive, but now we are seeing that smartphones are actually lot cheaper, a lot of people are a lot more into social media so you have social media financially inclusive products,” he said.

Ugo of Nairarmetrics said MPESA is good, as it showed that if one actually focuses on a particular area, it can actually have a lot of people adopt it so when building financial inclusive products, one have to build it to what they are actually used to.

“For example, if you are going to build a fintech product that people are going to use, build it around what they are used to, so currently a lot of people are used to cheap smartphones or phones that are actually not smart (phones that you can buy at N2000, N2500, are you going to provide financially inclusive products that rely on the internet solely or are you going to use the USSD? So, you are going to have a plethora of all these products available to them for us to adopt,” he added.

He concluded his reply to the question by saying that Kenya is doing a good thing but personally he feels Nigeria is doing a lot better.

When the guest was asked tools or strategies players in the financial inclusion sector like stakeholder, financial institutions the Nigerian government can use to drive financial literacy in the informal sector, and particularly agriculture, he responded by saying;

“I think one thing that is important is that we got to put things into perspective, so what exactly is the target, what do you expect from the participants of the agricultural sector. Do you want a particular percentage adoption; we need to have these bench marks to know how we measure them. To answer your question directly, financial literacy is not like you have people in a class then you start to preach to them, you have to find a way to get to them in a way or language that they can understand or in an area within their comfort zone. These guys also are a community like you and I,”

“So there areas where they sit down together and have discussions about life, their business, so you can actually take financial literacy to them, look at what they listen to, maybe they listen to radio, they watch TV I mean, they do something with their social life, you can actually get financial literacy to them through those means as well. On social media, a lot of these guys are on whatsapp groups that we belong to, or Facebook groups, so you can push financial literacy through those mediums as well,” he explained.

Meanwhile, Financial literacy according to the CBN may be defined as the possession of knowledge or skill by individuals to manage their financial resources effectively to enhance their economic wellbeing. It also enables financial service providers to better understand their products, the associated risks and the needs of their customers.

On who should drive financial literacy Ugo said “I think that everybody has a responsibility to play in driving financial literacy, however, you have people with primary responsibility and people with secondary responsibility. So I will always advocate for private sector driven initiatives especially when it is profit motivated. I feel you have no choice than to do it actually well. In terms of leading the fore front of financial literacy, I believe business news sites like BusinessDay and Nairametrics should be in the fore front of driving financial literacy because, by virtue of what you do, by reporting business news, you currently are in touch with the private sector, and the business world in general so you understand the language of business and you can communicate better with the people that we want to adopt financial literacy. I think our schools also, we have to start from the foundation, we need to get our schools involved, let us get financial literature courses, within not just our tertiary and secondary schools but also from primary schools,”

“In a nutshell financial literacy basically is just teaching you how to save, how to manage your expenses, how to invest and live a fulfilling life as you grow older. It sort of covers every facet of your life so you have to start from the schools as well”. He elaborated.

“In terms of secondary responsibility, now comes from the people that benefit from the wide adoption of financial literacy, we are talking about banks, quoted companies, governments as well, and of course medium like the media, religious institutions. Make no mistakes about it, you can’t have a developed economy without a population that is not financially literate, it is not going to happen. In a financially literate economy, they are the kind of people that provide capital that the economy needs to grow. For example the Nigerian stock market as a percentage of our GDP, it is probably in the range of 8, 9 percent which is very paltry, so what it means is that a lot of people don’t even have enough capital to take Nigeria where it should be. They don’t have capital to do research and development, to hire the best people around, they don’t have capital to build, to innovate and to get that kind of capital you get to pull it from everyone, so if you and I are not financially literate you actually don’t see a reason to invest in a stock or any reason why you should put your money in the bank or any reason why you should actually save, have a pension fund. There is a spectrum of responsibility out there but as I said, I think it starts with the media then you now go to schools,” the guest stressed.

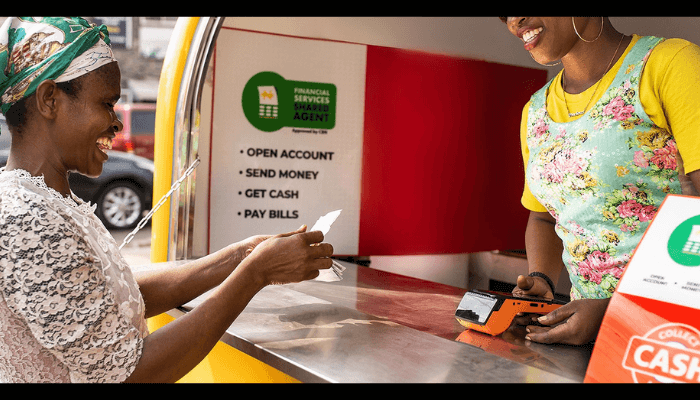

On the factors limiting women from the financial cycle, the founder of Nairametrics said “the irony is that women are going to be the easiest converts of financial literacy as compared to men, but the participation rate of women are low is also symptomatic on how we are in Nigeria in terms of the work place, you go to a regular work place, it is probably 8 to 2 or 7 to 3 at most in terms of male to female workers so that also transcends all the way to financial inclusion. I think if we continue to give women chances in terms of career and give equal opportunities if not better opportunities than men then you can start to see that filter into financial inclusion,”

“So I think there is got to be a way we can key into turning that disadvantage into an advantage for financial inclusion so the fact that you don’t have a proper balance between men and women in terms of career as it is skewed towards men then it means that it is probably easier to convince a lot more women who are just about coming up to adopt financial inclusion and financial literacy from the get go or from the foundation. Once that is done, it is easier to get them, to get their kids to adopt financial literacy and financial inclusion and then to get their husbands as well so the multiplier effect of actually getting a woman is a lot more than converting a man. Yes, it’s a disadvantage but I think it is something that we can easily turn into an advantage for us so,” he concluded.