As Nigeria strides toward a digital future, its financial inclusion journey faces a paradoxical challenge: How can Nigeria change the fortunes of its unbanked adult population and revolutionise its economy through digital transformation? The answer may lie in reimagining digital identity systems—not merely as administrative tools but as catalysts for economic empowerment and financial inclusion.

According to the 2020 EFInA Access to Financial Services Survey, only 50.5% of Nigerians use formal financial services, leaving about 38 million adults financially excluded. This exclusion stems from several factors, but one fundamental barrier remains persistent: the identity gap.

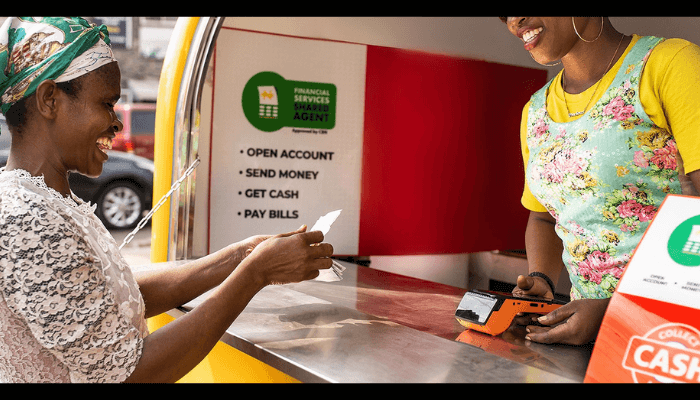

Without a verifiable identity, Nigerians cannot access loans, insurance, or even basic banking services.

The National Identification Number (NIN) initiative by the National Identity Management Commission (NIMC) has registered over 70 million Nigerians as of 2021, yet integration challenges between this system and financial services persist. The fragmentation of identity systems across multiple government agencies has created inefficiencies that disproportionately affect the poor and vulnerable.

Biometric Solutions and Global Precedents

Emerging markets facing similar challenges have demonstrated remarkable success through biometric identity solutions. India’s Aadhaar system stands as the world’s largest biometric ID

program, having enrolled over 1.2 billion citizens by 2021. Its integration with banking through the Jan Dhan Yojana initiative brought millions of previously unbanked Indians into the formal financial system. Similarly, Peru’s national ID system contributed to increasing financial inclusion. The key success factor in both cases was not merely the creation of digital IDs but their deliberate integration with financial services platforms.

Unlike traditional IDs, biometric systems offer particular advantages for Nigeria. Fingerprints and facial recognition bypass literacy barriers, essential in a country where adult literacy stands at approximately 63% in 2021. The biological uniqueness of biometrics significantly reduces identity fraud and duplicate registrations. Once enrolled, citizens can verify their identities anywhere with minimal infrastructure, making the solution ideal for a country with a significant rural population.

Balancing Privacy Concerns with Inclusion Benefits

The relationship between privacy and inclusion is often presented as an either-or proposition, but evidence suggests otherwise. A 2018 World Bank study found that well-designed ID systems can strengthen privacy protections without compromising inclusion. Strong data protection frameworks don’t hinder financial inclusion—they enable it by building trust and encouraging citizens to participate in digital financial systems.

Nigeria’s data protection landscape has evolved with the 2019 Nigeria Data Protection Regulation (NDPR), but implementation challenges remain. The limited capacity of regulatory bodies poses risks to proper enforcement while potentially stifling innovation if applied inconsistently.

Rather than pursuing a monolithic identity system, Nigeria could benefit from a federated approach, where multiple identity providers operate under common standards. This model has shown promise in countries like Estonia, where private and public entities collaborate within a standardised framework.

For Nigeria, this could mean allowing banks to serve as trusted identity verifiers with regulatory oversight, leveraging the extensive reach of mobile networks for identity verification, and implementing proportional verification standards based on transaction value and risk.

The Path Forward: Economic Implications and Stakeholder Roles

Achieving transformative change requires coordinated action across multiple stakeholders. Policymakers must streamline regulatory frameworks to eliminate contradictory requirements

across agencies and incentivise private sector participation through clearer guidelines. Financial institutions need to develop simplified onboarding processes that leverage existing identity

verification channels and create products specifically designed for newly identified customers.

Technology providers should focus on offline authentication mechanisms suitable for areas with poor connectivity while ensuring solutions are optimised for the low-cost smartphones

prevalent in Nigeria. The economic case for solving the identity-inclusion nexus is compelling. McKinsey estimates that digital IDs could unlock economic value equivalent to 3-13% of GDP in developing economies by 2030. For Nigeria, this represents potential economic gains of up to $59 billion annually.

As Nigeria positions itself as Africa’s fintech hub, resolving the identity challenge is not merely a technical matter—it’s an economic imperative. By implementing thoughtful, inclusive identity

systems that balance innovation with protection, Nigeria can transform the identity gap from a barrier to a bridge, connecting millions to the financial opportunities that have remained

tantalizingly out of reach.

The question is not whether Nigeria should pursue digital identity solutions for financial inclusion, but rather how quickly and effectively it can implement them. The technology exists.

The economic case is clear. What remains is the political will and cross-sector collaboration to make it happen.

About the author

Oluwaseun Yusuff is a Fintech and Payments expert, holding an MBA from the University of North Carolina’s Kenan-Flagler Business School in Chapel Hill. He writes from New York City.