In the oil and gas business, cash isn’t just king; it’s survival. The industry is one of the most capital-intensive in the world, requiring billions for exploration, drilling, production, and maintenance. Access to liquidity determines who can endure market shocks, finance new projects, and ultimately stay in business.

A glance at the financial statements of Nigeria’s listed upstream oil companies reveals just how cash-hungry this business is. Most operators rely heavily on bank borrowings to fund exploration and maintain production facilities. In fact, the capital needs of oil and gas projects are often too large for any single company to shoulder, prompting the formation of multiple joint ventures and syndicated partnerships.

As of the first nine months of 2024, Nigerian banks had a staggering N111.5 trillion exposure to the oil and gas sector, particularly the upstream segment. This underscores just how heavily leveraged the industry is.

The debt picture: Seplat, Oando, and Aradel

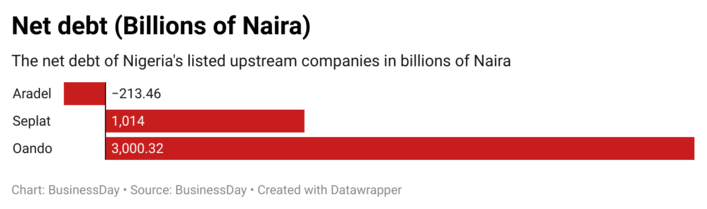

Take Seplat Energy, for example. The company’s books show a net debt of $676 million and a gross debt of $1.096 billion. In other words, even if Seplat used all its available cash and equivalents to pay off its borrowings, it would still owe about $676 million.

Oando’s situation is even more complex, with a net debt position of around N3 trillion (approximately $2 billion). But debt, in the oil business, isn’t necessarily a red flag; it’s about how well a company manages it. Analysts often look to the net debt-to-EBITDA ratio, a key measure of leverage that shows how much debt a company carries relative to its earnings.

For Seplat, the company’s self-imposed benchmark is a ratio of 2.0x, while its actual figure as of H1 2025 stood at 0.53x, well within range. Oando’s negative EBITDA makes its ratio meaningless. But then comes Aradel Holdings Plc, with a surprising twist: a negative net debt-to-EBITDA ratio.

Not because it’s making losses, but because it’s sitting on more cash than debt.

A rare position: Aradel’s net cash advantage

Unlike most upstream companies, Aradel has a net cash position of N213.5 billion. In plain terms, the company has enough cash to pay off all its liabilities and still have money left over. That’s remarkable for an operator that also runs a refinery and a gas processing plant, two ventures known for their heavy capital requirements.

So, the natural question arises: why is Aradel sitting on a pile of cash?

Read Also: Africa Capital Alliance exits Aradel Holdings with 3.4x return – Businessday NG

The case for prudence

Compared with global oil majors, Aradel appears distinctly underleveraged. For perspective, Shell Plc’s net debt-to-EBITDA ratio stood at 1.51x in H1 2025, Chevron’s at 2.5x, and Seplat’s at 0.53x. Using Seplat’s 0.53x as a leverage benchmark, Aradel could comfortably raise as much as N400 billion in new debt.

Being underleveraged isn’t inherently bad. In fact, some investors view it as a mark of financial discipline and resilience. However, for equity investors, the story is more nuanced.

According to Oluwaseun Magreola, Head of Investment Research at STL Asset Management, “Underleverage is a double-edged sword for equity investors. It reduces the risk of default or bankruptcy, allowing the company to withstand economic slowdowns better. But on the flip side, it can limit upside potential by lowering return on equity and suppressing valuation multiples, especially if peers achieve higher returns through prudent leverage.”

Yet, Aradel is delivering returns

Interestingly, Aradel has defied that logic. Despite its conservative balance sheet, the company is outperforming its peers on profitability metrics. In H1 2025, Aradel reported a Return on Equity (ROE) of 10.2 percent, compared to Seplat’s 1.5 percent. For full-year 2024, it posted a stellar 24.6 percent ROE, one of the strongest in the Nigerian upstream space.

If the company can achieve such returns while keeping its leverage this low, analysts argue it could unlock even greater value by judiciously deploying some of that idle cash.

A look at Aradel’s portfolio

Aradel’s asset base tells a story of vertical integration and operational depth. The company owns a 100 percent stake in the Ogbele Marginal Field (OML 54), operates a 100 million standard cubic feet per day gas processing plant, and runs the 11,000-barrel-per-day Aradel Refinery, all located within its Ogbele asset cluster in Rivers State.

Beyond that, Aradel holds an equity stake in Renaissance Africa Energy, the consortium that recently acquired Shell Petroleum Development Company (SPDC).

Despite this diverse portfolio, Aradel’s spending in H1 2025 appears modest. The company invested just N45.5 billion in new projects, about 31 percent of its half-year net income, compared to Seplat’s N179 billion in the same period.

To some observers, this signals underinvestment. But others see it as a strategic restraint.

According to Adebayo Adebanjo, an oil and gas analyst at CardinalStone, “They will sit on cash until they find viable opportunities to take advantage of. Aradel has different methodologies for assessing opportunities; they don’t rush into projects that don’t align with their long-term growth plan.”

The bigger picture

In an environment where Nigeria’s upstream sector faces declining investment, fiscal uncertainty, and volatile oil prices, Aradel’s prudence could be strategic. Holding a strong cash buffer gives it the flexibility to act quickly when opportunity knocks. This could mean acquiring distressed assets, expanding refining capacity, or deepening its stake in gas infrastructure.

But it also poses a challenge: how long can the company justify such a large idle balance in a growth-hungry industry?

Ultimately, Aradel’s cash-heavy stance reflects both strength and caution, a sign of a company preparing for the next big move rather than overextending itself in uncertain times.