In the heart of Nigeria’s financial district, where the pulse of the nation’s economy beats in charts and tickers, a quiet revolution has begun.

The Securities and Exchange Commission (SEC) is sitting at the centre of this shift, observing a world that had grown far more complex than the one for which its old rules were written since 2015. Interestingly, the window to either stay or exit is open for just 18 months.

Why the sudden hike?

The directive for an increased minimum capital is very clear: the capital market operators – the brokers, dealers, issuing houses, fund managers and other operators in the market who act as the nervous system of investment – need more muscle. The capital raise isn’t just about higher numbers on a balance sheet; but it is about survival in an era of unprecedented volatility.

From a competitive standpoint, the recapitalisation puts the nation’s market on the map. Global portfolio managers, who move billions of dollars with the click of a button, look for markets where the intermediaries are stable.

No doubt, the SEC decision to mandate recapitalisation was born from a realisation that the previous capital buffers were relics of a past era. In 2026, the risks are no longer just local; they are systemic and digital.

“The revised Minimum Capital framework seeks to: enhance the financial soundness and operational resilience of market operators; align capital requirements with the scope, complexity, and risk exposure of regulated activities; promote market stability and systemic risk mitigation; and support innovation and orderly development of new market segments, including digital assets and commodities markets”, SEC said in a January 16 circular to market operators.

By raising the minimum capital requirements, the SEC wants to ensure that firms have the “skin in the game” necessary to absorb sudden shocks. This is because without this financial bolster, a single major default or a flash crash could trigger a domino effect, thereby toppling smaller, undercapitalised firms and eroding the hard-earned trust of the investing public.

Globally, the tide has been shifting toward “prudential regulation” for years. From the post-2008 reforms in New York and London to the modern digital asset frameworks in Singapore, regulators are demanding that market participants be more than mere middlemen; they must be fortresses of stability.

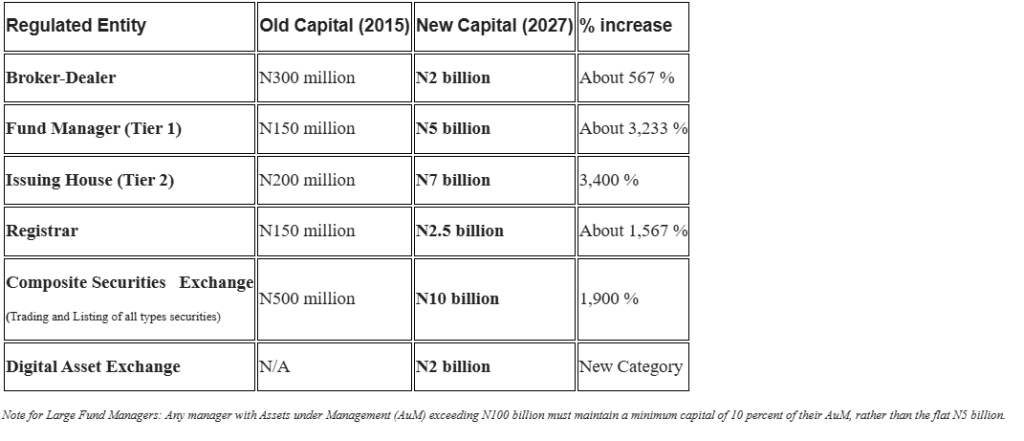

The most critical shifts: Increases range from a 100% rise for some to over 3,000% for others…

Note for Large Fund Managers: Any manager with Assets under Management (AuM) exceeding N100 billion must maintain a minimum capital of 10 percent of their AuM, rather than the flat N5 billion.

For instance, Tier-1 Portfolio Managers ((Full Scope) who are involved in: Management of Collective Investment Schemes (CIS) and Alternative Investment Funds (Private Equity, Venture Capital, Infrastructure Funds etc) above N20 billion Net Asset Value (NAV); discretionary and Non-Discretionary Private Portfolio Management Services above N20 billion Assets under Management (AuM); exposure to foreign instruments up to 40 percent of the NAV are now required to have a minimum capital of N5billion as against N150 million.

“Any Fund and Portfolio Manager with NAV/AuM of more than N100billion should have a minimum of 10 percent of the NAV/AuM as capital”, SEC added.

For the Tier-2 Fund/Portfolio Managers (Limited Scope) who are into: Management of Collective Investment Schemes with limited pooled fund creation of not more than 10 times the required capital (N20 billion) on Net Asset Value (NAV); Discretionary and Non-Discretionary Private Portfolio Management Services of not more than N20 billion; and exposure to foreign instruments of not more than 20 percent of the NAV, they now require N2billion as minimum capital as against low of N150 million.

Likewise, Broker-Dealer whose services include: client execution, proprietary trading, margin/securities lending and advisory services no longer require N300million minimum capital to operate but N2 billion.

Weeding out “fragility”…

The Nigeria’s SEC’s move aligns perfectly with this global trend, signalling to international investors that the local market is no longer a “frontier” playground but a sophisticated, well-guarded arena where their capital is protected by robust institutional frameworks.

The minimum capital requirement for Nigeria’s market operators, according to the SEC is informed by the need to strengthen market resilience, enhance investor protection, align capital adequacy with the evolving risk profile of market activities, and ensure that regulated entities possess sufficient financial capacity to discharge their obligations in a sustainable manner.

The SEC circular was sent to all entities regulated by the Commission, including but not limited to: core and non-core capital market operators; market infrastructure institutions; capital market consultants; financial technology (FinTech) operators; Virtual Asset Service Providers (VASPs); and Commodity market intermediaries.

All affected entities are required to comply with the revised Minimum Capital Requirements on or before June 30, 2027 a development seen to usher in era of mergers and acquisitions (M&A) in the market.

“Entities that fail to meet the prescribed requirements within the stipulated timeline shall be subject to appropriate regulatory sanctions, including suspension or withdrawal of registration, as may be determined by the Commission,” SEC said.

Looking further at the new required minimum capital, Tier 1 – Issuing House who do Non-Interest Finance services, Advisory & Arrangement services, and No underwriting now require N2billion as against N200 million; while Tier 2 –Issuing House with Underwriting and offers a ‘one-stop-shop’ for issuers, provides underwriting services, and renders advisory and product development services require N7billion minimum capital for this business as against N200million.

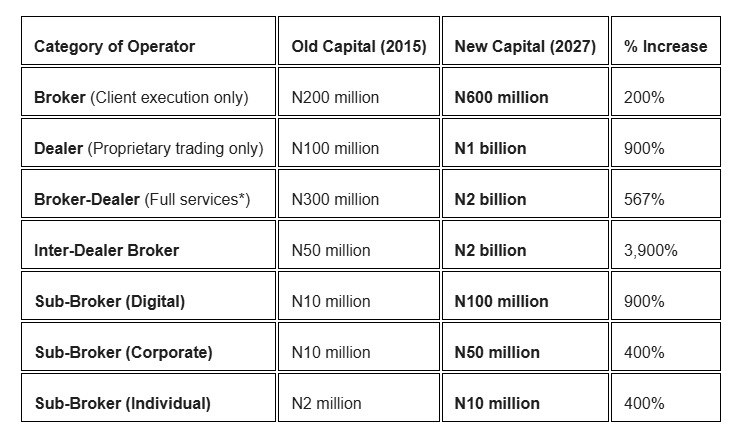

The minimum capital requirement for Broker (client execution only) has been jacked up from N200 million to N600 million; Dealer (proprietary trading only) from N100 million to N1 billion; Broker-Dealer (client execution, proprietary trading, margin/securities lending and advisory services), from N300 million to N2 billion; Sub-Broker (Digital) from N10million to N100million; Sub-Broker (Corporate) from N10million to N50 million. Also, Sub-Broker (Individual) now need N10million minimum capital for this business as against N2million while Inter-Dealer Broker requires N2billion as against N50million.

This recapitalisation is particularly vital for the protection of the retail investor—the everyday person putting savings into the market.

When a market operator is well-capitalised, the firm has the resources to invest in better technology, stronger internal controls, and superior cybersecurity.

In an age where digital assets and algorithmic trading are the norms, a firm with a tiny capital base is a liability. By forcing a higher standard, the SEC is effectively weeding out “fragility” and ensuring that only the most resilient and professional entities handle the public’s wealth.

The ripple effects…

The ripple effects of this policy extend far beyond the stock exchange floor. A stronger set of market operators acts as a catalyst for the broader goal of a $1 trillion economy. Large-scale infrastructure projects, such as power plants and rail networks, require massive long-term funding that only deep, liquid capital markets can provide. A well-capitalised issuing houses and underwriters are the only ones with the financial capacity to lead these multi-billion-dollar deals, bridging the gap between idle savings and national development.

Furthermore, the regulatory move encourages a healthy wave of consolidation. In the past, the market was saturated with hundreds of small players, many of whom struggled to innovate or provide quality service.

Through mergers and acquisitions (M&As) to be triggered by these new requirements, the industry will be witnessing the birth of “super-operators.”

These larger entities benefit from economies of scale, allowing them to lower transaction costs for clients while providing a wider array of sophisticated financial products that were previously out of reach.

Innovation is the other side of the recapitalisation coin. With a larger capital base, operators are finally empowered to embrace the “FinTech” revolution fully. They can afford to develop proprietary trading platforms, integrate AI-driven robo-advisory services, and explore the tokenisation of real-world assets. The SEC’s framework specifically includes new categories like Virtual Asset Service Providers (VASPs), recognising that a modern market must be large enough—and rich enough—to regulate the future of finance.