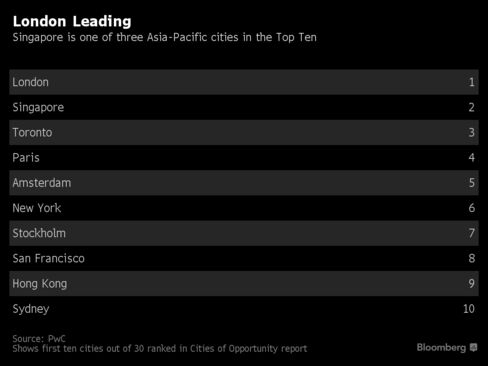

Singapore is next in line if London loses its status as leading business hub in the world.

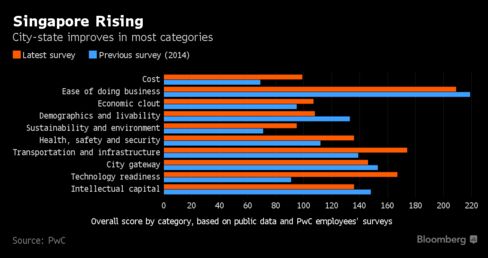

Superior technology, low taxes and efficient transport and infrastructure systems helped Singapore to overtake New York and move one notch higher in the rankings since the previous study in 2014, according to PwC.

Unlike other surveys that rank financial hubs based on their competitiveness, the PwC index assesses cities on their social and economic health too, measuring indicators such as the ease of doing business, demographics and technology readiness.

The results show Singapore’s growing business clout, driven in part by an expanding financial and insurance industry, which makes up about 13 percent of the economy.

Singapore leads its main Asian rival, Hong Kong, in categories such as ease of doing business, infrastructure and health, safety and security. Hong Kong dropped one spot in the overall index to ninth, partly due to a decline in the category measuring intellectual capital and innovation.

Few cities beat Singapore on taxes. The corporate tax rate of 17 percent compares with more than 30 percent in France, 35 percent in the U.S. and an average of 22.8 percent for the 35-member Organisation for Economic Co-operation and Development.

To be sure, the No. 2 spot on the index doesn’t mean Singapore will attract companies seeking to shift their operations out of London as the U.K. untangles itself from the EU. For a start, the city state has been tightening rules for foreign workers and has a perennial pollution problem from forest fires in Indonesia.

Ravi Menon, head of Singapore’s central bank, said Tuesday that businesses set up operations in Hong Kong and Singapore to tap Asian markets and Brexit may not dent London’s appeal as a financial hub.

“London will remain a major financial center,” he said. “At the margin there will some shift to other financial centers in Europe.”

Bloomberg