In Lagos, real estate isnŌĆÖt just business; itŌĆÖs a battleground of ambition and access. From the glistening towers of Ikoyi to the sprawling estates of Ibeju-Lekki, property is the cityŌĆÖs most visible symbol of power and wealth creation. Yet, behind the billion-naira transactions and luxury high-rises lies a deep market divide: one where developers chase the affluent while millions still dream of affordable shelter.

LagosŌĆÖ real estate story is full of contrasts: increasing investment inflows, expanding cityscapes, and a persistent housing shortage that highlights urban inequality. As infrastructure develops and global capital returns, the key question is whether Lagos can build not just for profit, but for the people. Who is really purchasing these homes?

Read also:┬ĀExperts urge innovation, ethical standards to drive excellence in NigeriaŌĆÖs real estate sector┬Ā

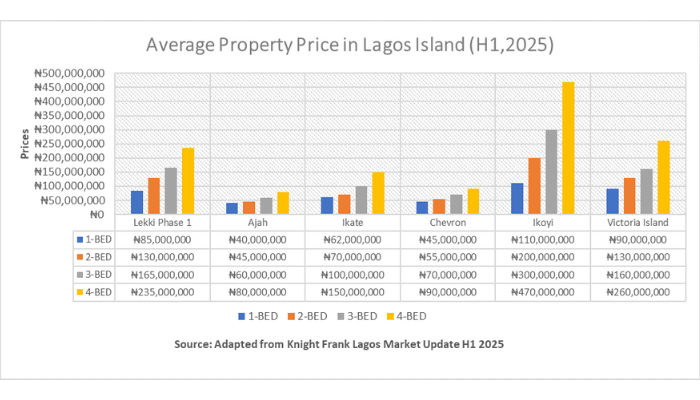

Housing cost in Lagos Island

Over the last five years, apartment and duplex prices in Ikoyi, Lekki, and Victoria Island have increased well beyond what most middle-class professionals can afford. According to data from Knight Frank Lagos Market Update, a luxury two-bedroom flat in Lagos Island now sells for approximately N105million, while median salaries remain far below the level required for such purchases, widening the affordability issues

The affordability gap continues to widen, pushing many professionals toward more budget-friendly areas such as Ajah and Chevron, where two-bedroom flats average N70 million and N90 million, respectively.

This trend underscores the growing exclusivity of Lagos IslandŌĆÖs luxury real estate market, where high-end apartments are increasingly reserved for upper-income earners and investors. Without targeted housing reforms or income growth, homeownership in these areas will be tough.

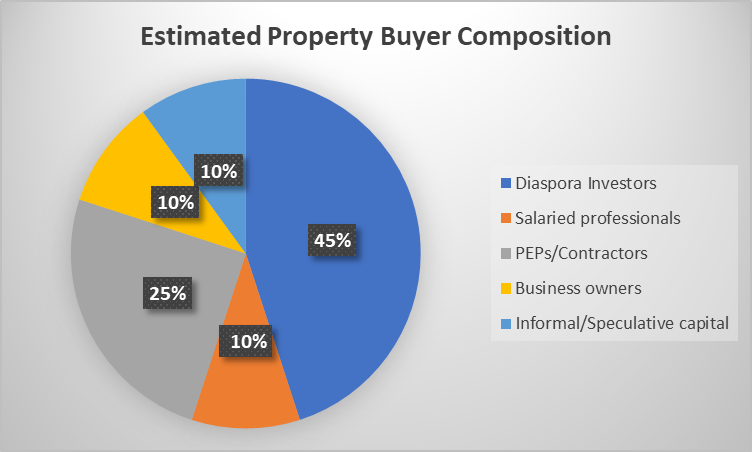

BuyersŌĆÖ breakdown

If middle-income professionals are struggling to stay in the game, the question then is: who is really driving property demand in Lagos? The cityŌĆÖs buyer landscape remains complex and largely unclear.

According to Estate Intel, only about 10 percent of buyers in prime Lagos neighbourhoods are salaried local professionals and a few business owners. The majority fall into three groups: diaspora investors, politically connected individuals or government contractors, and those investing through speculative or unclear capital sources often tied to ŌĆśinformal wealth.ŌĆÖ

Some realtors report that a significant number of luxury apartments and houses are sold before completion to buyers who never actually move in. These units are often treated as investment vehicles or safe havens for capital rather than homes.

Read also:┬ĀFoundation plans masterclass on Tax in Real Estate for professionals

This trend aligns with findings from Digital Landlord, which notes that diaspora remittances are increasingly driving property investments. Some estimates suggest that as much as 30 percent of funds sent home by Nigerians abroad end up in real estate.

Meanwhile, local mortgage rates remain prohibitively high, frequently above 18 percent, shutting out many domestic buyers and favouring those who can pay cash upfront.

These patterns paint a clear picture of a market sustained less by end-users and more by speculative and external capital, reinforcing the illusion of broad-based homeownership in Lagos.

The regulation gap

NigeriaŌĆÖs property market shows clear signs of imbalance, but regulators have been slow to respond. Enforcement remains weak, and policy development has not kept pace with market activity. In Lagos, real estate prices often operate without proper oversight. Developers frequently quote prices in dollars or their naira equivalent, linking property costs to foreign exchange (FX) rates instead of local income realities. This has created a market where property values no longer accurately reflect domestic affordability.

Land registration and documentation are still poorly coordinated, making it difficult to identify accurate property owners. The lack of transparency and limited disclosure requirements allow many large transactions to go untracked. This oversight gap enables questionable capital inflows to circulate freely within the sector.

The absence of effective price regulation and the weakness of consumer protection frameworks further deepen inequality. Regulators, developers, and policymakers now face growing pressure to restore fairness, transparency, and confidence in NigeriaŌĆÖs most dynamic property market.

The Central Bank of Nigeria data shows that remittances hit $600 million in 2025 ŌĆō the highest figure in years. A notable portion of this capital flows into real estate, pushing up property prices across prime areas of Lagos.

While the CBN has outlined plans to unlock dormant assets tied to property and land, concrete steps to enforce pricing standards or require clear buyer disclosure are still being developed.

Read also:┬ĀReal estate professionals tasked on trust, global standards at NIESV Lagos summit

Impact on middle class

The consequences of this skewed market hit LagosŌĆÖs already burdened middle class the hardest. For many young professionals earning between N800,000 and N1.5 million a month, owning a home in prime Lagos remains a distant dream. Apartments in Lekki, Ikoyi, or Victoria Island are priced well above what local incomes can support. Mortgage options are limited, interest rates are high, and savings rarely cover the down payment needed. As a result, most professionals keep renting, delaying home ownership year after year.

A 31-year-old software engineer described saving diligently for five years, only to find that a modest two-bedroom apartment still costs tens of millions of naira. His experience reflects a growing sentiment among middle-income earners that property ownership is unattainable without external funding or connections.

If this imbalance continues, Lagos could become a city where homeownership is reserved for those with foreign earnings, political ties, or speculative wealthŌĆöleaving productive citizens locked out of long-term stability.

Mid-income housing remains an untapped segment with growing demand and low supply. Structured rent-to-own schemes and joint-development partnerships could attract credible buyers and generate steady returns.

Reforms should target affordable mortgage financing, enforce property taxes on under-utilised assets, and incentivise developers to build for actual local demand rather than speculative value.

Balanced intervention now could stabilise the market and restore faith that hard work, not privilege, can still buy a home in Lagos.