Chairman of Lafarge Africa Plc, Bolaji Balogun, had seen the future through the flames when he told Bloomberg in an interview that the company debt would reduce drastically.

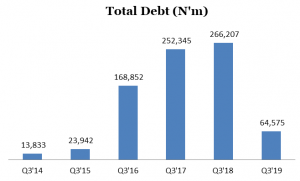

The prognosticator knew he had strategies awaiting execution. And the plan has been meticulously executed.┬ĀThe second largest producer of the building material has recorded a marked improvement in leverage ratio.

The combination of a reduction in financial leverage and costs reduction helped the company revert to the path of profitability, which means shareholders will be rewarded in form of share appreciation and bumper dividend. ┬Ā

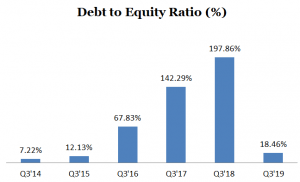

For instance, debt to equity ratio, a leverage ratio that measures the proportion of debt in the capital structure of a firm reduced to 18.67 percent in September 2019, which is far lower than the 60 percent and 70 percent company expectation.

This means investors own N0.813 of every Naira of company assets while creditor own N0.186 on the dollar.

The debt to equity ratio is a financial, liquidity ratio that compares a companyŌĆÖs total debt to total equity. It shows the percentage of company financing that comes from creditors and investors.

A higher debt to equity ratio indicates that more creditor financing (bank loans) is used than investor financing (shareholders).

The chart shows the ratio was as high as 142.29 percent in 2016, when the cement maker suffered a foreign exchange loss due to dollar based debt of its subsidiary, United Cement Company of Nigeria (Unicem).

That year, a lot of companies suffered huge foreign exchange losses as the Central Bank of Nigeria (CBN) abruptly changed the exchange regime, while a precipitous drop in crude oil price of mid 2014 stoked a severe dollar scarcity that tipped the county in its first recession in 25 year.

Read also:┬ĀLafarge Africa relaunches ŌĆśElephant SupasetŌĆÖ cement in Nigeria

Lafarge Africa PlcŌĆÖs operating profit can cover interest expense as its times coverage ratio stood at 2.14 times, which means earnings before interest and tax is 2.14 times.┬Ā

Analysts attribute the impressive performance of the company to the divestment in a subsidiary, a strategic decision they say added impetus to shareholdersŌĆÖ value.

In June, Lafarge Africa had sold its South African operations to┬ĀCaricement B.V, an indirect subsidiary of┬ĀLafarge Holcim Limited, for $317 million to pay-off a related-party loan, amounting to $293 million.

┬ĀThe company said the sale will enable it focus more on its Nigeria operations, as competition with peer rivals such as Dangote Cement and Cement Company of Northern Nigeria (CCNN) heightens.

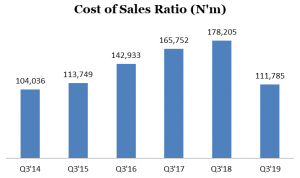

Lafarge Africa decision to diversify its energy sources has bear fruit as its total cost of production has fallen, which further added strength to margins.

Hitherto, the company used gas to power plant at its factories, but it now uses coal, a cheaper source of energy.

It has substituted locally sourced coal for imported which was relatively expensive and susceptible to foreign exchange risk.

Total cost of sales otherwise known as input costs dipped by 37.27 percent to N111.78 billion in September 2019 from N178.20 billion as at September 2018.

Cost of sales ratio fell to 68.56 percent in the period under review from 76.06 the previous year; this means the cement maker is spending less on input cost to produce each unit of product.

┬Ā

A glimpse at the chat shows cost of sales was 88.75 percent in 2016, when attacks on oil and gas infrastructure by the Niger Delta militants and currency devaluation increased the cost of gas.

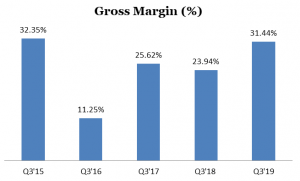

Lafarge Africa uses its materials and labour to produce and sell products profitably, as gross profit margin increased to 31.44 percent in September 2019 from 23.94 percent as at September 2018.

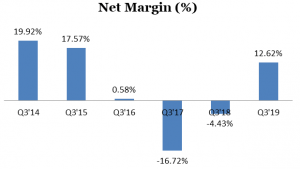

It is able to turn each Naira invested in sales into higher profit as net profit margin increased to 12.62 percent in the period under review against a negative figure of (4.42percent).

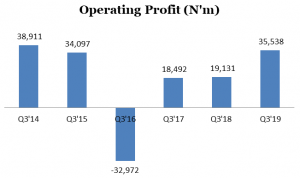

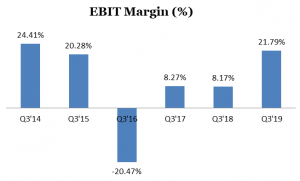

Operating profit margin, another measure of efficiency improved to 21.97 percent in the period under review from 8.17 percent as at September 2018.

BusinessDay calculation shows Lafarge Africa recorded the fastest margin expansion among peer rivals, which validates management and board of directorsŌĆÖ focus and market penetration strategies.

┬Ā

The cement maker has embarked on an aggressive expansion plans with a view to taking advantage of the Nigerian market that is beset by huge infrastructure deficit.

Lafarge Africa bought a plant in Calabar, in south eastern Nigeria, that can produce 5 million tons of cement a year and is also investing in its South African operation as it seeks to increase capacity to 17.5million tons from 14 million tons across the continent.

┬Ā

Federal Government proposed capital expenditure spending is expected to accelerate construction activities and add impetus the demand for cement, a boon for Lafarge Africa and its peers in the industrial building industry will benefit from

The Minister of Finance, Budget and National Planning, Zainab Ahmed,┬Ā┬Āsaid her ministry plans to release up to N900 billion for capital expenditure by December.

Further analysis of the financial statement of cement maker shows it posted a profit after tax of N20.57 billion as at September 2019 from a loss of N10.37 billion the previous year.

┬Ā

Its net cash from operating activities was up 64.34 percent to N47.58 billion┬Ā┬Āin the period under review from N28.95 billion the previous year. This means it has the financial strength to pay dividend, settle its debt and fund future expansion plans.

Amid a stock market rout that forced investors to dump shares of bellwether firms, Lafarge AfricaŌĆÖs shares have been growing since last year as it has a year to date of 14.86 percent. That outperforms the Nigerian Stock Exchange and All Share Index -14.12 percent.┬Ā

┬Ā

┬Ā

┬Ā

┬Ā

┬Ā

┬Ā

┬Ā

┬Ā