Nigeria’s equity market closed 2025 with a performance that few would have confidently predicted two years earlier. The NGX delivered a year-to-date return of just over 50 percent, its strongest showing in five years and among the best-performing markets on the continent. This rally was not simply a rebound from a low base; it reflected a deeper shift in how investors now view Nigerian equities. Faced with persistently negative real returns in fixed income, investors rotated decisively toward equities as a hedge against inflation and currency risk.

Market capitalisation expanded sharply, creating real wealth effects and restoring relevance to the stock market as a savings and investment vehicle. Domestic institutional investors led the charge, while foreign portfolio investors—still cautious—began to re-engage as policy clarity improved. What made 2025 stand out was not just the size of the gains, but the quality of the re-rating: companies with resilient earnings, stronger balance sheets, and credible exposure to Nigeria’s adjustment story were consistently rewarded.

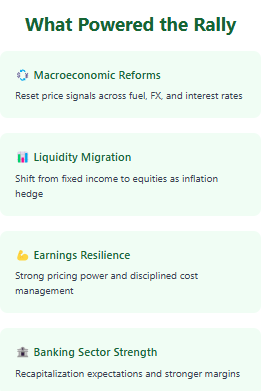

What powered the rally

Several forces came together to reshape market outcomes in 2025. Macroeconomic reforms reset long-distorted price signals across fuel, foreign exchange, and interest rates, forcing investors to reprice risk more honestly. As fixed-income yields struggled to keep pace with inflation, liquidity migrated steadily into equities, driven by pension funds, asset managers, and increasingly confident retail investors. Corporate earnings proved more robust than expected, supported by pricing power, foreign exchange repricing, and disciplined cost management. This earnings resilience provided the fundamental justification for higher valuations.

The banking sector, in particular, benefited from expectations around recapitalisation and stronger margins, reinforcing confidence in systemic stability. Importantly, the rally was not narrow. Gains cut across banking, industrial goods, consumer stocks, insurance, and energy, signalling a market that was reassessing Nigeria’s corporate landscape through a medium-term lens rather than chasing short-term defensive trades. That breadth reduced fragility and marked a clear break from past rallies driven by only a handful of names.

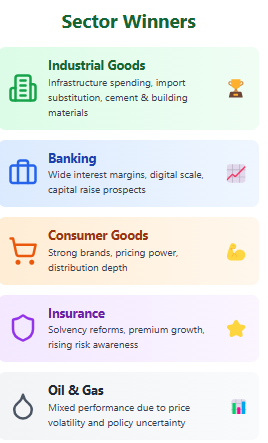

Sector winners and shifting narratives

Sectoral performance in 2025 revealed where investors saw both protection and opportunity. Industrial goods led the market with outsized gains, buoyed by infrastructure spending, import substitution policies, and strong demand from construction and energy-related value chains. Cement, glass, and building materials benefited from improved foreign exchange availability and local sourcing advantages. Banking stocks followed closely, supported by wide interest margins, digital scale, and the prospect of capital raises that could unlock future credit growth.

Consumer goods surprised on the upside despite pressure on household incomes, as strong brands used pricing power, distribution depth, and operational efficiency to defend margins. Insurance stocks quietly staged one of the most meaningful re-ratings, lifted by solvency reforms, premium growth, and rising risk awareness from a low base. Oil and gas performance was more mixed, reflecting crude price volatility and policy uncertainty, but firms with clearer governance and cash-flow visibility continued to attract interest.

Gainers, losers, and a more discerning market

A closer look at the market’s biggest winners and laggards highlights how much the NGX has matured. The strongest performers were not defined by size alone, but by narrative change. Companies emerging from long periods of neglect, balance-sheet repair, or strategic repositioning saw dramatic re-ratings once credibility returned. Names like NCR and Guinness reflected investor appetite for technology exposure and consumer franchises capable of navigating inflationary conditions.

On the other end of the spectrum, the weakest performers were often those caught on the wrong side of policy change, operational setbacks, or fading confidence after earlier rallies. This dispersion sends an important signal. The Nigerian market is no longer one where broad sector exposure guarantees returns. Stock selection now matters. Governance quality, earnings durability, and strategic clarity increasingly determine outcomes. Volatility remains, but it is becoming more selective rather than indiscriminate, rewarding preparation over speculation.

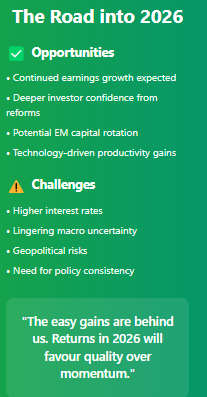

The road into 2026

Looking ahead, the outlook for Nigerian equities remains constructive, though more demanding than in 2025. Corporate earnings growth is expected to continue supporting valuations, while ongoing structural reforms should deepen investor confidence and attract incremental domestic and foreign flows. Global conditions may also help, particularly if capital continues to rotate toward emerging markets and technology-driven productivity gains reshape investment theme

s. That said, the easy gains are likely behind us. Higher interest rates, lingering macro uncertainty, and geopolitical risks mean returns in 2026 will favour companies embedded in resilient value chains, with strong cash flows and adaptable management teams. For policymakers, sustaining momentum will depend on policy consistency, regulatory credibility, and continued reform discipline. For investors, the message is clear: the next phase of returns will come not from chasing momentum, but from owning quality. Nigeria’s equity market has rediscovered its relevance; the challenge now is to prove it can sustain it.