As 2026 approaches, the nation faces cautious optimism, yet beneath the surface, its economy undergoes a critical stress test. Recent analysis from market experts and policymakers agree: recovery now depends not just on growth numbers but on resilience under changing pressures. While macroeconomic reforms, FX liberalization, and fiscal adjustments have boosted credibility, they have also uncovered underlying structural vulnerabilities that might worsen in the coming year.

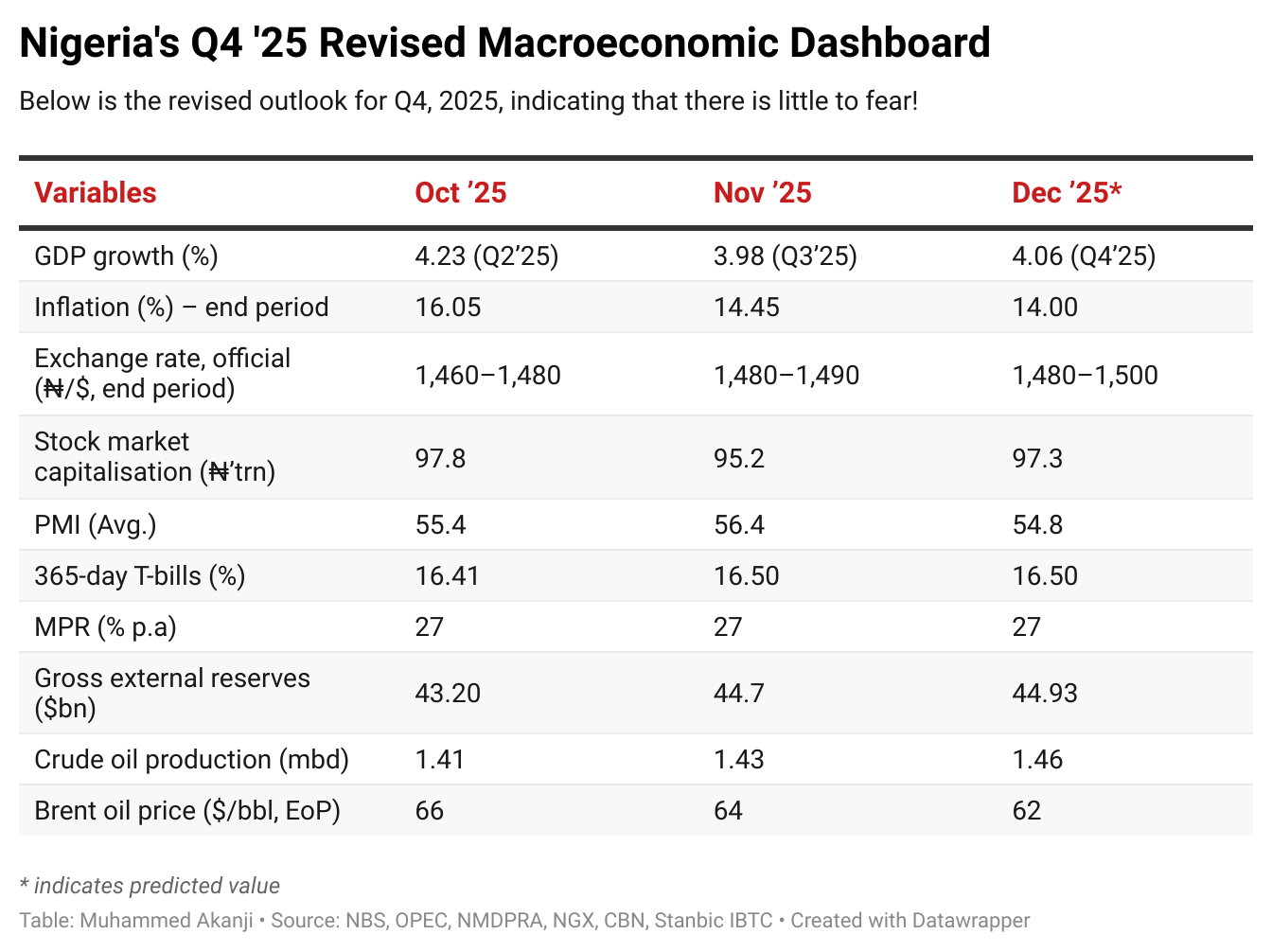

Headline GDP growth is expected to remain positive, supported by services, modest oil recovery, and pockets of non-oil expansion. But this growth masks persistent vulnerabilities. Inflation remains mildly elevated and sticky (now at 14.45% for Nov.’25), with food prices especially sticky, eroding household welfare. Debt service continues to absorb a dominant share of government revenue, limiting fiscal space just as social and infrastructure demands intensify. Oil production assumptions- still hovering around 1.6-1.8 million barrels per day- remain a critical swing factor in a volatile global energy market.

At the same time, FX stability rests on fragile foundations: reserve buffers, portfolio flows, and oil receipts must align in a year when global financial conditions may tighten. For businesses and households alike, 2026 will test whether recent reforms translate into jobs, lower costs, and improved confidence- or whether Nigeria’s long-standing pressures reassert themselves. The question is no longer whether growth will return, but where the system is most likely to bend- or break.

Fiscal atress & the debt trap: Can revenues keep up with debt service?

Nigeria’s fiscal outlook for 2026 is increasingly shaped by a key constraint: debt service is outpacing revenues. Recent fiscal forecasts and analyst reviews indicate debt-service-to-revenue ratios frequently reaching crisis levels- often above 80% in recent years- leaving little room for development spending. While headline debt-to-GDP remains moderate by global standards, Nigeria’s main vulnerability lies in weak revenue mobilisation rather than excessive borrowing.

FX-denominated liabilities compound the risk. A significant portion of external debt is denominated in dollars, so exchange-rate volatility automatically raises debt-service costs whenever the naira depreciates. This creates a feedback loop: FX pressure raises debt service, debt service crowds out capital spending, and underinvestment slows growth and revenue expansion.

Subsidy risks further complicate the picture. Although fuel subsidies were formally removed, fiscal documents and analyst notes warn of implicit re-emergence through under-recovery mechanisms, which could quietly reopen a major drain on public finances. At the same time, rising personnel costs and security spending squeeze already thin fiscal space.

The result is capital crowd-out: infrastructure, health, education, and productivity-enhancing investments are sacrificed to keep the government solvent. Unless revenue reforms- tax efficiency, oil output stability, and non-oil exports- accelerate meaningfully, Nigeria risks stabilising debt on paper while sinking deeper into a functional debt trap.

Inflation, incomes & household strain

Even as headline inflation shows signs of moderation, the lived experience of Nigerian households tells a harsher story. Food inflation remains persistently high, driven by insecurity in key farming belts, logistics disruptions, climate shocks, and FX pass-through on imported inputs. For low- and middle-income households that spend 50–60% of their income on food, this keeps the cost-of-living crisis firmly in place, reducing the benefits of disinflation.

Wage growth has failed to keep pace. Outside a narrow segment of the formal sector, earnings remain largely stagnant, while real wages continue to decline. Minimum wage adjustments were implemented, lagging inflation, and are uneven across states, widening inequality between public and private workers. The result is purchasing power erosion: households are consuming less, trading down in quality, and deferring spending on health, education, and durable goods.

This income-inflation mismatch risks becoming a demand-side drag on growth in 2026. Without faster food price normalisation, productivity-led wage growth, and targeted social transfers, macro stability will remain statistical rather than social sensitivity, and naira pass-through risks.

FX stability & external vulnerability

Nigeria’s FX outlook in 2026 rests on a narrow and fragile base. External reserves have improved on a headline basis, but adequacy remains questionable when measured against import cover, external debt service, and portfolio-flow sensitivity. A large share of recent reserve accretion has been driven by short-term inflows rather than durable FX earnings, leaving the naira exposed to sudden reversals if global risk sentiment tightens.

Oil receipts remain the key swing factor. Production assumptions continue to outpace historical performance, while price volatility and pipeline risks threaten revenue predictability. Any shortfall quickly transmits into FX markets, given Nigeria’s heavy import dependence for food, fuel inputs, and industrial goods. The result is high naira pass-through risk: exchange-rate movements feed rapidly into inflation, raising costs for households and businesses alike.

Portfolio flows add another layer of fragility. Elevated domestic yields attract hot money, but these inflows are highly sensitive to global interest-rate shifts and geopolitical risk. In 2026, FX stability will depend less on administrative controls and more on reserve buffers, credible oil output, and sustained confidence.

Growth without jobs: The productivity gap

Nigeria’s growth story is increasingly at risk of becoming job-poor. While GDP expansion is expected to remain positive into 2026, employment growth continues to lag, reflecting deep structural weaknesses in productivity. Much of recent growth has been driven by services and informal activities with low employment elasticity, offering survival incomes rather than sustainable livelihoods. Manufacturing and agro-processing—sectors that historically absorb labour at scale—remain constrained by high energy costs, logistics bottlenecks, FX shortages, and limited access to long-term finance.

The result is increasing informalization. New workers entering the job market are often placed in low-productivity roles with minimal capital or skills development, which weaker income growth and domestic spending. Even when output increases, value added per employee stays flat, hurting competitiveness and export prospects. This gap explains why overall growth hasn’t led to widespread improvements in living standards.

Unless Nigeria unlocks productivity through industrial policy, skills development, and investment in value chains, 2026 risks repeating a familiar pattern: growth that looks encouraging on paper but leaves unemployment, underemployment, and working poverty largely untouched.

Security, climate & supply-side shocks

Shocks outside the traditional fiscal and monetary toolkit will increasingly shape Nigeria’s macro-outlook in 2026. Persistent insecurity- banditry in the North-West, insurgency in the North-East, and farmer-herder conflicts across the Middle Belt- continues to disrupt agricultural cycles, raise food prices, and constrain rural livelihoods. These security pressures intersect with climate stress: flooding, droughts, and erratic rainfall are reducing crop yields, damaging infrastructure, and deepening food supply volatility.

Logistics disruptions compound these risks. Insecure transport corridors, damaged rural roads, and climate-related infrastructure losses raise distribution costs and widen regional price disparities. The result is a fragile supply chain where local shocks quickly translate into national inflation spikes, especially for food, which dominates household consumption.

Insecurity and climate risks together act as macroeconomic amplifiers, weakening growth, fueling inflation, straining public finances, and increasing reliance on imports. Without coordinated investment in security, climate adaptation, and resilient logistics, supply-side shocks will continue to undermine stability.