Economic orthodoxy insists that stable, low inflation is the bedrock of long-term growth. For Nigeria, however, the historical record tells a more complicated story.

In 2010, when the country posted an impressive 8 percent GDP expansion, the kind of headline number that policymakers still dream about, inflation was running at nearly 14 percent. The mid-2000s, often celebrated as Nigeria’s “boom years,” also saw double-digit inflation for much of the time.

Between 2004 and 2008, growth averaged about 7 percent annually, even though consumer prices climbed by 12 percent–18 percent in most years. Only in 2006 and 2007 did inflation dip briefly below 10 percent.

At first glance, the numbers appear to challenge conventional wisdom. If high inflation is supposed to stifle growth, why did Nigeria’s economy perform so strongly in the very years when price pressures were elevated? Does this mean that single-digit inflation is unnecessary for hitting 8 percent–10 percent GDP growth?

The answer lies in understanding the drivers of Nigeria’s performance. The mid-2000s boom was powered less by domestic policy finesse and more by an extraordinary external environment.

Oil prices surged above $100 a barrel, global liquidity was abundant, and debt relief under the Paris Club gave Nigeria fiscal breathing space. These one-off factors turbo-charged growth even as inflation eroded household purchasing power. In other words, the economy was lifted by a tide that concealed underlying weaknesses.

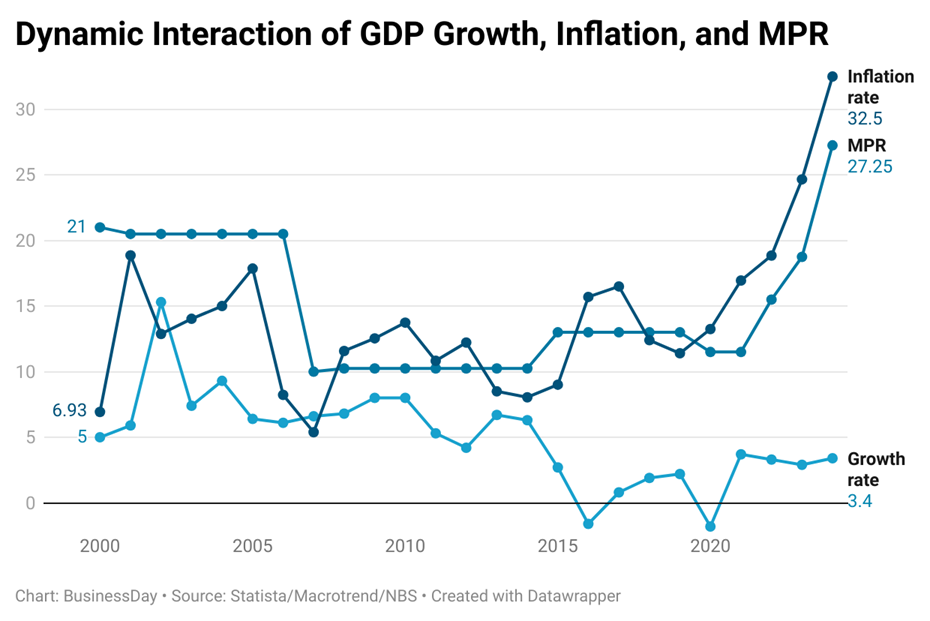

A closer look at the data shows why sustained growth under double-digit inflation has proven elusive. After 2010, Nigeria never again managed to combine high growth with double-digit inflation. By 2016, when inflation reached 15.7 percent, GDP actually contracted by 1.6 percent, the country’s first recession in two decades.

Again in 2020, as inflation climbed above 13 percent, the economy shrank by 1.8 percent. The most recent figures are more sobering: in 2023, growth slowed to 2.9 percent while inflation surged to nearly 25 percent. In 2024, inflation breached 32 percent a level not seen in decades while growth hovered at a modest 3.4 percent.

According to Ibrahim Musa, a researcher at the Federal University Dutsin-Ma, recent econometric evidence shows that “a percentage unit change in inflation has resulted in a 31 percent and 21.9 percent decrease in economic growth in the long run and short run respectively” in Nigeria, underscoring how destructive high prices can be for output.

Similarly, a Central Bank of Nigeria (CBN) paper using a threshold-inflation model estimated that once inflation rises above 13 percent, the impact on growth becomes increasingly damaging.

Yet some experts caution against overzealous monetary tightening. Paul Alaje, chief economist at SPM Professionals, recently argued that pursuing a sharp disinflation path could “stunt nascent growth trajectories” in an economy already battling infrastructure gaps and currency instability.

“The ambition to force inflation down to 15 percent in 2025 may carry a growth trade-off that Nigeria cannot afford,” he noted.

The implication is clear: while double-digit inflation did not prevent short bursts of rapid expansion in the past, it undermined sustainability. Inflation erodes real incomes, deters investment, and compounds inequality.

It also forces the central bank into a perpetual tightening cycle. In 2000, Nigeria’s benchmark Monetary Policy Rate (MPR) stood at 21 percent. Two decades later, in 2024, it has been ratcheted up to 27.25 percent in an effort to tame inflation. Such high rates squeeze credit to businesses, making it harder for the non-oil economy to thrive.

Comparisons with peer economies underscore the risk. Indonesia, which in 1960 had a lower GDP per capita than Nigeria, achieved long stretches of 6 percent–7 percent growth while keeping inflation in single digits for much of the 2000s and 2010s.

Vietnam, another resource-light economy, managed a similar feat. Their experience suggests that low inflation is not just desirable but a prerequisite for broad-based and inclusive growth.

Nigeria’s case, therefore, is best seen not as evidence that inflation doesn’t matter, but as proof that external booms can temporarily mask its costs. High oil prices once provided a cushion, allowing growth to coexist with inflation.

But in today’s more diversified global energy landscape, with oil demand peaking and climate policy shifting capital flows, that cushion no longer exists. The economy can no longer rely on windfalls to offset domestic fragility.

So, can Nigeria achieve 8 percent–10 percent growth again with inflation above 12 percent?

The data suggests it is unlikely. Without structural reforms, double-digit inflation will continue to choke competitiveness and erode productivity. The country may still see short-lived spikes of growth if oil prices rise sharply, but the broader economy will remain vulnerable.

The lesson is that Nigeria’s future growth model cannot be built on the shaky foundation of double-digit inflation. Price stability is not just an economist’s obsession; it is the precondition for investment, job creation, and poverty reduction.

If Nigeria wants to match the performance of its peers, it must prove that it can deliver sustained growth alongside single-digit inflation, a combination it has yet to master.