The financial services sector in Nigeria, long perceived as conservative and slow to innovate, is now turning to artificial intelligence (AI) to reinvent its operating model and cut costs.

According to the Talent Management Report 3.0 by Phillips Consulting, the integration of AI and automation in traditional banks is helping institutions reduce operating expenses by as much as 22 percent.

The report finds that Nigerian banks are increasingly deploying AI in recruitment, fraud detection, compliance automation, and customer service.

ŌĆ£Banks are piloting AI in recruitment, fraud detection, and compliance automation, but HR applications lag behind customer-facing innovations,ŌĆØ the report said.

While customer engagement and security have historically been the primary drivers of digital investment, HR functions are catching upŌĆöalbeit slowly.

Read also:┬ĀReps probe commercial banks over incessant, arbitrary charges

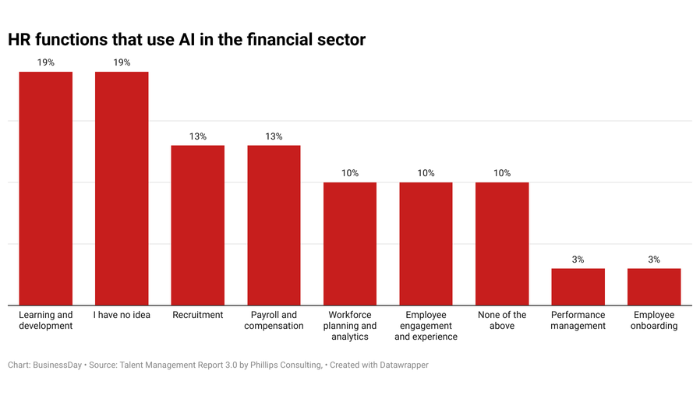

ŌĆ£Today, 34 percent of financial institutions use AI in recruitment, while 19 percent have introduced AI-enabled learning and development programmes to scale employee upskilling,ŌĆØ it said.

The report stated that institutions such as Zenith Bank and Fidelity Bank are already reaping measurable efficiency gains.

ŌĆ£Zenith Bank has automated its recruitment process, reducing time-to-hire and administrative overheads, while Fidelity BankŌĆÖs HR chatbot now handles routine employee queries, improving engagement and cutting response times significantly.ŌĆØ

The report underscores that AI-driven automation is translating directly into operational savings.

A Marsh & McLennan (2019) benchmark cited in the study suggests that traditional banks could cut up to 22 percent of their total costs through AI adoption, a figure that aligns with the early results emerging from Nigerian institutions integrating digital systems into core HR operations.

From manual processes to predictive models

The transformation is not limited to cost optimisation. Fintechs are leading the charge, using predictive workforce models to anticipate staffing needs, identify skill gaps, and allocate resources efficiently. Traditional banks are beginning to follow suit, deploying AI-based analytics to inform strategic workforce planning and enhance productivity.

By leveraging machine learning to identify hiring bottlenecks and predict attrition, financial institutions can now anticipate talent shortages before they impact performance.

These predictive tools are also helping HR departments optimise recruitment spending and refine retention strategies, effectively reducing turnover costs while improving hiring accuracy.

The report reveals that 37 percent of banks use AI primarily for operational efficiency, 32 percent for data-driven decision-making, and 11 percent for cost optimisation.

This underscores that AIŌĆÖs current role is largely backend-focused, aimed at streamlining processes rather than driving comprehensive workforce transformation.

Read also:┬ĀBig banks incur N442bn in AMCON expenses amid falling profit

AI is restructuring the workforce, not replacing It

While automation is displacing some traditional roles, especially those involving repetitive tasks, the report stresses that AI is reshaping jobs, not erasing them.

The International Labour Organisation (ILO) estimates that up to 40 percent of tasks in NigeriaŌĆÖs financial services industry could be automated by 2030, particularly those performed by bank tellers, back-office clerks, and call centre agents.

However, this transformation is simultaneously creating new opportunities.

The Nigerian Communications Commission (NCC) reports a 35 percent annual increase in demand for roles such as data scientists, cybersecurity analysts, AI specialists, and customer experience managers, positions that did not exist in traditional banking structures a decade ago.

The Talent Management Report captures this duality clearly: while 24 percent of financial institutions are automating or phasing out roles, 21 percent report an increased demand for new digital skills, and 18 percent are actively redesigning jobs to integrate AI-driven responsibilities.

Only 5 percent cite downsising as a direct consequence of AI, suggesting that automation is being used more for redeployment than retrenchment.

Bridging the digital skills gap

Despite the optimism surrounding AI adoption, the report warns that a widening digital skills gap could undermine progress. Fewer than 12 percent of employees in the financial sector possess proficiency in AI, analytics, or cybersecurity.

Meanwhile, the talent report added that only 27 percent have adequate digital skills to function effectively in AI-enhanced workplaces.

This gap is especially pronounced among mid-career professionals those responsible for managing AI systems and ensuring their ethical deployment.

Read also:┬ĀCBN gives banks 48 hours to refund failed ATM transactions

As the report explains, ŌĆ£Mid-career professionals, who are essential for managing and optimising AI applications in talent management, often lack specialised training in data analytics, AI ethics, and robotic process automation.ŌĆØ

To address this, banks are prioritising internal retraining over external hiring. About 28 percent of institutions now provide AI-related training for employeesŌĆÖ current roles, while 23 percent are retraining staff for new positions. Another 15 percent are redesigning roles to include AI responsibilities, the report said .

The BankersŌĆÖ Committee of Nigeria has called for a national reskilling programme to prepare the workforce for automationŌĆÖs demands.

Without this, the report warns, ŌĆ£AI adoption could unintentionally widen the capability gap it aims to close.ŌĆØ

The path to full AI integration is not without obstacles. Legacy infrastructure continues to impede transformation, with only 39 percent of Nigerian banks having adopted scalable cloud solutions.

The Nigerian Fintech Cloud Adoption White Paper (2023), cited in the report, points to regulatory bottlenecks, data security concerns, and hierarchical management structures as key barriers slowing progress.

Cultural resistance also plays a role. ŌĆ£More than 60 percent of financial sector employees express anxiety over job security in the wake of AI deployment.ŌĆØ

This anxiety, the report finds, often stems from low AI literacy and poor internal communication. ŌĆ£Leadership familiarity with AI is low, slowing adoption at the top and across teams,ŌĆØ it warns.

Still, the benefits are becoming increasingly clear. In recruitment, the talent report disclosed that 26 percent of banks report faster candidate screening times and improved job-candidate matching, while 19 percent note better hiring accuracy through AI-driven assessments.

Meanwhile, in performance management, institutions are beginning to use AI to reduce bias, automate appraisals, and deliver real-time feedback

However, developmental applications remain underutilised. Only 3 percent of organisations use AI to recommend training or coaching opportunities, suggesting that while efficiency is improving, talent growth and engagement are lagging.

The report noted that ŌĆ£AI is primarily seen as a backend enabler, not a strategic HR asset,ŌĆØ a sentiment echoed by HR executives who believe AIŌĆÖs full value will emerge only when integrated into learning, leadership, and performance ecosystems.

Read also:┬Ā7 Nigerian banks hold N257.1bn equity stake in small businesses

Changing perceptions: From fear to opportunity

The report stated that while 33 percent of financial sector workers believe AI will boost productivity and create new opportunities, 56 percent express concern or uncertainty about the future.

ŌĆ£Nearly 28 percent fear job losses, underscoring the urgent need for transparent change management and clear communication strategies.ŌĆØ

Yet optimism persists. The report shows that 80 percent of employees in the financial sector believe AI can make HR processes fairer and more efficient, particularly in recruitment and learning.

This suggests that with proper leadership engagement and continuous education, banks can shift the narrative from fear to empowerment.

Despite widespread awareness, full-scale AI integration in HR remains limited. ŌĆ£Only 9 percent of institutions report organisation-wide adoption, compared to 21 percent at the strategic stage and 24 percent still in exploration.ŌĆØ

Furthermore, 39 percent of banks describe their AI investments as minimal, reflecting a cautious, risk-averse approach to innovation.

ŌĆ£The financial services sector is caught between ambition and execution,ŌĆØ the report said. ŌĆ£Many banks recognise AIŌĆÖs transformative potential but lack the infrastructure, skills, and regulatory clarity to scale pilot initiatives into sustainable models.ŌĆØ

From cost-cutting to value creation

Ultimately, the Talent Management Report 3.0 frames AI as both a cost-saving mechanism and a strategic growth enabler.

Beyond operational efficiency, it presents AI as a tool for strategic workforce planning, allowing banks to align talent pipelines with future needs and reduce long-term overhead.

By 2030, the report projects, AI could help financial services globally save over $1 trillion, with NigeriaŌĆÖs banks poised to contribute significantly to that figure if they continue on their current trajectory.

Read also:┬ĀBanksŌĆÖ dividend declarations spur optimism in stocks

However, realising this potential will require a mindset shift from viewing AI as a technology initiative to treating it as a people strategy.

As the report said, ŌĆ£AI wonŌĆÖt replace talent; it will redefine it. Adaptability will become the new currency of talent.ŌĆØ

For Nigerian banks, the next phase of AI adoption will hinge on balancing efficiency with empathy. Investment in AI literacy, ethical training, and data transparency must accompany automation if institutions are to sustain trust and inclusion in the digital era.

ŌĆ£Reimagine your workforce strategy. Start small, build readiness, embed agility, and scale what works. Focus on people-first transformation,ŌĆØ the report said