For the first time in over five years, Nigeria is offering positive real return, as the interest rate is now higher than inflation. On paper, this should be good news—after all, it means money in the bank might finally grow rather than shrink.

But for millions of Nigerians struggling with rising costs, the reality is more complex.

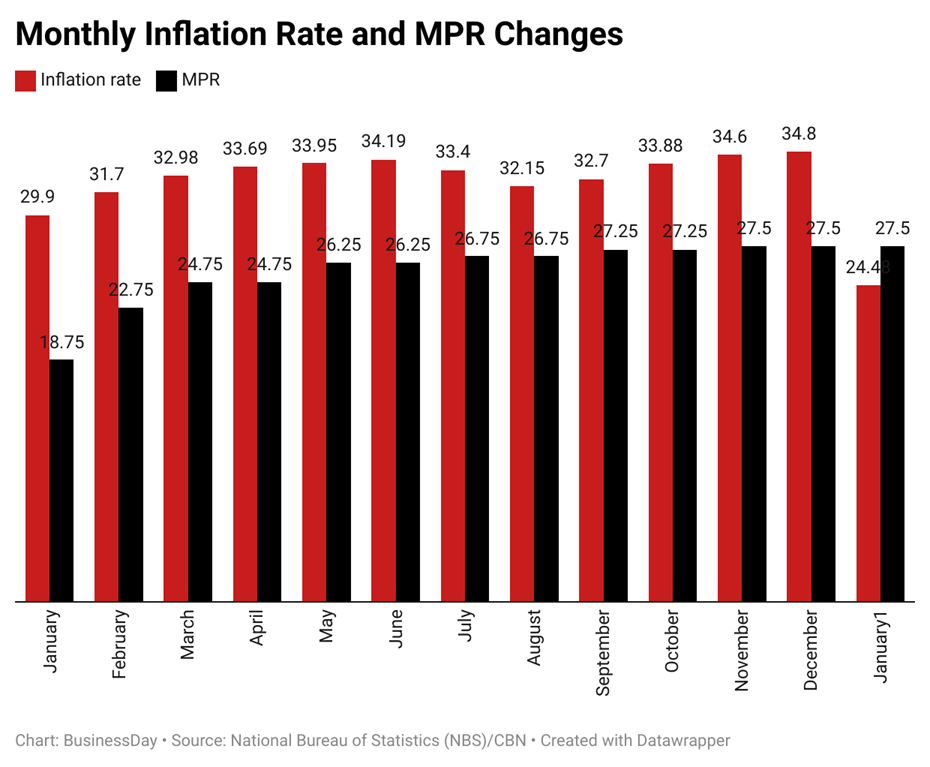

This shift follows the National Bureau of Statistics’ (NBS) recent rebasing of the Consumer Price Index (CPI), which caused inflation to drop sharply from 34.8 percent in December 2024 to 24.48 percent in January 2025.

At the same time, the Central Bank of Nigeria (CBN) has kept its benchmark interest rate at 27.5 percent, making borrowing more expensive while encouraging savings. But will this help or hurt ordinary Nigerians?

What Changed?

The rebasing of the CPI means inflation is now measured against a more updated set of goods and services that reflect current spending habits.

While this provides a more accurate picture, it does not mean prices have fallen—only that inflation is being calculated differently, Basit Shuaib, a financial advisor, explained.

Food, fuel, and transport costs are still high, and for many Nigerians, daily expenses remain a struggle.

Meanwhile, with the MPR staying at 27.5 percent, borrowing has become more expensive. Loans for school fees, medical bills, or business expansion now come with higher interest rates, making access to credit even harder.

What This Means for Households

For the average Nigerian, the biggest impact is on savings and loans. Higher interest rates mean keeping money in a bank could finally yield real returns—something unheard of in previous years when inflation ate into savings faster than banks could grow them.

This could encourage more Nigerians to save, strengthening financial institutions in the process.

However, borrowing is now costlier. Families who need loans for essentials like school fees or emergencies may struggle to afford credit.

Even with inflation appearing lower, food prices remain high, meaning many will not feel any immediate relief. In reality, people’s wallets will still bear the weight of expensive living costs.

What This Means for Businesses

For businesses, particularly small and medium enterprises (SMEs), this shift presents both opportunities and challenges.

On the one hand, higher interest rates could attract foreign investors looking for better returns, helping to stabilize Nigeria’s currency and economy.

On the other hand, expensive credit is bad news for SMEs that rely on loans to manage cash flow, stock goods, or expand.

Fewer businesses may be able to afford loans, leading to slower growth, reduced hiring, and potentially higher unemployment.

Additionally, if households cut spending due to financial pressure, businesses that rely on consumer purchases could see a decline in demand.

The Bigger Picture—Saving and Spending

While a higher MPR could encourage Nigerians to save more, excessive saving at the expense of spending can hurt the economy.

When people stop spending, businesses suffer, leading to fewer jobs and slower growth. Nigeria already faces weak consumer demand, and a further drop in spending could worsen economic struggles.

What’s Next?

For now, the CBN’s decision to keep interest rates high suggests a wait-and-see approach, as policymakers monitor inflation and economic activity. If inflation remains stable, future rate cuts could become an option to stimulate growth.

As Olayemi Cardoso, the CBN Governor put it, the bank remains focused on “maintaining price stability and fostering a more transparent foreign exchange market.”

But for ordinary Nigerians, the key question remains: Will this shift make life easier, or will the cost of living continue to outpace income growth?

For now, Nigerians must navigate a financial system where saving may finally pay off, but borrowing comes at a steep price—and despite official figures, everyday survival remains a struggle.