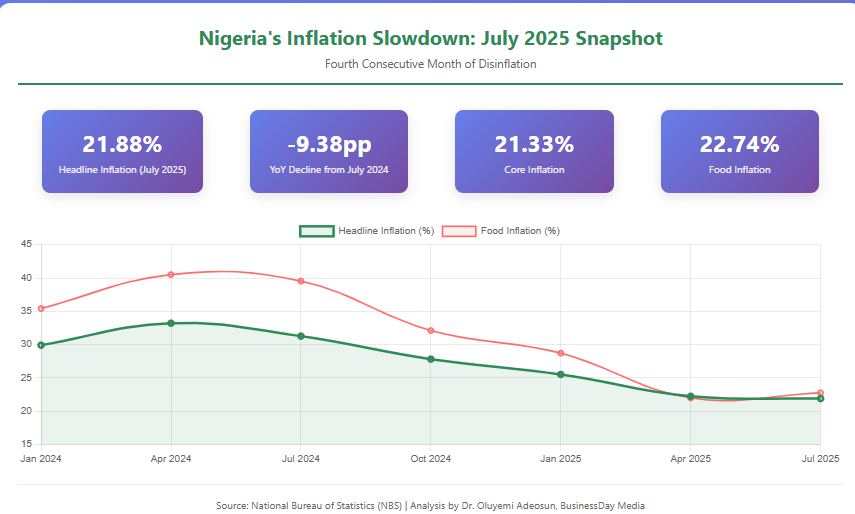

Nigeria’s inflation narrative in 2025 presents a tale of cautious optimism tempered by persistent structural vulnerabilities. The latest data from the National Bureau of Statistics reveals that headline inflation moderated to 21.88% year-on-year in July 2025, marking the fourth consecutive month of disinflation and representing a significant 9.38 percentage point decline from the 31.26% recorded in July 2024. While this trajectory offers welcome relief to an economy long besieged by soaring prices, the underlying dynamics suggest that Nigeria’s journey toward price stability remains fraught with formidable challenges.

The Anatomy of Nigeria’s Disinflation

The current disinflation trend reflects a convergence of favorable base effects, seasonal agricultural improvements, and relative monetary stability. Core inflation, which excludes volatile food and energy components, declined to 21.33% year-on-year, signaling broad-based price moderation across sectors. However, the month-on-month inflation uptick to 1.99% in July from 1.68% in June reveals the fragility of these gains, driven primarily by seasonal travel demand and fuel price adjustments. Food inflation presents a particularly complex narrative. While year-on-year food price growth moderated to 22.74%, the marginal month-on-month improvement masks severe regional disparities. The paradox lies in the seasonal nature of agricultural supply improvements coinciding with persistent structural disruptions in key farming regions. Early harvest supplies provided temporary relief, yet the underlying vulnerabilities in Nigeria’s food security architecture remain unaddressed. The naira’s relative stability against major currencies has been instrumental in reducing imported inflation pressures. This forex stability, combined with lower global commodity prices, has created breathing space for domestic price adjustments. However, this external reprieve should not mask the fundamental weaknesses in Nigeria’s foreign exchange management framework, which continues to rely heavily on administrative measures rather than market-driven mechanisms.

Regional Divergence

Perhaps the most telling aspect of Nigeria’s inflation story lies in its stark regional variations. While national headlines celebrate disinflation, states like Borno continue to grapple with inflation rates exceeding 34%, reflecting the devastating impact of insecurity on local food systems. The insurgency-related disruptions in the Northeast, combined with farmer-herder conflicts across the Middle Belt, have created pockets of hyperinflation that defy national trends. Conversely, states like Yobe experienced inflation declines of over 23 percentage points, highlighting the potential for rapid price moderation when security and supply chain conditions improve. This divergence underscores the critical importance of addressing Nigeria’s security challenges as an economic imperative, not merely a political one. The geographical distribution of inflation pressures reveals deeper structural issues. States with better infrastructure, improved security, and diversified economic bases consistently outperform those dependent on agriculture and afflicted by conflict. This pattern suggests that Nigeria’s inflation challenge cannot be resolved through monetary policy alone but requires comprehensive structural reforms addressing security, infrastructure, and institutional capacity.

Market Response and Sectoral Dynamics

Nigeria’s equity markets have responded positively to the disinflation trend, with the Nigerian Exchange recording significant gains across multiple sectors in July. The Industrial Goods Index surged 34.27%, reflecting improved investor sentiment and lower input costs. Banking stocks gained 25.82% as easing inflation reduced pressure on interest rates and loan performance expectations. Consumer goods companies benefited from a 11.14% gain, supported by improved household purchasing power in regions experiencing price moderation. This market optimism, while encouraging, must be viewed within the context of Nigeria’s broader economic fundamentals. The correlation between inflation moderation and equity performance suggests that investor confidence remains highly sensitive to macroeconomic stability. However, the sustainability of these gains depends critically on whether policymakers can address the underlying drivers of price instability. The Oil and Gas sector’s modest 1.72% gain underscores Nigeria’s continued dependence on external commodity dynamics. Despite being a major oil producer, Nigeria remains vulnerable to global price volatility due to its limited refining capacity and heavy dependence on refined product imports. This structural weakness continues to transmit external shocks directly into domestic inflation, highlighting the urgent need for downstream petroleum sector reforms.

Global Context and External Vulnerabilities

Nigeria’s inflation trajectory cannot be divorced from global economic dynamics. The moderation in international commodity prices, particularly food and energy, has provided temporary relief to import-dependent economies like Nigeria. However, this external environment remains precarious, with geopolitical tensions in key shipping routes and ongoing conflicts threatening to reignite global inflation pressures. The Federal Reserve’s monetary policy stance continues to influence capital flows to emerging markets, including Nigeria. While current conditions have supported naira stability, any shift toward aggressive monetary tightening in advanced economies could trigger capital flight and currency pressures, potentially reversing recent inflation gains.

Structural Challenges: The Persistence of Vulnerability

Despite recent improvements, Nigeria’s inflation dynamics remain fundamentally shaped by structural vulnerabilities that monetary policy alone cannot address. The country’s agricultural sector continues to operate below potential due to insecurity, inadequate infrastructure, and limited access to modern inputs. Climate change impacts, evidenced by increasing flood frequency and intensity, threaten to exacerbate food supply disruptions. The logistics and transportation network remains a critical bottleneck, with poor road infrastructure and limited rail capacity driving up distribution costs across the economy. Power sector inefficiencies continue to impose significant costs on manufacturers, contributing to persistent core inflation pressures despite favorable external conditions.

Perhaps most critically, Nigeria’s fiscal framework lacks the institutional capacity to support sustainable price stability. The continued reliance on crude oil revenues exposes public finances to external volatility, while limited non-oil revenue generation constrains the government’s ability to invest in productivity-enhancing infrastructure.

Policy Imperatives: Beyond Monetary Accommodation

Consolidating Nigeria’s disinflation gains requires a comprehensive policy response addressing both immediate vulnerabilities and long-term structural constraints. Security sector reforms must prioritize the protection of agricultural communities and critical infrastructure, recognizing that economic stability and national security are inextricably linked. Investment in climate-resilient agriculture, including irrigation systems, improved seed varieties, and post-harvest storage facilities, represents a critical component of long-term food security. The Central Bank’s continued focus on monetary policy rate management, as emphasized by Governor Olayemi Cardoso, provides necessary anchoring for inflation expectations, but must be complemented by coordinated fiscal and structural reforms. Foreign exchange market development requires moving beyond administrative allocation toward a more transparent, market-driven system with appropriate safeguards. This transition, while potentially disruptive in the short term, is essential for building sustainable external stability.

Conclusion: Cautious Optimism, Vigilant Implementation

Nigeria’s current inflation trajectory offers genuine cause for optimism, representing the most significant disinflation progress in recent years. However, the path from statistical improvement to sustainable price stability remains challenging and uncertain. The convergence of favorable base effects, seasonal agricultural improvements, and external commodity price moderation has created a window of opportunity that policymakers must seize decisively. The regional disparities in inflation performance serve as a sobering reminder that national averages can mask severe local challenges. Until Nigeria addresses its fundamental security, infrastructure, and institutional weaknesses, the economy will remain vulnerable to recurring inflation pressures regardless of monetary policy stance. For businesses, investors, and households, the current environment offers cautious optimism but demands continued vigilance. The sustainability of recent gains will ultimately depend on the government’s capacity to implement comprehensive structural reforms while maintaining macroeconomic stability. Only through such coordinated efforts can Nigeria transition from temporary statistical relief to enduring economic transformation.