| The stakes are high in Nigeria’s banking recapitalisation play. Some banks are immersed sundry “financial engineering” to comply with the Nigerian Central Bank’s (CBN’s) unusual definition of capital; Nova Bank has chosen a path that tracks least resistance – or easy survival. As the wind swung through the Kofo Abayomi head office of erstwhile merchant bank, Chairman Philips Oduoza, once at the helm at top-tiered United Bank for Africa, paced around his glass-enclose office, musing about this route to downgrade.

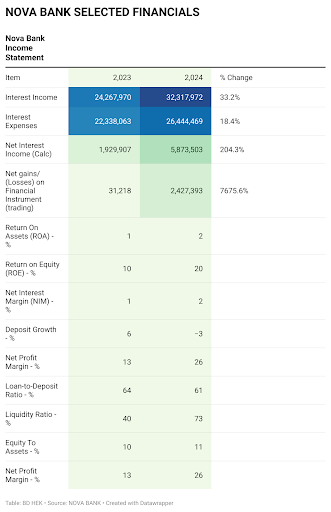

Curiously, Nova did not pursue a merger to shore up its capital base; it chose rather to downgrade from the national status, which it gained in July 2024, to regional status, as its ambition dropped to meet its modest means. But for Nigeria’s bankers’ party where big is good, small is sustainable for Nova. So the “Phygital” empire dream crumbles as the cold water of capital brings it back to a biting reality. With only two branches in Victoria Island and a balance sheet of N373.5 billion that barely touches under 1 per cent of industry assets, Nova fought Goliaths like Zenith and fintech favourites like OPAY. Meanwhile, customer deposits contracted by 3 per cent between 2023 ND 2024 as expensive institutional funding raised costs to 18%. |

|

| The mandate from the regulator was unmistakable – Nova needs N200 billion in capital as a national bank by March 2026, but its shareholders’ equity was a miserable N40.83 billion in 2024, just N10 billion shy of the N50 billion regional bank requirement, but N160 billion miles from national glory.

Whispers of N160 billion capital increase through rights issues, placements, and an IPO had vanished. Earnings are weak and volatile, with almost half coming from non-interest income. Loans are concentrated with top 20 obligors clutching 87.8%, and rating agency GCR’s verdict damns competitive position to “modest”. Was much expected of Nova with its nagging leadership turmoil? Probably not. Since November 2023, Nova has weathered through the times of three CEOs as Nath Ude exits for Adebowale Oyedeji. Now, Chinwe Iloghalu, albeit in acting capacity, superintends over the flight to regional. This CEO churn is scarcely a recipe for confident capital hunt. But lower capital bar may mean survival without fireworks. CBN’s deadline looms and we expect more banks to head the path of downgrade or be forced into uncomfortable marriages. Nova’s choice may yet underscore a reality: in banking, back your ambition with capital bullets or wallow in folly waters. And for Nova, it’s regional relevance is better than national obscurity. FMDQ Group: Hefty Handshake Amid Governance Doubts The options, which entitled Koko to a profit on share price rise above N0.37, already deep in the money given current share price, was a “reward for long-term value creation” according to the FMDQ Board. The reward claim might be true, but it is contextually inappropriate. Koko has midwifed FMDQ’s mutation from just a fixed-income trading platform into a full-fledged market-infrastructure group housing integrating fixed income, currencies, and derivatives. Pre-tax earnings jumped rose 64 per cent in 2024 and revenue climbed 50 per cent to N51.41 billion as the mulls the previously unthinkable move of fighting with the NGX for equity listings. However, total personnel costs soared 63.64 per cent from N11.3 billion in 2023 to ₦17.6 billion in 2024. Average cost per employee stood at a staggering ₦161 million with the bulk going to the top. Minority shareholders are therefore left helpless as they ponder whether the handshake to Koko is a reward for prudent stewardship or a reckless agency cost that points to governance lapse. The N10.4 billion package stunts average executive exit pay in emerging markets and dwarfs Nigeria’s economic realities given a monthly minimum wage of N70,000 ($44) and pervasive poverty that afflicts over 40 of the people. A critical analysis reveals that FMDQ’s financial fortune was driven by factors beyond the market. Almost 67% of total revenues came as fees paid by FMDQ’s main shareholder and regulator, the CBN. CBN’s forex futures are majorly be traded on the FMDQ Group’s platform, giving it a monopoly to generate sturdy futures and margin management fees. Bloom before the rains: Nigerian equities excite with early spring When Halima Okwechime, a recently-inducted stockbroker, walked along the customs street haven of the Nigerian Exchange (NGX), a gush of cheer welled up her slender spine, channelled by the energetic buzz of the trading floor. Recently recruited by a modest stockbroking outfit, her office overlooks the imposing edifice of the trading house where equities in Africa’s most populous economy had trashed global talks of Nigeria’s economic cataclysm to flourish like lilies in the streams. Charts glimmered in the screens of her smooth laptop as they exhibited dazzling rise of local stocks. Dangote Cement and MTN Nigeria were leading a recovery fuelled that rides on the back of a rise in domestic investment and innovative policies. The government’s recent policies had stirred confidence as investors in refused to wait for macro-stabilisation but swooped on stocks they deem to have promising fundamentals. Halima wonders whether the flowering being witnessed is a precursor of healthy seasons ahead or just a greenhouse effect that could wilt under inquest. But the charm of dividend is just one of the storylines NGX’s theatre of trades. Lafarge Africa is a major character in Nigeria’s infrastructure drama, adorning the costume of a powerful growth story jewelled by a year-on-year EPS growth of 100 per cent. Investors then bid up the price to join play. But price moves of stocks like Sovereign Trust Insurance, which rose close to 10 per cent in one day amidst heavy traded volume, bubbled speculation rather than recalibration of fundamentals. So you see a divergence that smacks of a market increasingly rewarding both tangible financial strength and perceived future potential. That is the point! Nigerian stocks behaviours reflect the belief that the better days are already here. Hence, they are delivering gains ahead of time. For investors sufficient risk appetite to trust that Nigeria macro variables will recover, this moment feels less like early spring than a delayed summer and rouses the optimism that future expectations have arrived today. |