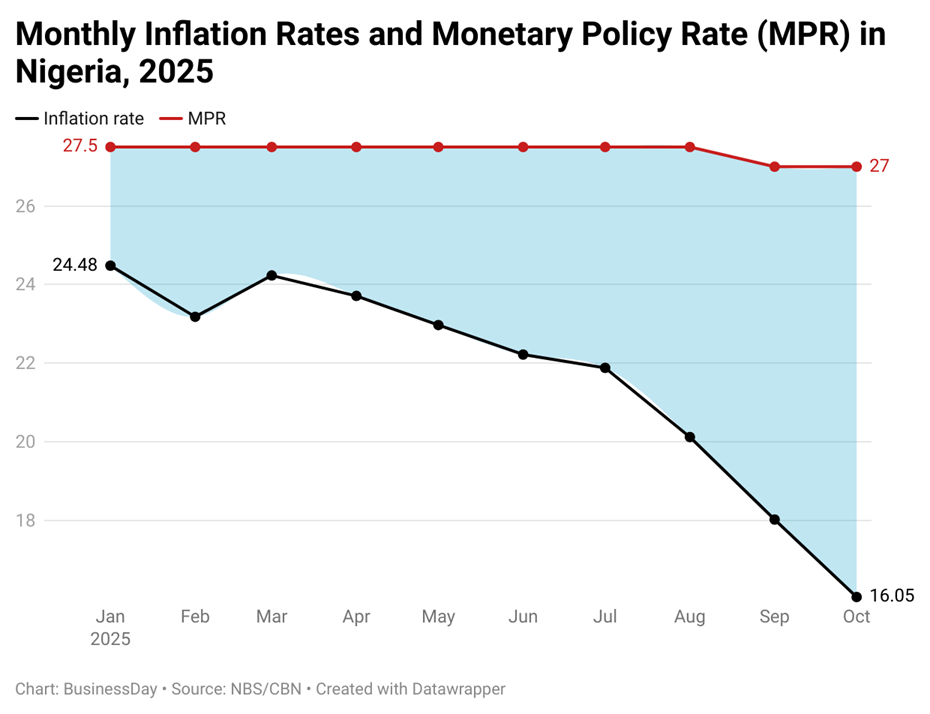

Nigeria’s inflation story is showing signs of a turning point. The National Bureau of Statistics (NBS) reports that headline inflation eased further to 16.05 percent in October 2025, down from 18.02 percent in September, moving closer to the Central Bank of Nigeria’s medium-term target of 15 percent.

In response to this sustained moderation, the bank’s Monetary Policy Committee meeting on 23 September led to a cut in the Monetary Policy Rate by 50 basis points, from 27.50 percent to 27.00 percent, the first-rate reduction since the reform cycle began.

Cooling inflation alongside this policy easing is reshaping market sentiment and signaling a potential shift away from an era of aggressively tight monetary policy.

A shift investors have been waiting for

The fall from 18.02 percent to 16.05 percent may appear modest but it is significant in the Nigerian context. It marks the seventh consecutive month of disinflation and came in below many analysts’ expectations.

Slower inflation is giving households and businesses some relief after two years of persistent cost pressures.

The central bank’s rate cut was initially met with caution because one reduction does not confirm a trend. Combined with sustained moderation in inflation, however, the cut is increasingly being interpreted as the first signal of a broader shift in policy.

Razia Khan, Chief Economist for Africa and the Middle East at Standard Chartered, notes that, “The central bank’s stance suggests the possibility of more easing ahead.”

The sentiment is spreading across the market and investors now see a credible case that the tightening cycle is approaching its limit. With inflation continuing to ease, expectations are growing that the next MPC meeting could bring another round of easing.

For most of the past two years, investors assumed that high inflation and expensive credit would remain entrenched. That assumption is now being tested as the link between falling inflation and policy adjustments becomes clearer and as confidence gradually returns.

Bonds gain early momentum

Fixed income markets tend to respond first when inflation softens. As inflation moderates, real yields improve and existing government bonds become more attractive.

In Nigeria, longer maturities, particularly those between 20 and 30 years, have become key targets for institutional investors positioning for a potential easing cycle.

State bonds with stronger fiscal management and high-quality corporate issuers are also attracting attention. Lagos State’s N200 billion bond issue was oversubscribed by 55 percent, according to BusinessDay, while its N14.8 billion Green Bond drew nearly double the offer size. The response signals renewed confidence in the state’s fiscal strength and infrastructure plans.

Paul Alaje, Chief Economist at SPM Professionals, argues that the combination of moderating inflation and greater currency stability is creating the conditions for a rotation into longer dated local debt.

In periods of high inflation, fixed income assets struggle because rising yields rarely keep pace with price growth. With inflation now softening, the asset class is regaining its relevance after a challenging period.

Equities receive a quiet boost

The equity market tends to react more gradually, but the effects are meaningful. Lower inflation and a softer MPR reduce borrowing costs for banks, manufacturers and consumer goods firms. Banks stand to benefit from improved credit demand and greater stability in net interest margins.

Nigerian banks still operate with one of the lowest loan-to-deposit ratios among large emerging markets such as Brazil, India and South Africa. A more predictable macroeconomic environment improves their medium-term earnings outlook.

Manufacturers and consumer goods companies are also noting early signs that the shock from the 2023 and 2024 reforms, including subsidy removal, naira adjustment and higher import costs, is beginning to fade. If inflation continues its downward trend, input cost pressures will ease and valuations could re rate across several sectors.

This creates an opening for patient investors to re-enter undervalued segments of the market, especially high dividend blue chips that had been avoided during the inflation and credit squeeze.

Short term instruments enter a new phase

Treasury bills and money market placements offered safety during the tightening cycle. They will remain important for liquidity management but yields on these instruments are likely to compress as inflation eases.

Investors with large cash positions may need to begin planning a move into longer term bonds and corporate credits once the yield curve starts to readjust.

A calmer inflation path supports mild FX stability

Nigeria’s structural foreign exchange challenges remain, including import dependence, fragile reserves and periodic volatility.

However, moderating inflation reduces import-driven price shocks and contributes to a more predictable currency path. This benefits importers, exporters and participants in the FX market.

Foreign investors typically require a predictable inflation trajectory before returning to Nigerian Eurobonds or selective equity exposure.

Oyekan Idris, a capital markets analyst, notes that the key question is whether lower policy rates can reach the real economy and stimulate credit growth without reigniting inflation. His view captures the delicate balancing act facing policymakers.

Eurobonds offer an opening for dollar investors

If the disinflation trend persists, Nigeria’s Eurobond spreads are likely to tighten, which would boost prices of existing notes. For global investors searching for yields above major benchmarks, Nigeria presents an appealing mix of carry and potential capital gains.

Markets often price in turning points before they become consensus, which makes early positioning critical for those who believe inflation has peaked.

What investors should focus on now

Nigeria’s inflation remains elevated by global standards but its trajectory has shifted. This matters for pricing, valuations and expectations around monetary policy.

Investors who move early can lock in attractive fixed income yields before further rate cuts, accumulate high quality equities while valuations remain compressed and still maintain short term placements for liquidity while preparing for reallocation.

In a market where momentum can shift rapidly, this may be the period when positioning begins to pay.