Once the fabric that clothed a nation and supported livelihoods, the textile industry now tells a story of both decline and resilience. For decades, it stood as the pride of West Africa, employing hundreds of thousands and integrating itself into the country’s cultural and economic identity. Today, it still holds significant potential for job creation and non-oil diversification; however, its strength has diminished due to years of underinvestment, inconsistent policies, and a steady flow of cheap imports.

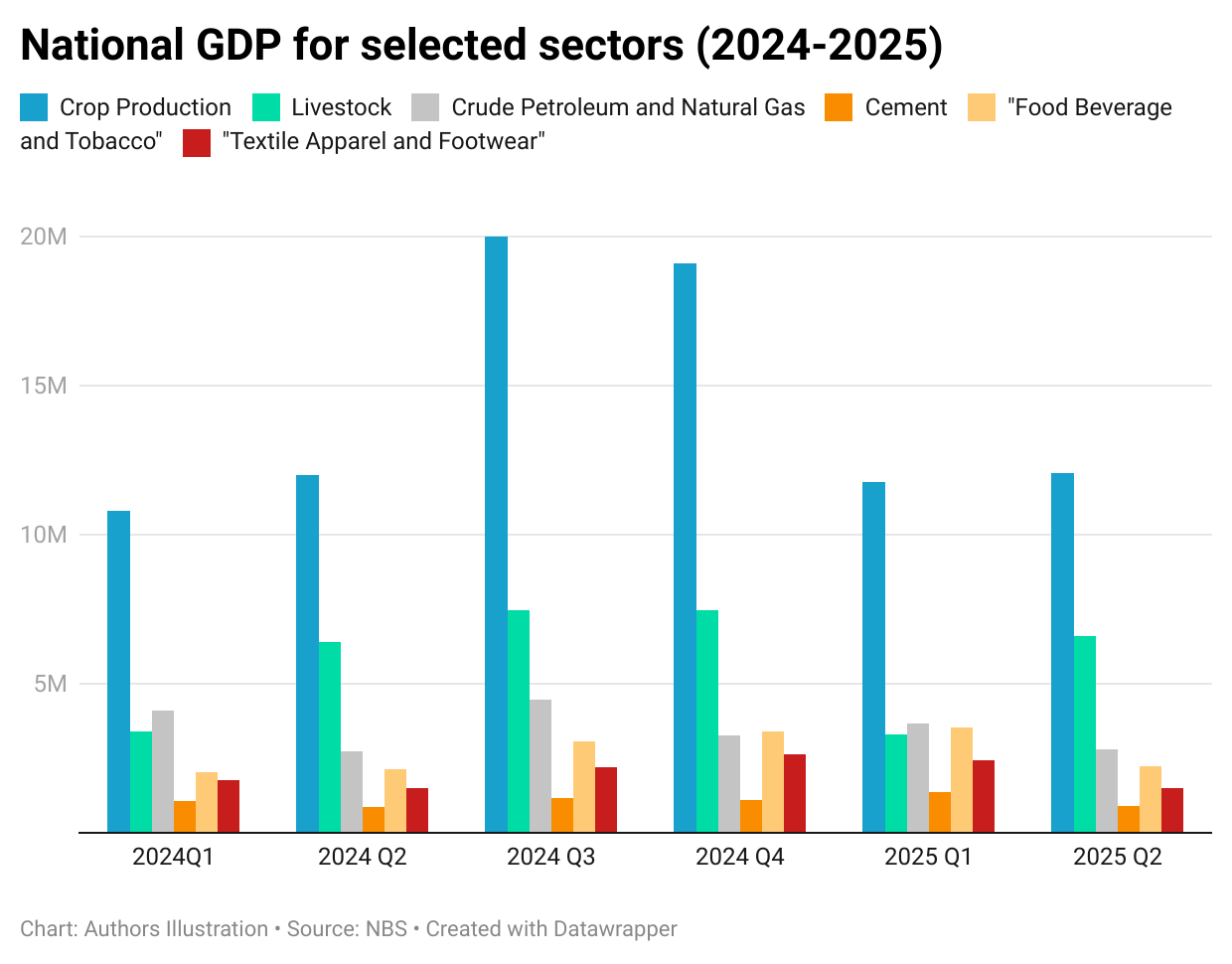

Nigeria’s sectoral GDP from 2024 Q1 to 2025 Q2 is led by crude petroleum and crop production. Textile, apparel, and footwear, however, remain at the bottom, contributing very little across all quarters. This poor performance underscores the ongoing challenges faced by Nigeria’s textile manufacturing sector, despite revival policies. The small GDP share signals limited industrial capacity, reliance on imports, and informal tailoring clusters that fail to generate measurable growth. Without increased investment, energy stability, and modernization of mills, the sector risks further marginalization in the national output.

Mapping Nigeria’s textile revival by region

Textile revival gathered pace between 2015 and 2017, when the government rolled out the Cotton, Textile and Garment (CTG) policy alongside the Central Bank’s Anchor Borrowers’ Programme to strengthen cotton farming and resuscitate mills. The Journal Nigeria notes that this drive was reinforced by the Nigeria Industrial Revolution Plan and subsequent measures through 2023–2025, though outcomes have been uneven. Informal clusters such as Aba and Lagos‑Ogun have flourished, while Kaduna’s integrated mills continue to face challenges. Output shares illustrate the balance of activity: Kano leads with 38%, Kaduna holds 26%, despite a decline, Lagos and Ogun consolidate 20% through garmenting and imports, and Aba’s tailoring hub contributes a resilient 14%.

Author’s creation

Nigeria’s textile industry shows resilience despite missed opportunities. Once a leading force in Africa, it now struggles with unstable policies. However, regional advantages suggest that targeted investments and reforms could drive a potential revival.

In the North, cotton remains the key industry. States like Kano, Katsina, and Kaduna have historically supported Nigeria’s textile mills. Industry experts suggest that reviving ginneries and linking them to modern factories could reduce reliance on imported fabrics. However, insecurity and poor logistics still disrupt the supply chain.

The South-East tells a different story. Aba in Abia State has become synonymous with mass production of garments and footwear. According to an industry analyst, millions of units are churned out annually, though most producers remain informal. Aba has the potential to become West Africa’s fast-fashion hub through improved branding and financing.

In the South-West, Lagos stands tall as Nigeria’s fashion capital. Designers and ready-to-wear brands are already eyeing AfCFTA markets, but access to credit and logistics support will determine whether these SMEs can scale.

The South-South offers another angle. With petrochemical plants in Delta and Rivers, there is potential to supply polyester and synthetic fibers locally. Linking these inputs to textile production could create a domestic synthetic fabric base, reducing reliance on imports. Together, these regional threads may yet weave Nigeria’s textile comeback.

Policy and productivity in government delivery

The government has launched revival schemes in the past, such as the Nigeria Industrial Revolution Plan (NIRP) and other borrowers’ programmes. Billions have been pledged to rebuild cotton farming and reopen textile mills, but progress has been uneven. Many promised investments have not translated into lasting factory output or stable jobs.

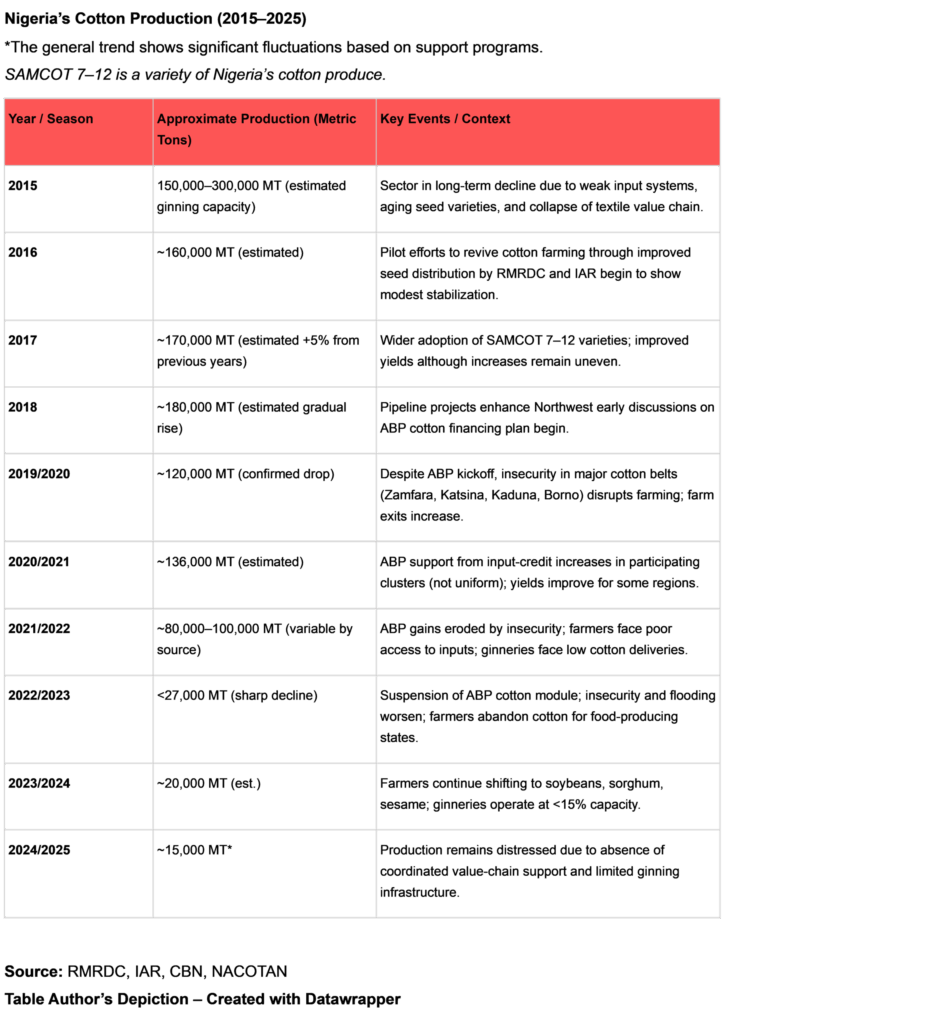

Cotton production fluctuated dramatically over the past decade, underscoring the sector’s fragility. In 2015, production fell to between 150,000 and 300,000 metric tons as ageing seed varieties and a collapsed value chain weighed heavily. A modest rebound followed in 2016 and 2017, driven by improved seed distribution and the adoption of SAMCOT 7–12 varieties. By 2018, private ginners had returned to northern states, lifting confidence and yields. That momentum was short‑lived: flooding in 2019/2020 slashed output to 120,000 tons. A brief recovery in 2020/2021 under the Anchor Borrowers Programme gave way to steep declines from 2021 onward, with insecurity and poor input delivery dragging production to a projected 15,000 tons by 2025.

The textile industry faces two main challenges: high foreign exchange rates and an unreliable power supply. Additionally, ineffective enforcement against textile smuggling weakens local producers. If the government can strengthen trade rule enforcement, ensure stable energy, and complete planned industrial zones, cotton could once again support a vibrant manufacturing sector.

Recovery Outlook

The textile industry faces a crossroads with two potential paths. In one, the cotton-growing belt in the North could become vibrant again, while Lagos’ growing fashion scene benefits from its design talent and access to diaspora markets. Aba’s production clusters, once better funded and branded, could take advantage of regional opportunities under the AfCFTA framework.

A more pessimistic view indicates continued stagnation, persistent insecurity in the North, unchecked textile smuggling, and unstable power reforms, all likely to sustain low productivity and dependence on imports.

The most promising winners include integrated cotton-to-garment value chains in the North, fashion SMEs in Lagos targeting regional and overseas consumers, and petrochemical-linked textile ventures in the South-South. Aba’s informal network of tailors and fabric traders remains in a holding pattern until it is better structured and scaled. Large mills, too, will only thrive if energy supply becomes more stable and affordable.

For investors, the best prospects lie in regional clusters with clear comparative strengths; cotton in the North, design and branding in Lagos, and synthetics in the South-South—each offering a different but connected piece of Nigeria’s textile comeback.