Across Nigeria, many state governments are taking on record levels of debt to finance growth. Lagos leads that charge, but its rapid expansion is raising concerns about sustainability.

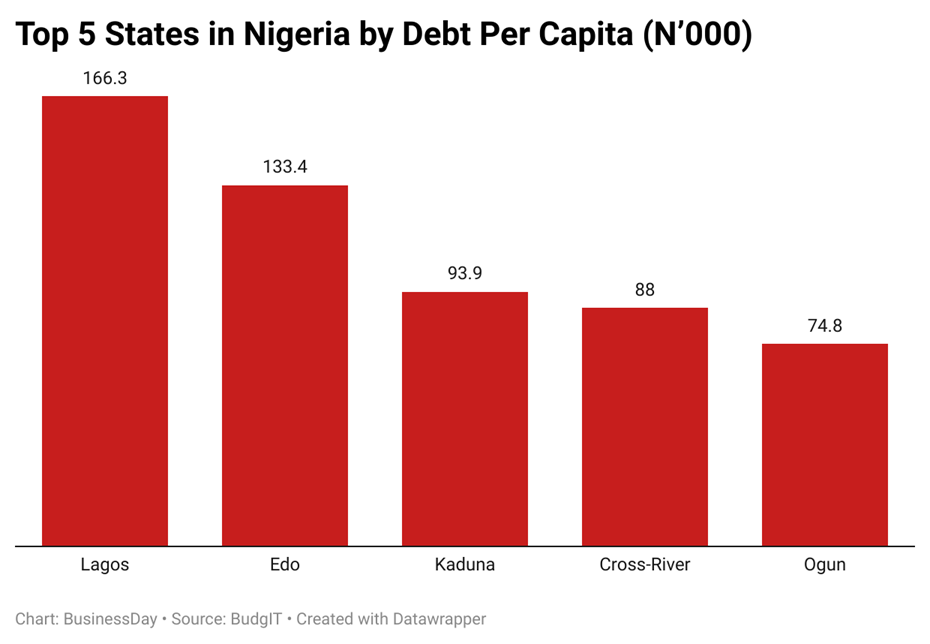

New data from BudgIT’s State of States 2025 report show that Lagos and Edo have the highest debt per capita, the average debt burden each citizen would bear if a state’s total debt were divided equally among its population. Both exceed N100,000, compared with the national average of N41,766.

In Lagos, the figures show a mixed picture. The state’s Internally Generated Revenue (IGR) rose to N1.26 trillion in 2024, up 50 percent from the previous year, yet total debt climbed to N2.7 trillion, making it the most indebted state in Nigeria.

From Cross River to Kaduna and Ekiti, states are borrowing heavily to fund infrastructure projects that often deliver slower economic returns. The trend has reignited debate about whether Nigeria’s subnational governments are financing development or mortgaging their future.

How the ranking works

BudgIT’s evaluation offers a comprehensive snapshot of how Nigerian states manage their finances amid rising fiscal pressure. The organisation assessed 35 states, analysing how effectively they raise and utilise public funds. Drawing on audited state accounts, as well as data from the Debt Management Office and the National Bureau of Statistics, BudgIT evaluated each state’s financial capacity and discipline.

The review focused on key indicators such as the share of spending funded by internally generated revenue, the pace of revenue growth, the ability to finance budgets without new borrowing, debt sustainability, and how efficiently states balance capital investments with recurrent costs. These metrics were then combined to show which states are fiscally stable and which are drifting deeper into debt dependency.

According to BudgIT, Rivers State was excluded from the 2025 analysis due to the removal of elected officers under a state of emergency. The state also failed to submit an audited financial statement by the time of final data compilation, making it ineligible for assessment.

The hidden price tag of growth

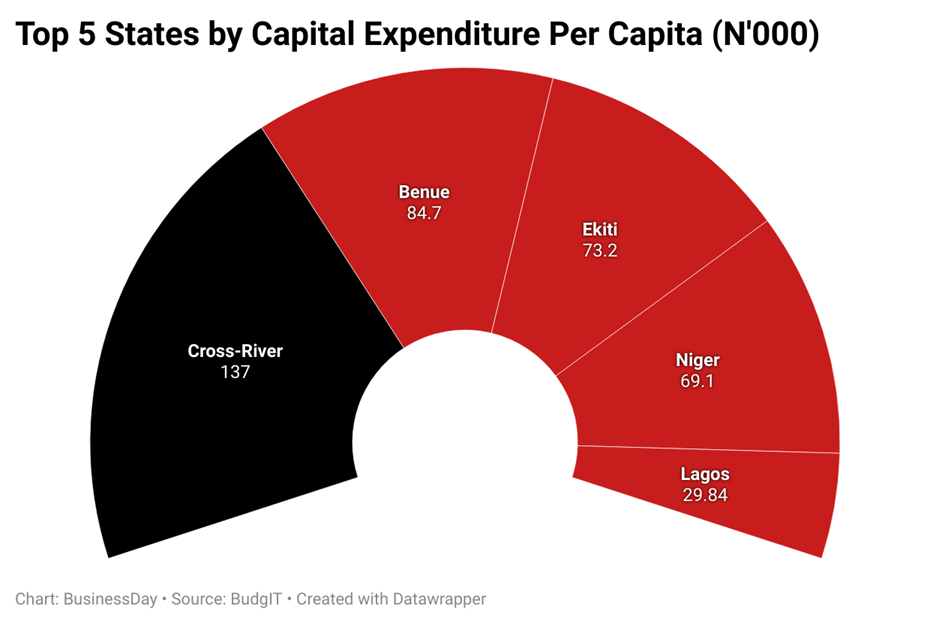

The report shows that total capital spending by states rose sharply to N7.63 trillion in 2024, representing an 88 percent increase from the previous year. Lagos alone accounted for N1.1 trillion, invested in projects such as the Blue Line Rail Phase 2, new bridges, and road networks across Yaba, Oyingbo, and FESTAC. Cross River recorded the highest capital expenditure per capita at N137,000, followed by Benue, Ekiti, and Niger.

BudgIT’s data also show Lagos as the least dependent on federal allocation, with taxation providing more than 80 percent of its total revenue. PAYE and withholding taxes form the backbone of its finances, enabling the state to surpass the N1 trillion mark for the first time. In contrast, many states remain heavily reliant on Abuja’s monthly allocations, leaving them vulnerable to oil price shocks and delays in disbursement.

Despite this strong revenue performance, Lagos’s debt profile is flashing red. Foreign loans account for about 66 percent of its total debt, leaving the state highly exposed to exchange rate volatility. The sharp depreciation of the naira in 2024 has inflated the naira value of these loans even though the dollar obligations have declined in nominal terms.

Debt per citizen: a new inequality

Nigeria’s subnational debt, now above N10.57 trillion, becomes even more revealing when viewed per citizen. Each resident of Lagos effectively carries a state debt of N166,253, while a citizen of Jigawa owes just N5,057. This 33-fold difference illustrates the growing fiscal inequality that defines the federation.

Twelve states now exceed the national debt-per-capita average of N41,766, with Lagos, Edo, and Kaduna among the highest. Analysts warn that while some borrowing supports infrastructure, much of it still goes into paying salaries, servicing old debts, or funding administrative overheads rather than productivity-enhancing projects.

In Lagos, the N166,000 debt per capita is 5.6 times higher than its capital expenditure per person, estimated at N29,837. This suggests that most borrowing maintains existing obligations rather than new development. Ekiti faces a similar challenge, with nearly 79 percent of its debt denominated in foreign currency, limiting its fiscal space for capital investment.

Cross River has channelled a larger share of its loans into development, recording the highest capital spending per capita nationwide. Yet its revenues have not kept pace with obligations, raising doubts about long-term sustainability.

Growth at a cost

The broader fiscal picture shows a widening gulf between states with strong internal revenue and those struggling to stay solvent. Lagos leads in both development and debt, a paradox that captures Nigeria’s central fiscal dilemma: whether borrowing is driving progress or mortgaging the future.

“Debt isn’t bad on itself,” said Faruq Quadri, an economist. “But it must build assets that raise income and productivity. If borrowed money ends up paying salaries or servicing old loans, we are simply passing the bill to our children.”

Biodun Adedipe, a development economist and founder of B. Adedipe Associates Limited, shared a similar view. “Debt is crucial for infrastructure development,” he explained. “It is not solely about borrowing; it is about how we allocate the borrowed funds.” His argument highlights that borrowing can stimulate growth if it finances productive assets rather than recurrent obligations.

The floating of the naira and sustained inflation have worsened repayment costs, while debt service and overheads now consume more than 70 percent of spending in several states, leaving little room for education, healthcare, or infrastructure renewal.

Paul Alaje, chief economist at SPM Professionals, warned that Nigeria’s growing subnational debt could worsen if the naira continues to weaken. “The more you devalue your currency, the more you owe; your debt becomes intimidating over the years,” he said.

“Between now and 2027, our national debt could surpass N200 trillion if fiscal discipline does not improve.” His remark reflects the increasing concern that exchange rate movements could amplify repayment risks for states with large external obligations.

Implications for investors

For investors, Lagos remains both a model and a warning. Its diversified economy and strong tax base make it attractive for partnerships, yet its heavy reliance on foreign loans and growing interest costs suggest a fragile balance between growth and sustainability.

Smaller states such as Jigawa and Niger, with lower borrowing and better expenditure control, offer more stable prospects even if their economies are modest. Others, including Benue and Anambra, have begun tightening their fiscal policies, improving revenue collection, and reducing waste to prevent future debt distress. The challenge for all subnationals is to sustain growth without overleveraging public finances.

The bottom line

Debt can fuel development, but only when it creates assets that outlast the repayment period. Lagos’s skyline continues to rise, financed by borrowed billions, but sustaining that growth depends on whether today’s debt translates into tomorrow’s prosperity.

Nigeria’s debt divide is widening. For millions of citizens, the cost of progress is already visible not only in higher taxes or delayed public services but also in the growing weight of obligations they never signed for.