…As lending hits record N1.87trn

Nigeria’s microfinance banks (MFBs), originally designed to support the country’s micro, small, and medium enterprises (MSMEs), are shifting their lending priorities towards safer and more lucrative deposit-taking institutions, where they earn higher returns.

The shift to depository corporations has raised concerns about the ability of MSMEs to survive in an increasingly tough economic climate.

A depository corporation is a financial institution that accepts deposits from customers and holds these deposits in various forms such as savings accounts, checking accounts or fixed deposits.

Depository corporations include commercial banks, savings banks, credit unions and other types of financial institutions that provide deposit services.

Read also:¬ÝLagos launches N10bn fund for MSMEs

Data from the Central Bank of Nigeria (CBN) show that loans issued by MFBs to depository or financial corporations soared by 71.3 percent, rising from N221.26 billion in September 2023 to N379.10 billion in September 2024.

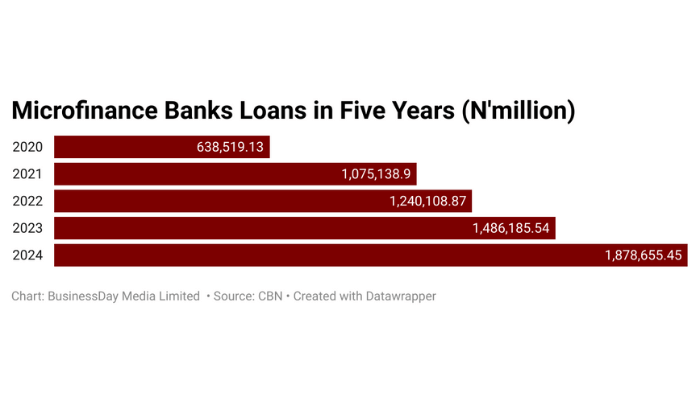

The growth in inter-institutional lending took place as the total loan book of MFBs expanded by 26.4 percent, reaching a record N1.87 trillion as of September 2024, up from N1.48 trillion in the same period of the previous year.

The CBN’s data also show that total assets of microfinance banks grew marginally by 0.7 percent over the same period, increasing from N3.02 trillion to N3.05 trillion. Despite this modest asset growth, MFBs’ investment in securities other than shares witnessed an explosive rise of 160.97 percent, from N35.16 billion in September 2023 to N91.77 billion in September 2024.

Why MFBs are shifting priorities

Speaking anonymously to BusinessDay, one operator acknowledged the shift, saying, “Microfinance banks are increasing their loan disbursement but are doing it in ways that reduce their exposure to risks. Rather than focusing on MSMEs, many now prefer tritiewo lend to other financial institutions or invest in government securities. It’s about protecting their balance sheets.”

The shift in lending behaviour has left MSMEs, who traditionally rely on microfinance banks for credit, with fewer avenues to access essential financing. The operator added, “Before now, MFBs had been heavily focused on micro-lending. But since the currency devaluation, which has had a ripple effect on the entire economy, most of us have started focusing more on retail and electronic banking. If you visit malls, you’ll notice that most PoS machines belong to microfinance banks now.”

MSMEs struggle

While MFBs pursue more secure and less volatile financial strategies, the MSME sector in Nigeria continues to shrink under pressure. The 2020 National MSME Survey conducted by the National Bureau of Statistics (NBS) in collaboration with the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN) reported approximately 39.7 million MSMEs in Nigeria, with micro enterprises accounting for 96.9 percent of the total.

Read also:¬ÝA Journey Through the Streets: What MSMEs Taught Us About Going Digital

However, more recent estimates show a sharp decline. The Nigerian Economic Summit Group (NESG) revealed that between 2023 and 2024, about 30 percent of the country’s registered MSMEs closed down.

This trend, if sustained, could spell deeper economic woes, especially given that MSMEs contribute around 46.3 percent to Nigeria’s GDP and provide over 80 percent of jobs.

Also, the currency and deposit base of microfinance banks contracted significantly, dropping by 33.68 percent to N339.29 billion in September 2024 from N511.64 billion a year earlier. The decline in deposits could further limit the sector’s ability to support lending, particularly to higher-risk segments like MSMEs, experts say.

CBN data also showed that MFBs’ net claims on the federal government jumped by a staggering 172.15 percent, rising from N32.67 billion in September 2023 to N88.92 billion in the same month of 2024. These claims are primarily investments in government-issued securities.

Explaining the significance of this trend, Ayokunle Olubunmi, head of financial institution ratings at Agusto & Co., said: “Claims on the central government are essentially funds that the government owes the microfinance banks, often through treasury bills and bonds. These are considered safe investments with predictable returns.”

He added that the CBN mandates microfinance banks to invest a portion of their deposit liabilities in treasury bills to maintain liquidity and stabilise the sector. “Microfinance banks are required to invest at least five percent and no more than 10 percent of their deposit liabilities in treasury bills. This rule is part of the central bank’s liquidity management framework for the sector,” Olubunmi said.

Despite a broader shift away from MSMEs, MFBs’ loans to non-financial corporations also grew significantly, reaching N1.49 trillion in September 2024, a rise of 18.54 percent from N1.26 trillion recorded in the same period of 2023.

Commenting on the rising demand for credit, Kazeem Olanrewaju, Group CEO of Alert Group, said that the economic climate has made additional funding a necessity for businesses. “The demand for credit is influenced by multiple factors, including the devaluation of the naira, high inflation, government fiscal policies, and monetary policies from the CBN. Entrepreneurs now need more funds just to maintain their inventory levels. What used to cost N1 million might now cost N1.8 million,” he said.

Read also:¬ÝOdua, NPO to deepen job creation, MSMEs growth in South West

MFBs’ contribution

Despite the challenges, some within the industry remain optimistic about the sector’s contributions. Adeola Ayibiowu, managing director/CEO of Lovonus Microfinance Bank, stated that microfinance banks continue to serve millions of Nigerians through a range of services. “The microfinance sector has experienced significant growth in terms of operators, technology integration, and scope of services. With over 900 licensed MFBs as of 2024, the industry plays a crucial role in driving grassroots economic empowerment,” Ayibiowu said.

Efforts to gather further reactions from leading figures in the sector were unsuccessful. Taiwo Joda, managing director of Accion Microfinance Bank, declined to comment, citing his busy schedule. Similarly, Rogers Nwoke, former president of the National Association of Microfinance Banks (NAMB), was unavailable for comment, and Cynthia Ikponmwosa, managing director/CEO of LAPO Microfinance Bank, said she was in a meeting.