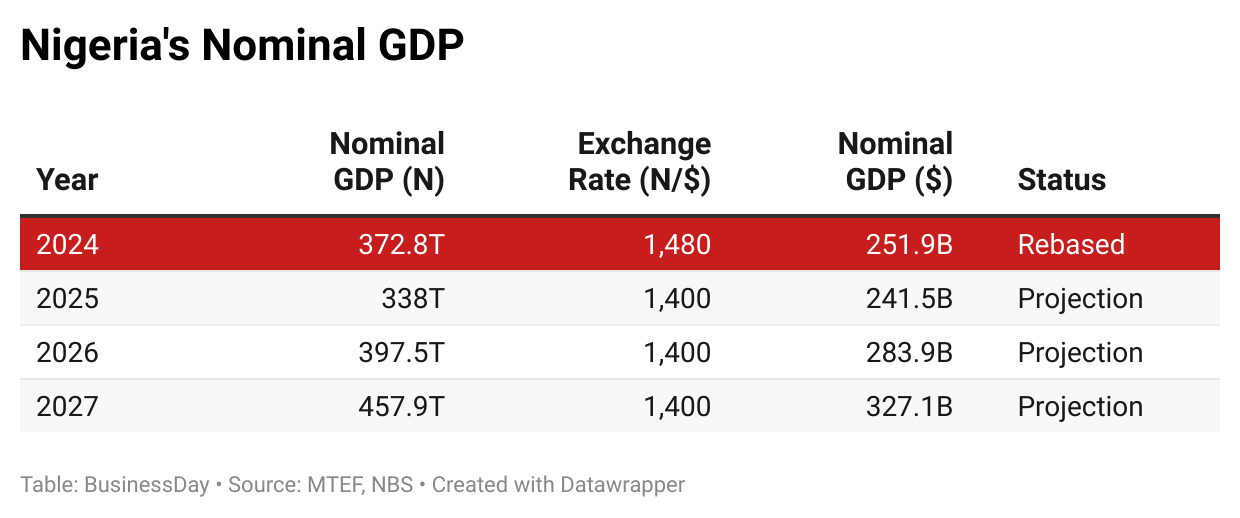

The National Bureau of Statistics (NBS) has rebased its GDP, which now stands at N372.8 trillion. In dollar terms, this is just a mere $252ŌĆ»billion, twice lower than the 2014 rebased numbers.

This is where it gets interesting. Locally, the nation is growing, but globally, it is lagging. The nominal GDP in 2014 was N89.8ŌĆ»trillion, compared to N372.8ŌĆ»trillion in 2024, a staggering 315.14 percent increase over the period. In dollar terms, the Nigerian GDP fell from $510 billion post-2014 rebasing to $252 billion post-2024 rebasing.

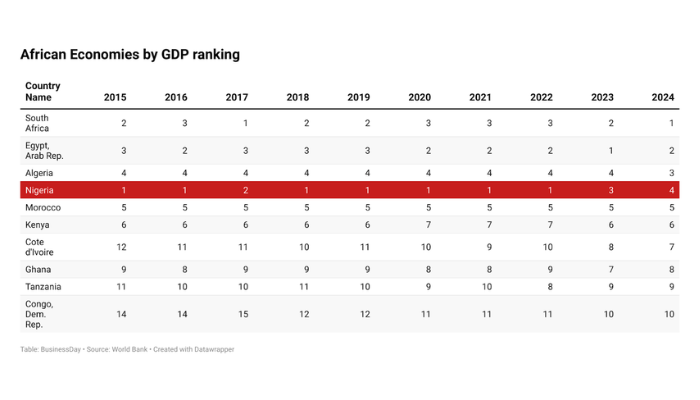

Another profound thing to note is that the Nigerian economy became the fourth largest in Africa for the first time in 2024, according to the World Bank data. In 2014, the nation emerged as AfricaŌĆÖs largest economy after rebasing.

Since 1960, NigeriaŌĆÖs economy has only ranked the third largest 14 times. This is happening as a result of sporadic naira devaluation.

Read also:┬ĀNigerian economy to grow by 3.7% in H1 on higher oil production

According to Kelvin Emmanuel, an economist and co-founder of Dairy Hills, ŌĆ£What ┬Ż1 could buy you in 1975 is what you need ┬Ż10.72 to buy in 2025. Ask yourself the same question for the naira. What could N1 buy you in 1975, and how much of the same naira do you need to purchase the same quality and quantity of item in 2025? The clearest test of GDP rebasing is its measure against purchasing power parity.ŌĆØ

The question Emmanuel asked is pivotal. The GDP has expanded in naira terms, but the purchasing power hasnŌĆÖt increased in the same manner.

Bismarck Rewane, CEO of Financial Derivatives Company, added another perspective on Channels TV, noting that while rebasing gives a clearer picture of the economy and now shows Nigeria at about $252ŌĆ»billion, it also underscores how far behind the country is in key fundamentals.

ŌĆ£The presidentŌĆÖs aspiration is to make this economy a $1 trillion economy by 2030. If you are to do that from $250ŌĆ»billion in five years, the economy has to grow at 15 percent, but youŌĆÖre growing at 3 percent. ThereŌĆÖs a difference between leaping and limping,ŌĆØ Rewane said.

He further highlighted that NigeriaŌĆÖs power generation per head is only 180 kilowatts, compared to 3,000 kilowatts per head in South Africa, a critical factor limiting growth.

This, once again, puts the question of a $1 trillion economy into another set of interrogation. The current administration plans to achieve this ŌĆśbold visionŌĆÖ by 2030, which is just five years away.

According to Femi Gbajabiamila, chief of staff to the President, speaking during the Fifth Steering Committee meeting at the State House, Abuja on July 22, 2025, ŌĆ£The recent Tax Reform Acts, signed into law in June, underscored the urgency of accelerating reforms and pursuing NigeriaŌĆÖs $1 trillion economy target.ŌĆØ

This shows that the government believes in its ambition, even when experts say it is farŌĆæfetched.

Read also:┬ĀNigerian economy resilient amid global trade tensions, Middle East war ŌĆō Report

Analysis done by BusinessDay in 2024 showed that Nigeria would need to grow by 38 percent annually to achieve the $1 trillion economy target, while the Financial Derivatives Company (FDC) put its estimate at 40 percent.

The World Bank, in its May 2025 Nigeria Development Update (NDU), said Nigeria must grow fivefold to achieve this.

Given the current growth projections in the Medium Term Expenditure Framework (MTEF) for 2025ŌĆō2027, NigeriaŌĆÖs economy is expected to hit $327.1ŌĆ»billion by 2027. However, it is important to note that these estimates were prepared before the recent GDP rebasing, meaning the MTEF figures may need to be updated to reflect the revised baseline.

$315bn in 2030

In contrast, BusinessDayŌĆÖs analysis, applying the current average growth rate of 3.8 percent and an exchange rate of N1,521.07/$, projects that NigeriaŌĆÖs economy could reach only $315ŌĆ»billion by 2030.

This represents a 68.5 percent shortfall from the governmentŌĆÖs $1ŌĆ»trillion target. While the country appears to be falling behind, with decisive reforms and structural changes, it still has the potential to catch up with its peers.