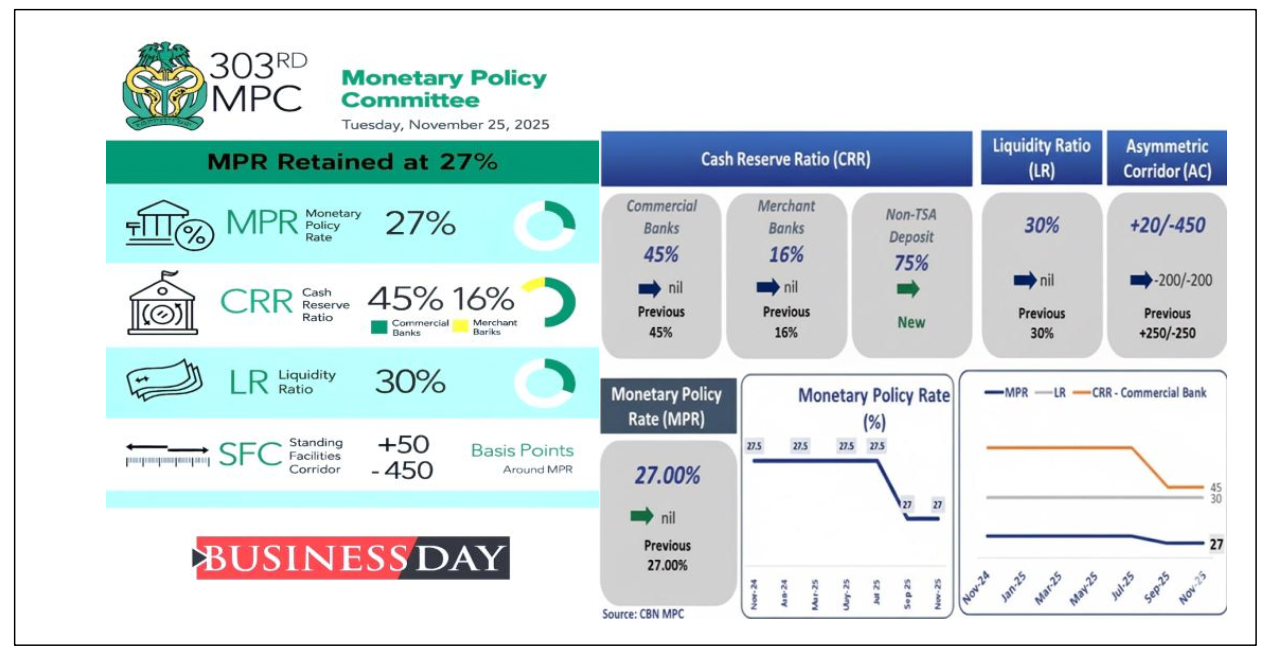

Following its two-day meeting that concluded on Tuesday, November 25th, 2025, the CBN’s Monetary Policy Committee (MPC) kept the Monetary Policy Rate (MPR) at 27%. It seems the central bank aimed to maintain strict monetary control over the economy, although the asymmetric corridor at +50/-450 basis points from the September meeting, compared to the previous +250/-250bps, provides some reassurance. This decision surprised many analysts after months of easing. Inflationary pressures have been exceptionally high because credit conditions remain tight, and small businesses continue to borrow at double-digit rates. The committee also kept the Cash Reserve Ratio at 45 percent for deposit money banks, 16 percent for merchant banks, and 75 percent for non-TSA public-sector deposits.

While the CBN maintains that holding the rate steady is essential for maintaining inflation control and FX stability, analysts warn that a prolonged tight stance could slow economic growth, restrict private-sector credit, and extend the business liquidity crunch.

As the festive season approaches and liquidity remains constrained, the real economy teeters between price stability and stagnation.

So, the question investors and businesses must ask is: Can the CBN hold the line without choking growth, or is this pause the calm to forestall a possible downturn given the fragile nature of the current recovery?

The Logic Behind the Pause

Beneath the surface of the CBN’s November rate hold lies a complex macro landscape that remains unsettled. Therefore, the MPC’s decision acts as a strategic pause aimed at balancing two competing realities: slowing inflation and stabilizing the exchange rate, along with a still-fragile economic recovery. Recent data shows headline inflation easing from earlier highs, month-to-month pressures moderating, and FX market liquidity improving as reserve buffers stabilize.

These gains, though modest, suggest that aggressive tightening may no longer be the most effective tool. While some analysts believed that there was no rate decision during the November round, many noted that holding rates could worsen the already weak credit conditions, especially for SMEs and manufacturers already borrowing at high rates. Questioning the disconnect between decreasing inflation and a stagnant interest rate, Mr. Eke Ubiji, the DG of the Nigerian Association of Small and Medium Enterprises, said, “Something is wrong somewhere. There’s no correlation. If inflation is decreasing every month but the interest rate remains unchanged, then something is wrong somewhere. If the interest rate is at 27 percent, then what is the cost of borrowing?”

Meanwhile, the Organised Private Sector (OPS) welcomed the hold, arguing that previous tightening cycles had entrenched a semblance of stability and predictability in the economy, noting that the CBN was trying to “consolidate the existing gains” according to Mr Gabriel Idahosa, the President of Lagos Chamber of Commerce and Industry (LCCI)

Although inflation eased for seven consecutive months in October, the MPC’s decision to hold the rate was based on the notion that inflation is still elevated, especially core inflation, necessitating sustained policy tightening to further moderate price pressures.

By maintaining rates, the CBN signals confidence that disinflation may be taking root, while also avoiding additional strain on lending and investment. The pause also reflects caution: FX inflows remain uneven, festive-season demand could reignite price pressures, and structural bottlenecks continue to limit transmission.

Other Macro Reality Checks: FX and Liquidity Pressures

Besides the above, core inflation components stay stubborn, showing ongoing structural pressures—energy costs, logistics delays, and high food prices that monetary policy alone cannot resolve. We believe these underlying factors remain strong enough to challenge any lasting disinflationary slowdown.

Liquidity conditions remain tight. OMO issuances, Standing Deposit Facility (SDF) sterilization, and Standing Lending Facility (SLF) borrowing have collectively squeezed banking-sector liquidity, limiting credit expansion even with the policy rate unchanged. However, a slight adjustment to the asymmetric corridors now gives banks a short-term incentive to lend at a lower rate, which further discourages them from bringing funds to the CBN.

The rate hold might calm markets temporarily, but it doesn’t remove vulnerabilities. The key question now is whether this pause stabilises expectations or simply delays larger macro adjustments.

Winners and Losers: Market Reactions

The new rate announcement has produced a mixed market reaction, creating clear winners and losers across asset classes.

In the credit market, lending to SMEs and manufacturers remains weak. Bank loan growth has slowed sharply, with effective lending rates still above 30%, meaning the rate hold offers little relief for businesses already struggling with liquidity constraints.

In equities, banks became short-term winners. Investors saw the MPR hold as stabilizing for asset quality, boosting tier-1 bank stocks, which were already supported by strong FX revaluation gains earlier in the year. Telecom and consumer-goods stocks, however, remain under pressure due to high input costs and weak household demand.

In the fixed-income market, T-bill yields remained elevated, around 18-22% across key tenors, attracting defensive investors and further tightening liquidity. Bond yields also adjusted higher, reflecting expectations that tight policy may persist longer.

The FX market showed slight support, with the pause seen as the CBN’s effort to preserve naira confidence. However, we argued that risks still exist: festive-season demand and slow oil inflows could challenge stability.

Ultimately, the rate holds steady markets- but does it resolve underlying structural vulnerabilities, or simply buy time?

The Outlook

The CBN’s rate hold raises a defining question: Is this a stabilising pause, or the start of policy drift as fiscal pressures mount? While the decision may steady expectations in the short term, persistent core inflation, weak credit expansion, and fragile FX inflows could quickly erode its impact. Investors should closely track inflation trends, reserve buffers, FAAC inflows, private-sector credit growth, and FX market turnover to judge whether the pause strengthens credibility or exposes deeper vulnerabilities. The coming months will reveal whether the MPC has bought stability, or merely time.