For Nigeria, it’s better late than never.

Just when it seemed like the lower interest rate in the U.S. would elude Nigeria’s Eurobonds, the yields on the dollar bonds are at their lowest level in seven months and sources say talks of a $2 billion sale are back on the table.

The sources who did not want to be named because the plan was not yet public said the government could raise as much as $2 billion but did not give a timeline.

“The market conditions are as favourable as they can get and it’s normal to weigh the options,” one of the sources said.

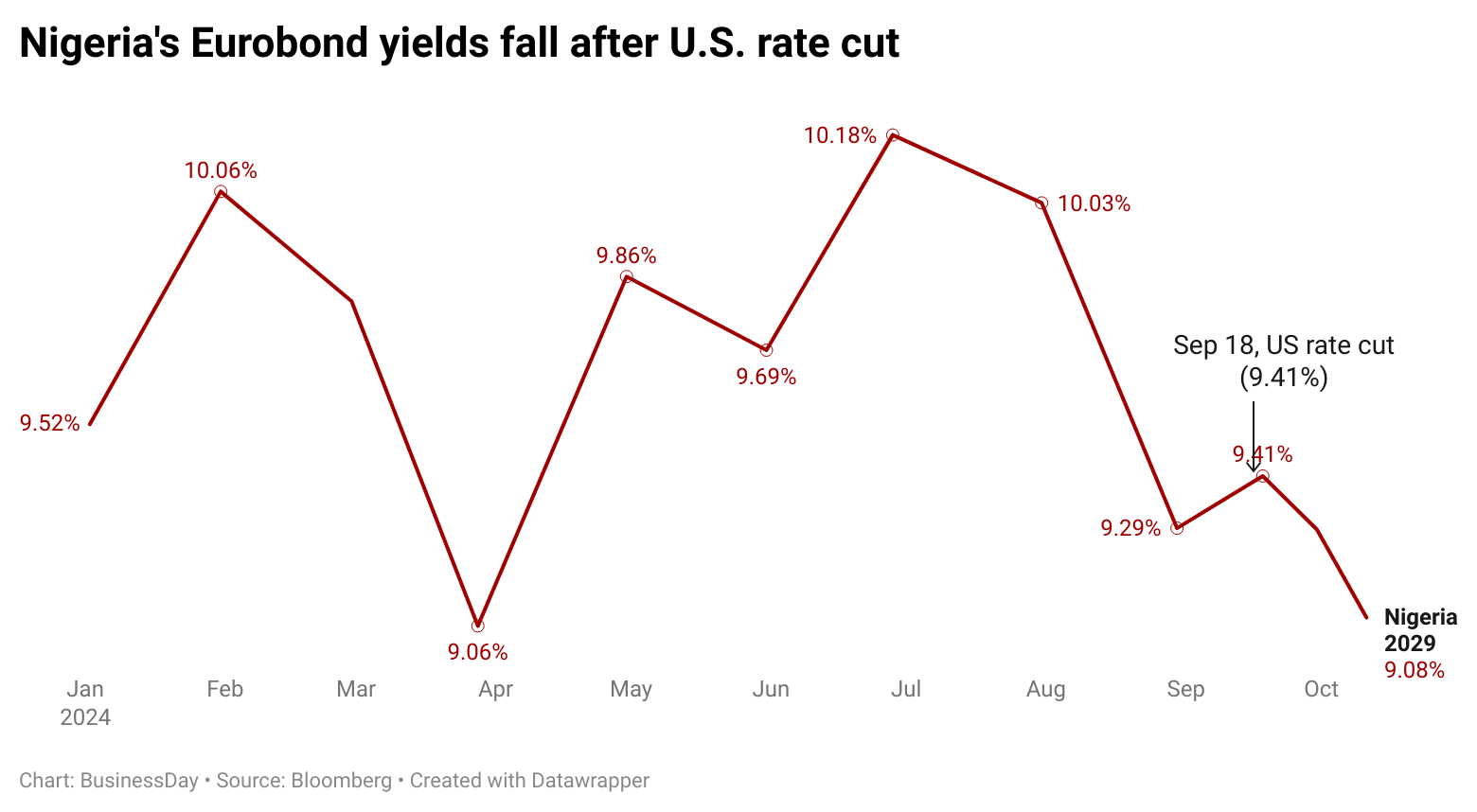

According to data compiled by BusinessDay, the average yield on Nigerian Eurobonds fell to 9.08 percent on October 11, the lowest since April. Falling yields are a sign of increasing investor appetite for a bond.

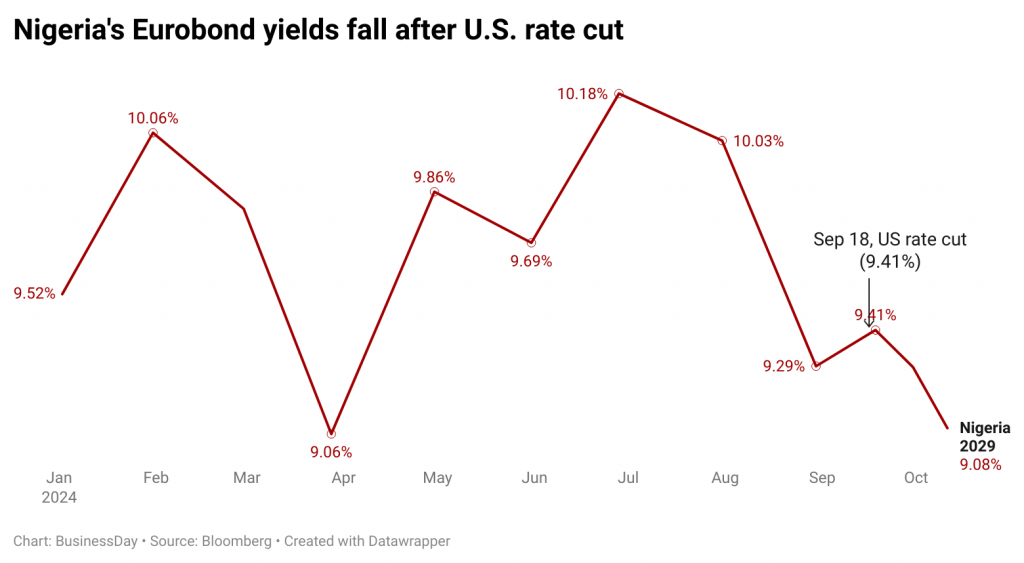

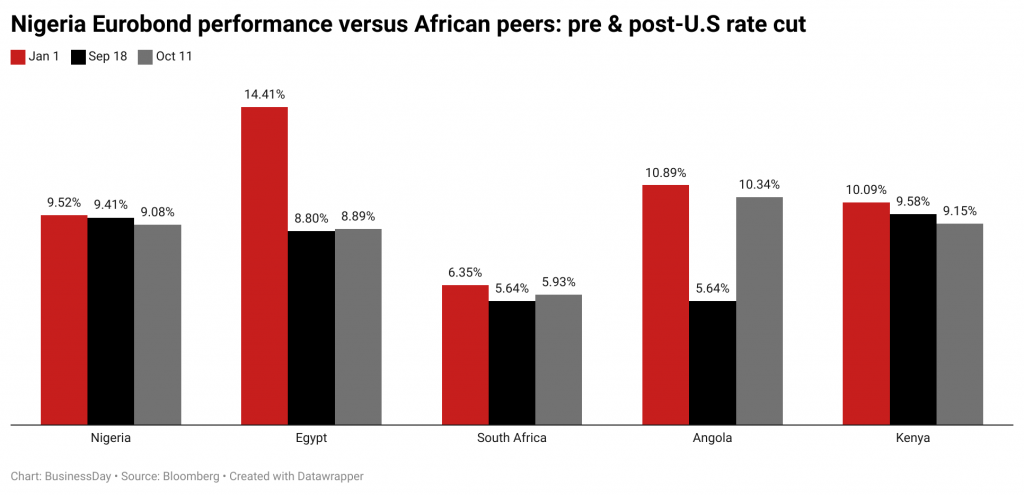

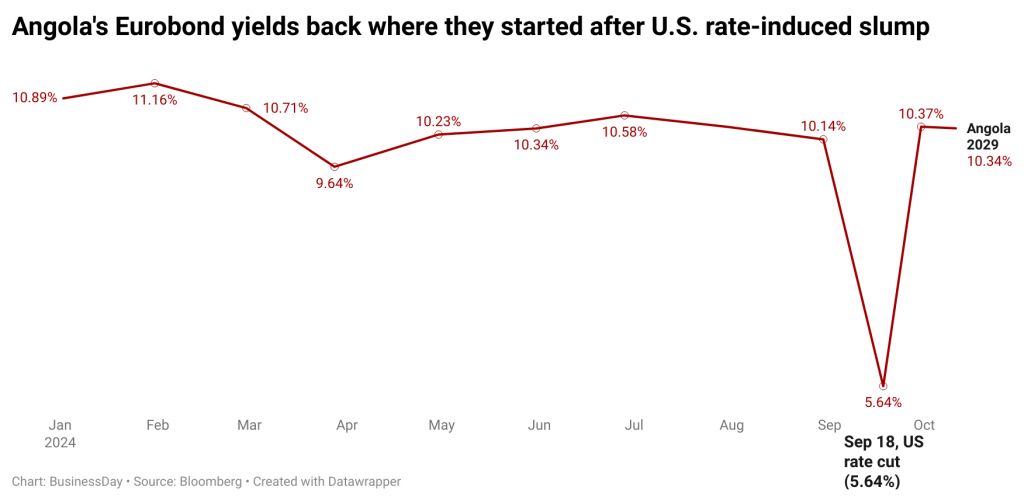

Since the interest rate cut by the United States Federal Reserve on September 18, yields on Nigerian Eurobonds have dipped 343 basis points, compared to a rise in the yields of Egyptian (+101 percent), South African (+517 percent) and Angolan bonds (+83.38 percent).

The movement in the yields since the beginning of the year however suggests that Nigeria was late to the party with investors already pricing in a possible rate cut in the U.S. in their investment in the other African markets.

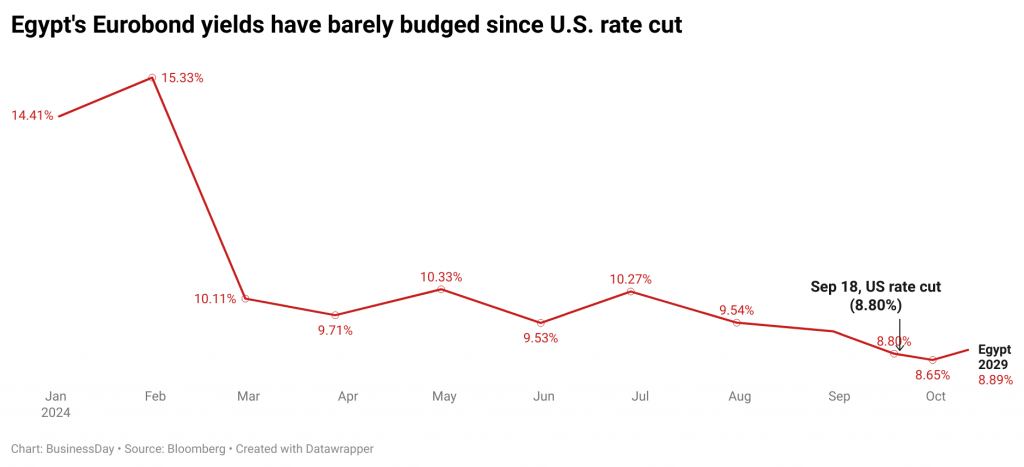

The yield on Egypt’s Eurobonds has dropped by the most since the start of 2024, tumbling by 3830 basis points.

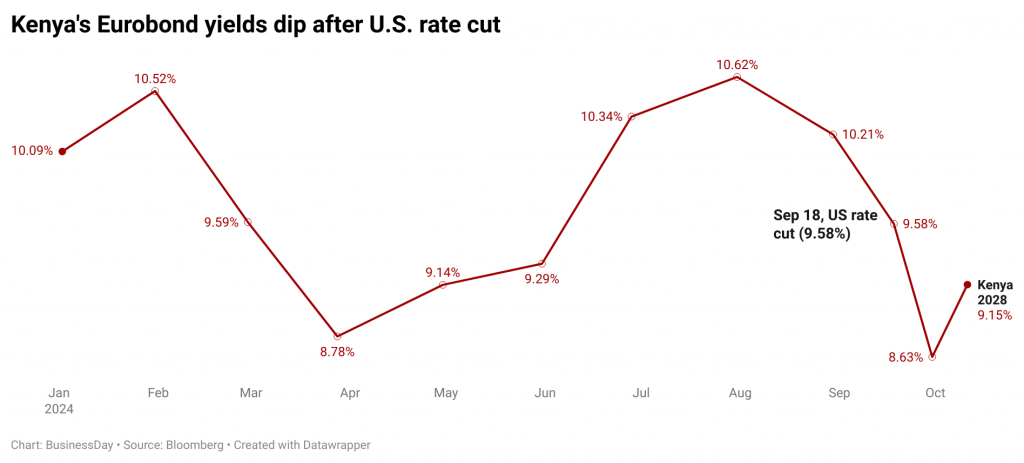

Kenya’s Eurobond yield has also dropped by 936 basis points in that time while yields on South African and Angolan Eurobonds have cooled by 657 basis points and 502 basis points respectively.

Nigeria’s Eurobond yield in comparison has declined the least with 463 basis points.

Favourable market conditions

Nigeria had seemed poised to return to the Eurobond market after a two-year break earlier this year but the plan has slowed.

Officials of the DMO, who watch the international capital markets closely, said that the government would only tap the Eurobond market when market conditions were favourable. Market conditions are deemed favourable when a country can borrow at relatively low interest rates.

With the yields on the Eurobonds falling to their lowest in seven months, Nigeria has the favourable conditions it has craved for thanks to the interest rate cut in the United States.

According to a recent report by the Financial Derivatives Company Limited led by Bismarck Rewane, the US Fed’s rate cut will pave the way for new debt issuances by African nations, including Nigeria and Angola.

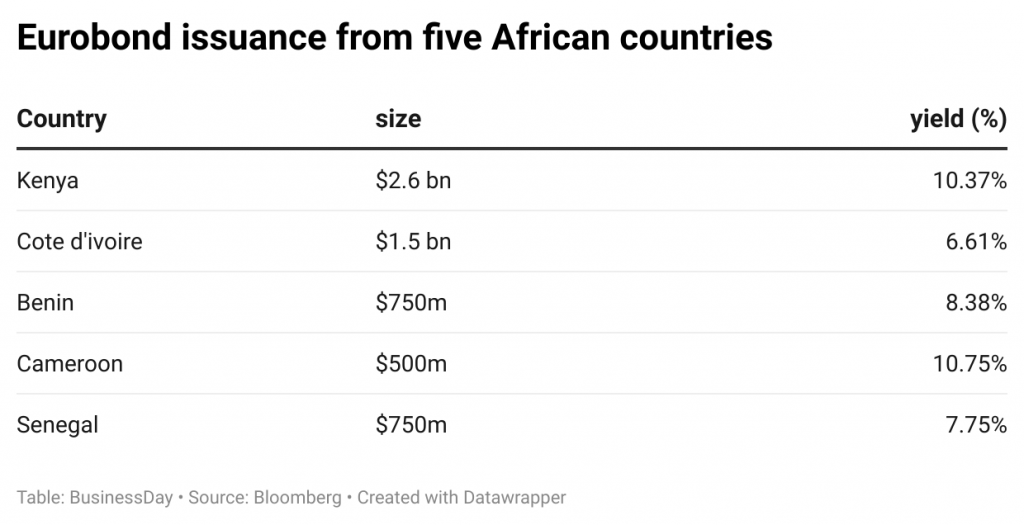

Côte d’Ivoire became the first African nation to re-enter the market post Covid-19, issuing $2.6bn Eurobonds in January 2024 at a yield of 6.61 percent, similarly Kenya successfully issued a new $1.5 billion Eurobond (10.37%) in February 2024.

Benin was the third African country to issue a Eurobond this year, its first-ever. The $750 million issuance was five times oversubscribed and cost 8.375 percent.

Senegal also issued a $750 million dollar bond in June at a rate of 7.75 percent.

Cameroon tapped the market in July, issuing a seven-year $550 million Eurobond at a yield of 10.75 percent.

Naira could do with some dollars

The biggest winner from a fresh Eurobond sale will be the naira, according to analysts who said the embattled currency is gasping for breath in the face of short dollar supply.

The naira has plunged by more than 70 percent since Nigeria removed capital controls mid last year.

“There is a strong possibility that Nigeria will tap into the Eurobond market next year,” an economist who did not want to be named said.

“It is expected that the government will raise at least USD 2.00 billion from the Eurobond market next year,” he said.

He said this expectation is based on the likelihood of a widening fiscal deficit, as projected expenditure growth is set to outpace revenue gains.

“Additionally, the anticipated easing of global monetary and financing conditions would encourage the government to enter the market, attracting substantial interest from foreign investors.”

New path to dollar loans

The success of Nigeria’s maiden domestic dollar bond could however provide a much assured path to raising dollar debt, according to some economists.

In August, the federal government issued its first series of the domestic dollar bond, a $2 billion programme to be raised in four batches of $500 million each, with a coupon of 9.75 percent.

The issuance was oversubscribed by 180 percent to the tune of $900 million.