Nigeria’s expanding tax net and new digital compliance systems have made understanding tax obligations crucial for entrepreneurs, particularly with the new tax reform acts.

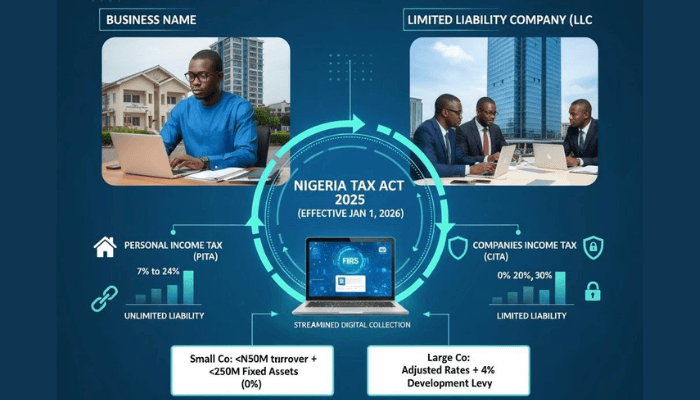

Business names, which include sole proprietorships and partnerships, are treated as a single legal entity where the owner assumes full responsibility for operations and liabilities, meaning personal assets may be used to settle business debts in the event of insolvency.

Limited Liability Companies (LLC), on the other hand, are separate legal entities distinct from their owners, with liability limited to the equity contributed, protecting personal assets in the event of liquidation.

Under the existing tax framework, business owners are treated as individuals, and profits are taxed under the Personal Income Tax Act (PITA) through a self-assessment system, with returns filed to the relevant State Internal Revenue Service (SIRS) for the preceding year, due by March 31.

Limited liability companies, however, are governed by the Companies Income Tax Act (CITA) and file returns with the Federal Inland Revenue Service (FIRS), with existing companies required to file within six months of the accounting year-end, and newly incorporated companies filing within 18 months of incorporation or six months after their first accounting period, whichever comes first. These filing provisions remain largely unchanged under the new tax reforms.

According to Olamide Sulaiman, Tax Consultant at Forvis Mazars, transitioning from a business name to an LLC may be financially prudent under certain conditions, including tax efficiency and access to funding and corporate contracts.

Under the Nigeria Tax Administration Act (NTAA), small companies with an annual turnover of no more than N100 million and total fixed assets under N250 million are taxed at zero percent. In contrast, a business owner with similar revenue is subject to personal income tax between zero and 25 percent, with only the first N800,000 exempted, making incorporation a strategic tool for tax optimization.

Read also: Here’s how Nigeria’s tax reform affects everyday investments

Sulaiman also notes that incorporation improves access to funding and contracts. Banks, investors, and government institutions often prefer dealing with registered entities, which ensures continuity and protects investor equity in the event of a shareholder’s death, a guarantee not available under a business name. Unregistered businesses may face administrative penalties when bidding for contracts, making incorporation a practical consideration for growth and enhanced business credibility.

A key operational advantage is the separation of personal and business income. Business owners often struggle to distinguish private funds, such as loans, from business income, and may face excessive tax assessments or disallowed deductions due to documentation issues and the fact that the two entities are legally one. Incorporation removes this ambiguity, as shareholders are assessed individually while the company is subject to corporate income tax, and in some cases, an LLC may incur no tax due to its classification and available reliefs.

Protection of personal assets is another critical consideration, since operating under a business name exposes owners to business risks, debts, and tax liabilities. Incorporation shields personal property, as the entity is treated separately from its shareholders, offering essential security during tax audits or investigations. Small companies also enjoy specific compliance reliefs and incentives, including exemptions from corporate income tax and value-added tax obligations. They receive relief from withholding tax deductions on supplier invoices under certain conditions and can receive full payment on invoices without deductions, significantly improving liquidity and working capital.

Recent reforms have also reshaped taxation by reclassifying companies as either small, taxed at zero percent, or other companies, taxed at 30 percent, replacing the previous three-tiered structure. Capital gains tax, previously set at a flat 10 percent, is now integrated into the income tax framework.

For business owners, chargeable gains are now taxed at the progressive PIT rates (0–25 percent), while larger companies are taxed at 30 percent.

Reliefs available to business owners include exemptions for certain compensations, disposal of owner-occupied houses or land, and disposal of personal chattels below defined thresholds. Large companies or members of multinational enterprises may be liable for a top-up tax of 15 percent, a provision that does not apply to business owners. A consolidated development levy of four percent of assessable profit applies to larger companies but not small businesses.

While there has been debate over whether business owners should convert to a limited liability company, Sulaiman emphasizes that the decision should be made on a case-by-case basis. The reforms offer incentives for small businesses but also introduce new compliance obligations that require careful consideration. Entrepreneurs are strongly advised to seek guidance from qualified tax consultants to ensure compliance and make decisions that optimize benefits for long-term growth.