For decades, Nigeria’s economy has been defined by a paradox: a nation rich in resources yet crippled by import dependency. Despite vast oil wealth, fertile lands, and a young, entrepreneurial population, the country remains a net importer of everything from refined petroleum to basic food items. This unsustainable model drains foreign reserves, weakens the naira, and leaves the economy vulnerable to global shocks.

But change is possible. With strategic industrial policies, a shift in value chain positioning, and urgent fixes to infrastructure bottlenecks, Nigeria could transform into a net exporter within a decade. The blueprint exists—what’s missing is execution.

Read also:¬ÝAssessing the implications of Nigeria‚Äôs ban on solar panel imports

The import trap: Why Nigeria must break free

Nigeria spends over $49.43 billion annually on imports as of 2023 (Statista), including refined petroleum. Meanwhile, non-oil exports, mostly raw commodities like cocoa and sesame, earn just $5.46 billion (BusinessDay). This imbalance strains foreign exchange reserves and perpetuates a cycle of dependency.

The solution lies in import substitution, a strategy that replaces foreign goods with locally produced alternatives. Countries like India and Brazil have successfully used this approach to build self-sufficient industrial bases. Nigeria must do the same by:

1. Boosting local manufacturing – Instead of importing finished goods, Nigeria should produce them domestically. The Dangote Refinery, set to meet national fuel demand, is a step in the right direction. Similar investments are needed in textiles, steel, and food processing.

2. Value addition in agriculture – Nigeria exports raw cocoa beans but imports chocolate. By processing cash crops locally, the country can capture more value. Ghana, for instance, now exports processed cocoa products worth $1.1 billion annually (Statista). Nigeria, the world’s fourth largest producer, earns just $815.04 million (trendeconomy) from raw beans.

3. Consumption switching – Fiscal policies should incentivise local products. Tariffs on non-essential imports (e.g., luxury cars, refined sugar) could fund subsidies for domestic industries.

4. Prioritising industrial-driven start-ups — Start-ups and SMEs with intents for manufacturing essential goods and offering essential services should be prioritised and aided with financial incentives like zero-interest loans and subsidised raw materials for production.

Moving up the global value chain

Nigeria currently sits at the bottom of global value chains, exporting raw materials and importing finished goods. This model is economically suicidal. To ascend the ladder, the country must:

· Develop industrial clusters – Special economic zones (like Lagos’s Lekki Free Trade Zone) can attract manufacturers with tax breaks and infrastructure.

· Leverage technology – Digital tools can streamline agriculture and manufacturing. For example, blockchain can track cocoa from farm to factory, ensuring fair pricing and quality control.

· Encourage export-oriented SMEs – Small businesses should be supported with grants and export financing to compete globally.

Power and security: The twin pillars of industrialisation

None of these strategies will work without reliable electricity and security.

“With strategic industrial policies, a shift in value chain positioning, and urgent fixes to infrastructure bottlenecks, Nigeria could transform into a net exporter within a decade.”

1. Fixing the power crisis

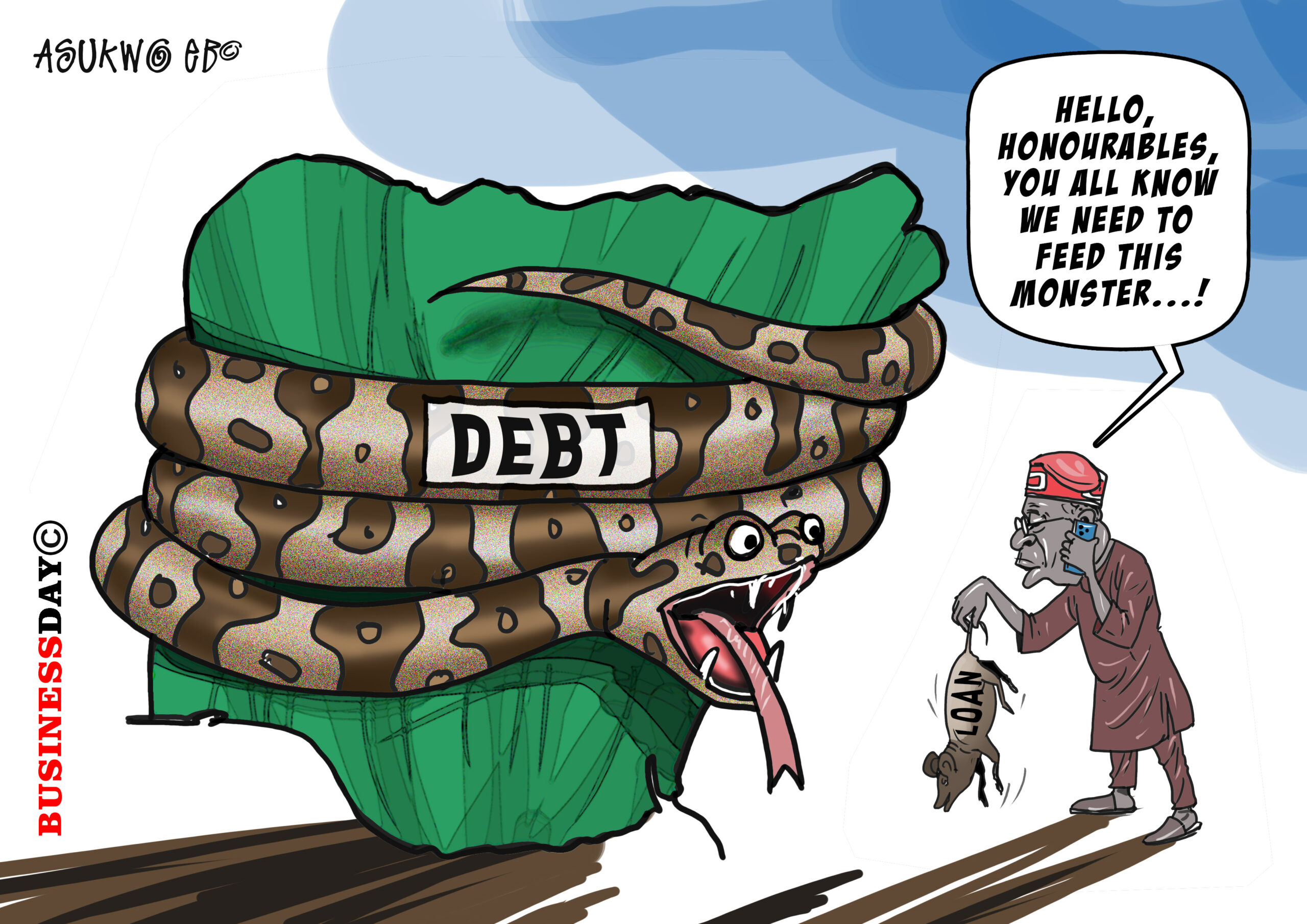

Nigeria generates a meagre 4,000–7,000 MW for 220 million people, less than half of what South Africa (population: 60 million) produces. The national grid is a relic of inefficiency, yet the federal government continues borrowing billions to prop it up.

Read also:¬ÝHow competition, importation can stimulate downstream sector

The way forward:

· Decentralise the grid – States like Lagos, Enugu, and Abia are already exploring independent power projects. The 2023 Electricity Act, which allows states to generate and distribute electricity, must be fully implemented.

· Privatise Transmission – The government still controls transmission, the weakest link in the power chain. Full privatisation could attract investment and expertise.

· Invest in renewables – Solar and hydro projects can bypass grid limitations. Niger State’s 1,000 MW hydropower plant is a promising example.

2. Tackling insecurity

Farmers in Nigeria’s food belt face constant attacks, disrupting agriculture—the backbone of any industrialisation drive. Without security, investors will stay away.

Solutions:

· Community policing – State-backed vigilante groups (like Amotekun in the Southwest) have shown effectiveness.

· Tech-driven surveillance – Drones and AI can monitor bandit-prone areas.

· Economic inclusion – Job creation in high-risk regions can reduce crime.

Political will: The missing ingredient

The biggest obstacle isn’t policy; it’s governance. Corruption, bureaucratic inertia, and short-term political thinking have derailed past reforms.

· Accountability in loans – The power sector has gulped over $10 billion in loans since 1999 with little improvement. Where did the money go? Forensic audits must track past expenditures before new loans are taken.

· State-led reforms – States must take the lead in industrialisation. Lagos’s focus on infrastructure and ease of doing business shows what’s possible.

· Citizen pressure – Nigerians must demand transparency. Social accountability tools, like Kenya’s “Ushahidi” platform, can track government projects and expose mismanagement.

Read also:¬ÝNigeria approves 90% duty waiver on imports under AfCFTA

Conclusion: A blueprint for the future

Nigeria’s journey from importer to exporter won’t be easy, but it’s achievable. The steps are clear:

1. Substitute imports by scaling local production.

2. Move up value chains through processing and industrialisation.

3. Fix power and security to enable business growth.

4. Hold leaders accountable to ensure policies translate into results.

If these measures are implemented with discipline, Nigeria could join the ranks of export-driven economies like Vietnam and Bangladesh within 10–15 years. The alternative continued reliance on imports and debt is a road to ruin. The choice is Nigeria’s to make.

¬Ý

Dr Oluyemi Adeosun is BusinessDay’s Chief Economist.