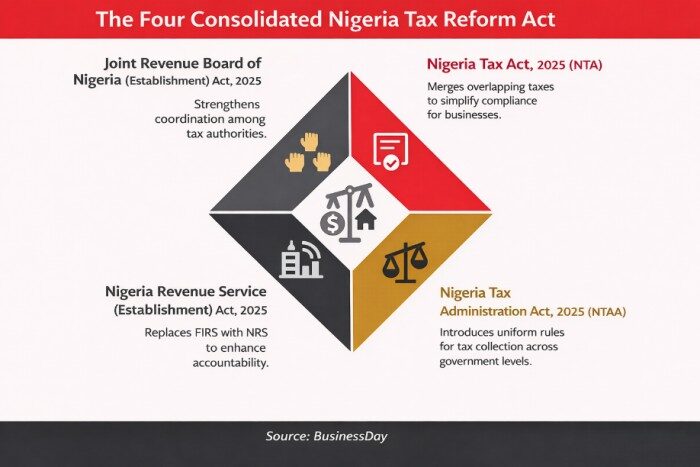

Nigeria’s ambitious tax overhaul: a four-act framework signed into law by President Bola Ahmed including the National Revenue Service (Establishment) Act, the Joint Revenue Board (Establishment) Act, the Nigeria Tax Act, the Nigeria Tax Administration Act, on 26th June, 2025 with the former two becoming effective immediately and the latter two taking effect from January 1, 2026, has quickly become a battleground of perception, legal scrutiny and political contestation.

While the federal government and tax authorities have framed the reform as a necessary modernisation of the nation’s fractured tax architecture, public controversy has centered on alleged discrepancies between the versions of the new tax laws gazette (together with the so-called harmonised version) and those actually passed by the National Assembly leading the public discourse being dominated not by the content of the reforms but by confusion over its authenticity.

Political actors, civil society groups and online commentators amplified concerns, with some calling for the implementation to be suspended and demanding transparent verification of the legislation. In a similar vein, many detractors and naysayers were also peddling misinformation, disinformation, and misconceptions about the content and the potential benefits and costs of the new tax regime.

In response to the mounting concerns, the House of Representatives directed the immediate release of Certified True Copies (CTCs) of the four tax reform acts to provide Nigerians with authoritative documentary evidence, enable independent verification, and dispel misrepresentation.

The early phase of the rollout, therefore, became less about the substance of the reforms and more about confusion over versions, social media claims, and disputed narratives-underscoring how perception can overshadow policy when clarity is absent at the outset.

To this end, this insight aims to cut through the noise, breaking down the impacts on individuals and companies, filing processes, penalties, and why taxes matter.

What the new tax regime actually says

Nigeria’s new tax laws are expected to consolidate more than 70 fragmented taxes into a unified, progressive framework, administered primarily by the reconstituted Nigeria Revenue Service (formerly the FIRS and the other subnational tax collection bodies). The reform aims to simplify compliance, broaden the tax base, reduce evasion, and mobilize revenue for development without placing additional strain on low-income earners.

However, as noted earlier, the rollout has been marred by widespread controversy. Claims on social media that all bank transfers will be taxed or that personal accounts will be seized have fueled public anxiety, with some Nigerians reportedly rushing to withdraw funds from banks, which could precipitate a bank run and erode public trust in the system.

While public debate around Nigeria’s new tax regime has been dominated by confusion over inconsistent documents in circulation, the Certified True Copies (CTCs) released by the National Assembly on Saturday, 3/01/2025, provide the authoritative blueprint of what the laws actually stipulate.

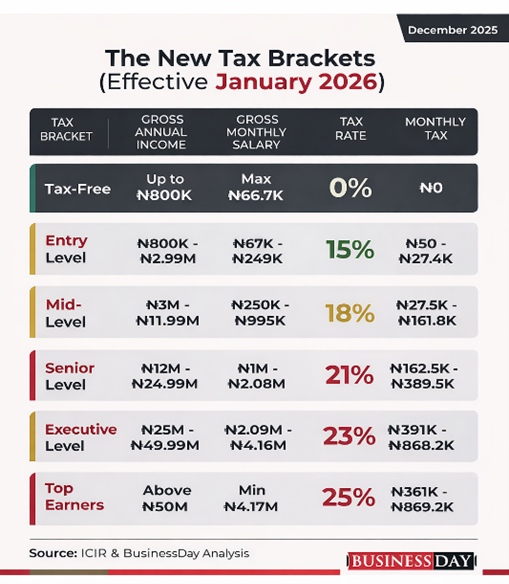

For example, the NTA merges multiple taxes into a streamlined regime. It introduces progressive tax policies, including full exemption for individuals earning ₦800,000 or less annually, with higher income brackets taxed progressively up to a maximum of 25%- a structure confirmed by independent fact checks.

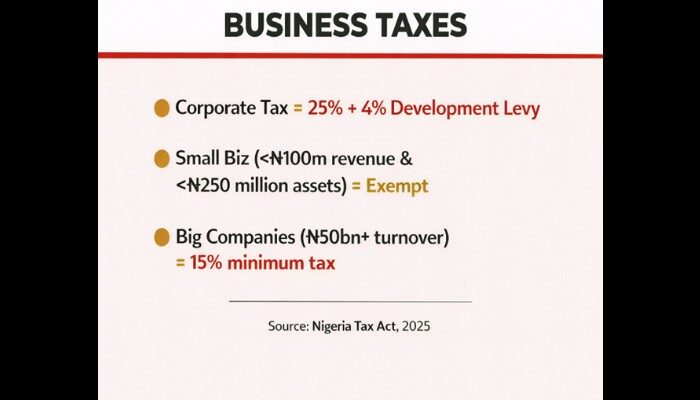

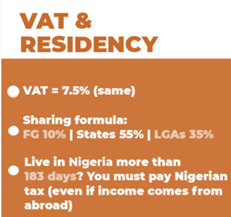

Nigeria’s 2026 tax reforms aim to replace confusion with clarity. Effective January 1, the new framework simplifies personal and business taxation, lowers the corporate tax rate to 25 percent, protects small businesses, retains VAT at 7.5 percent, and clarifies residency rules. Designed to consolidate fragmented levies and broaden the tax base, the reforms promise fairness and efficiency, yet public understanding remains the real test. Can more explicit rules finally rebuild trust in Nigeria’s tax system?

This gap between policy intent and public perception underscores the cost of unclear communication in a low-trust environment.

This clarification effort highlights the battle between perception and reality: whether tax reform is genuinely about modernising revenue administration or has been overshadowed by misinformation that risks undermining public confidence and compliance.

Unfolding controversy

In the unfolding tax law controversy, the National Assembly’s release of CTCs has brought into sharp relief the discrepancy between the versions of Nigeria’s tax reform laws passed by lawmakers and the documents officially gazetted and circulated to the public. The CTCs, covering the four acts, set out in clear terms the provisions actually approved by the legislature and transmitted for presidential assent.

A review of the certified copies alongside the gazetted Acts reveals mild differences. For instance, the version approved by the National Assembly explicitly assigned the Nigeria Revenue Service responsibility for administering key federal taxes, including petroleum income tax and VAT, provisions absent in the gazetted text.

Similarly, financial disclosure reporting thresholds originally set at N50 million for individuals and N250 million for corporate entities in the passed version were replaced in the gazetted Act with lower thresholds, broadening compliance obligations without legislative approval.

The misinformation loop

The controversy surrounding Nigeria’s new tax regime illustrates how misinformation thrives where trust is thin and economic anxiety is high. Unofficial drafts of the tax laws circulated widely online ahead of the release of Certified True Copies, allowing selective readings and speculative interpretations to harden into “facts.”

Social media accelerated the distortion, with excerpts stripped of context and framed as proof of hidden tax hikes or legislative sleight of hand. Political actors and interest groups further amplified these claims, often weaponising the reforms to advance partisan narratives rather than clarify substance.

Tax policy is particularly vulnerable to this cycle. In an economy grappling with accelerating prices, weak purchasing power, and rising living costs, even the perception of higher taxes elicits instinctive resistance.

Public scepticism is reinforced by Nigeria’s history of poorly communicated reforms and uneven policy execution, where official explanations often arrive after narratives have already taken root. In such a low-trust environment, confusion becomes contagious- and once misinformation fills the vacuum, clarity must fight harder to reclaim legitimacy.

Institutional response and credibility test

Faced with mounting public scepticism, Nigeria’s government institutions moved to contain the credibility fallout from the tax reform controversy. The National Assembly’s decision to release CTC of the four tax reform Acts marked a critical intervention, aimed at restoring documentary certainty and countering claims of legislative manipulation. By making certified laws publicly accessible, lawmakers sought to reassert institutional authority and draw a clear distinction between authenticated legislation and unofficial versions circulating online.

However, the response also exposed familiar weaknesses. The release of CTCs came after weeks of speculation, allowing misinformation to entrench itself before official clarification arrived. Tax authorities and the tax committee’s spokespeople largely adopted a reactive posture, explaining provisions only after public anxiety had escalated.

While the corrective steps were necessary and substantive, their delayed timing limited their confidence-building impact. The episode underscores a recurring governance challenge: credibility is not rebuilt by transparency alone, but by timely, proactive communication that anticipates public concern rather than merely responding to it.