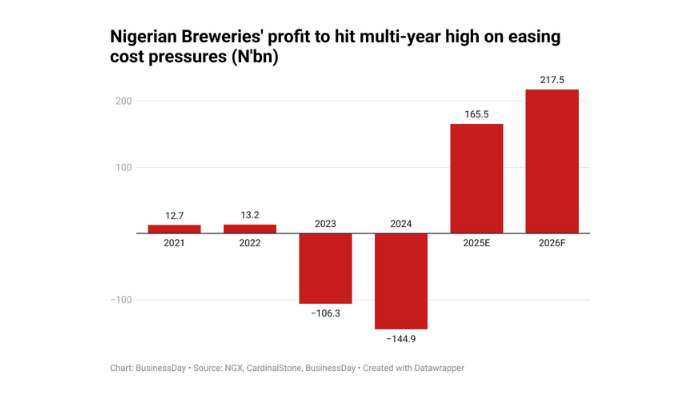

Nigeria’s biggest beer maker, Nigerian Breweries, is on course to record its highest profit in more than a decade as lowering cost pressures and stable naira overturn two consecutive year losses incurred by the consumer goods giant.

The Lagos-headquartered brewer is expected to declare a N165.5 billion profit-after-tax in full year 2025, a material recovery from the N144.9 billion loss reported last year and N106.3 billion posted in 2023.

Analysts at CardinalStone Research, a Lagos-based consultancy, see the company’s recovery set in the last quarter of 2024 and “accelerated” in the first quarter of this year to boost profit to a “multi-year high” and increase revenue.

“This strong recovery, which appears to have set in Q4’24 and accelerated in Q1’25, looks set to ride stronger-than-expected volume recovery amid favourable prices and tamer cost pressures,” the analysts said.

Read also: Shareholders laud Nigerian Breweries profitability amidst economic challenges

“We have a FY’25 revenue projection of N1.5 trillion, which is supported by strong volume growth projections and moderate price increases.”

Nigerian Breweries returned to profitability in Q1, bringing respite to the biggest beer maker in Africa’s most populous nation after two years of FX-induced losses dealt a blow to the company’s earnings.

The Brewer declared a net profit of N44.6 billion in its 2025 unaudited first quarter results, a 186 percent rise from the N52.1 billion loss recorded in the same period last year.

The recent stability of the naira against the US dollar saw a sharp drop in FX-induced losses as it fell to N178 million in the first three months to March compared to N72.9 billion in the corresponding period last year.

The company’s diversification drive beyond beer and expansion into other alcoholic beverage categories like wines, ciders, and spirits, which appeal to a more diverse consumer base is expected to support its earnings growth.

Nigerian Breweries completed the purchase of the remaining 20.0 percent stake in Distell Nigeria, thereby securing full ownership of the company. “We expect this acquisition to deliver accretive benefits to the company’s overall performance,” CardinalStone Research analysts said.

Read also:¬ÝClimate fund managers invest $36m in Nigerian Breweries‚Äô clean energy shift

Slowing inflation, FX stability to ease cost pressures

The company is betting on the declining inflationary trend and new-found stability in the exchange rate market to ease its cost pressures, which quickened to its highest in over a decade at 70.5 percent.

But the firm’s cost-to-sales ratio is expected to moderate to 61.0 percent in 2025.

“Our prognosis is supported by easing inflationary trends, a more stable foreign exchange environment, and the company’s ongoing cost-saving initiatives.”

The beer maker has embarked on some cost-saving measures, which include a strategic shift toward greater use of sorghum as a primary raw material and the increased localisation of packaging materials such as bottles and cans.

These measures, according to the analysts, are expected to underpin an improvement in gross margin to 39.0 percent compared to 29.5 percent in full year 2024.

Early recovery signs are emerging as the cost-to-sales ratio declined to 56.6 percent in Q1’25 when compared to 63.9 percent in Q1’24.

Read also:¬ÝHow distributors drove Nigerian Breweries‚Äô 2024 record revenue

Deleveraging strategy seen reducing FX losses

Nigerian Breweries raised N548.7 billion in its completed rights issue in December 2024 to repay foreign intercompany loans and trade payables, which had been major contributors to foreign exchange losses.

This deleveraging strategy might just have been panning out as the company recorded an FX gain of N2.9 billion in Q4’24, in contrast to an FX loss of N66.5 billion in the same quarter in 2023.

In the first three months of this year, foreign exchange loss was only N178.0 million compared to N72.8 billion in Q1’24, as the company continued to benefit from its strategic deleveraging.

“Looking ahead, we do not anticipate any new foreign borrowings, in line with management’s decision not to raise external debt,” the analyst wrote in a note.

“Rather, the company is now focused on minimising foreign currency exposures. These factors, combined with expectations of relative Naira stability, inform our expectation for minimal FX losses for FY’25.”