Six months ago, an article titled “Why Nigeria’s bold budget projections could backfire” was published by BusinessDay. It flagged a widening gap between fiscal optimism and economic fundamentals. That gap is now harder to ignore.

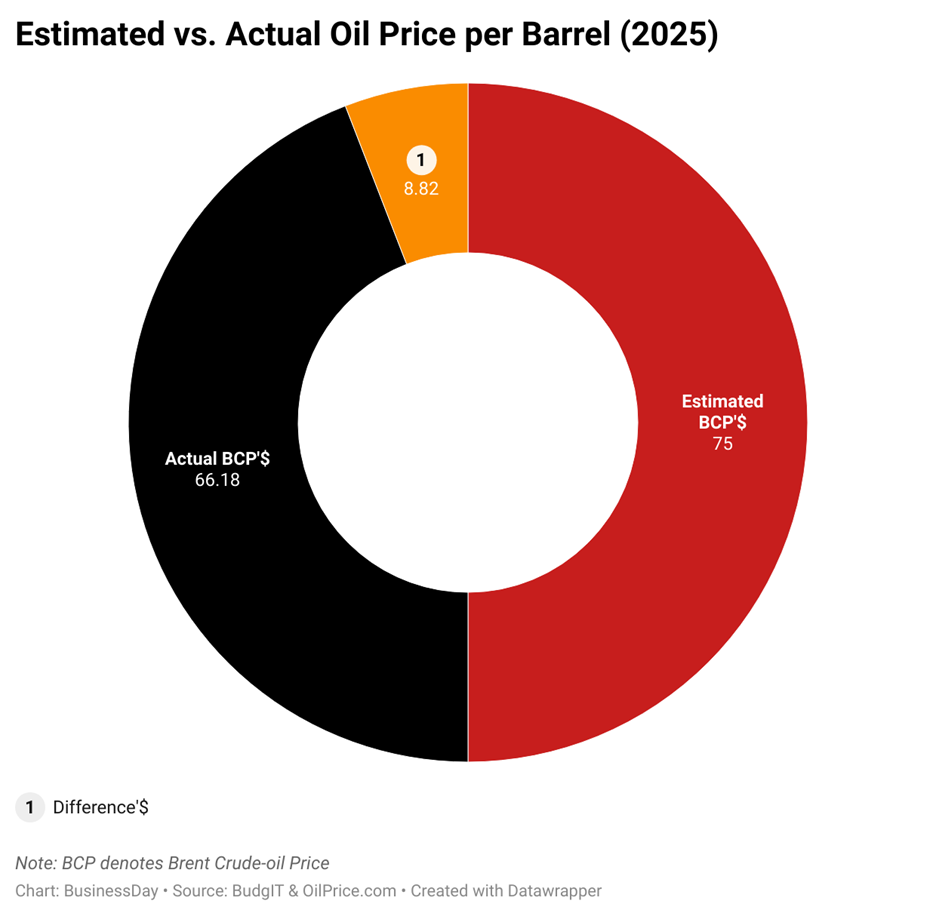

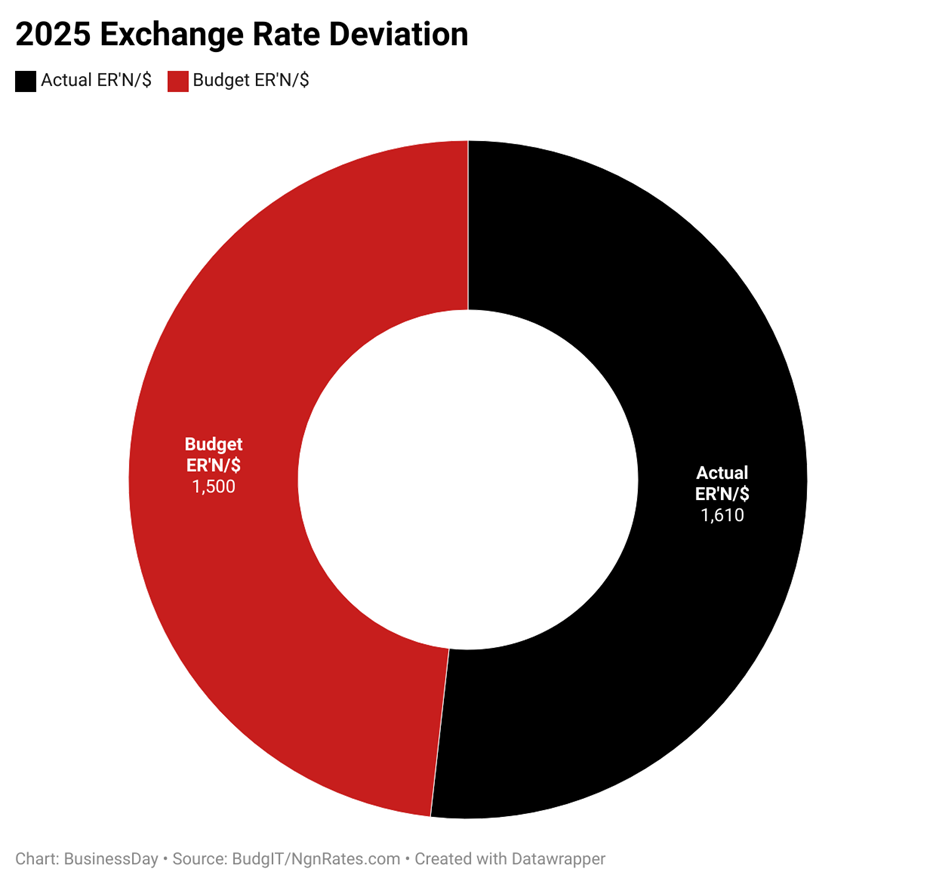

Nigeria’s Medium-Term Expenditure Framework (MTEF) for 2025–2027 rests on two key assumptions: a crude oil benchmark of $75 per barrel and an exchange rate of ₦1,400 to the dollar. While these targets project confidence, analysts warn they sit on shaky ground.

Independent projections from BusinessDay economists based on historical trends and macroeconomic modeling, suggest a more conservative baseline: oil priced at $60–$65 per barrel and an exchange rate closer to ₦1,498.

When the budget was finalized, the exchange rate was eventually adjusted to ₦1,500 per dollar, reflecting a more realistic stance in light of market movements.

Why does this matter? Because Nigeria’s fiscal stability still hinges largely on oil, a volatile commodity beyond its control. As a small, open economy, Nigeria is exposed to global oil price swings without the leverage to influence them.

The 2025 budget, pegged at ₦54.99 trillion, rests heavily on the assumption that oil prices will remain buoyant. But Brent crude has recently slipped to around $66.18, almost $9 below the benchmark, according to data from OilPrice.com. The gap between projections and reality is growing.

This fall in prices stems from global worries: a potential economic slowdown, revived trade tensions, and political uncertainty in major economies. For Nigeria, the fiscal consequences are immediate.

With expected revenues of ₦36.35 trillion based on $75 per barrel, lower prices point to a wider fiscal deficit and higher borrowing. Already, debt servicing consumes a large portion of government income.

Naira under pressure

The naira, meanwhile, is feeling the strain. With oil accounting for over 90 percent of Nigeria’s foreign exchange inflows, any drop in oil revenue reduces dollar supply, putting pressure on the local currency.

According to Bloomberg, Goldman Sachs economist Andrew Matheny explained that “the natural policy response to lower oil prices is a depreciation of the naira, as this boosts oil revenues in naira terms.”

That dynamic is already playing out. The naira has lost about 5 percent against the dollar in April, trading at approximately ₦1,610 on the parallel market.

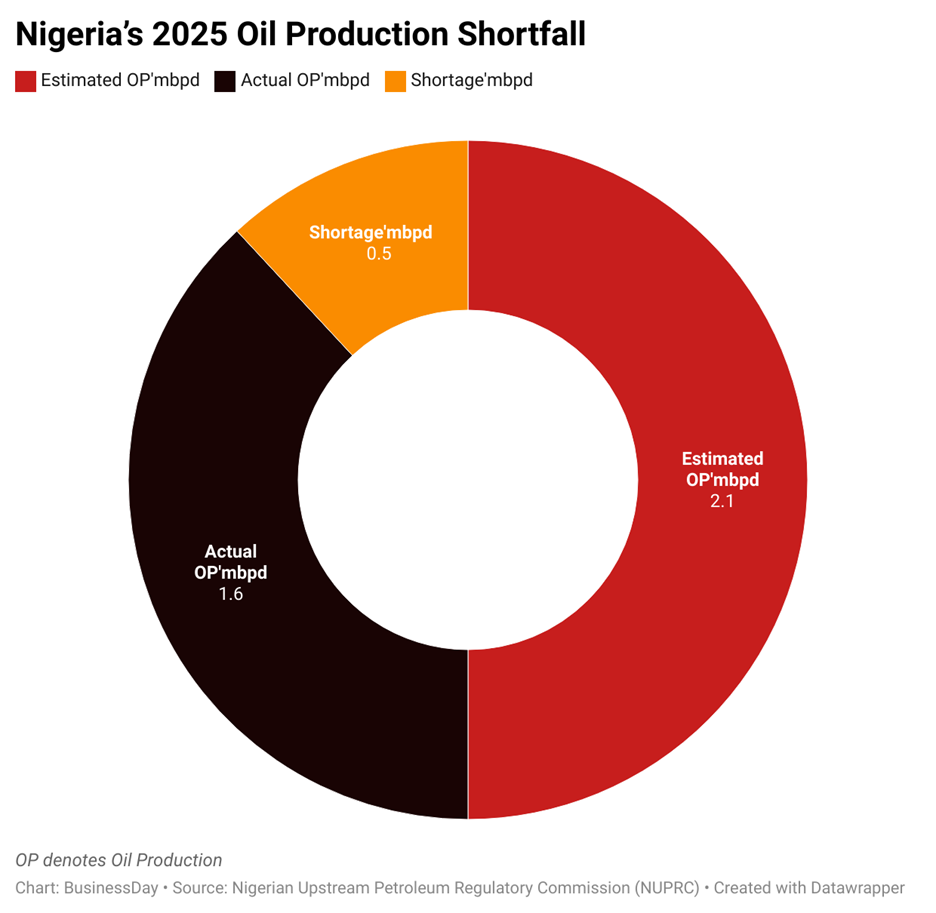

Oil production, meanwhile, stood at just 1.6 million barrels per day in March, well below the 2.1 million daily target set in the budget, according to the Nigerian Upstream Petroleum Regulatory Commission (NUPRC).

This marks a decrease from February 2025, when production was 1.68 million barrels per day

Matheny described the government’s production assumptions as “already optimistic,” warning that “risks are tilted toward fiscal slippage.”

Local warnings, global risks

International developments aren’t helping. In the United States, rising protectionist sentiment has put tariff threats back in the spotlight. President Donald Trump recently announced a 90-day pause on tariffs for several countries excluding China.

The move came after market volatility wiped trillions off U.S. equity markets and sent the dollar higher. A stronger dollar typically drags oil prices lower, more bad news for Nigeria. Then, just yesterday, Trump followed up with plans to cut tariffs on Chinese goods, which could further alter global trade dynamics.

At home, officials are acknowledging the risks. Farouk Ahmed, ceo of the Nigerian Midstream and Downstream Petroleum Regulatory Authority, cautioned earlier this week:

“If we lose the price of crude by $10, you can see the negative impact on our economy, our national reserves, and the strength of our naira.”

The price of overconfidence

This is where budgetary optimism confronts economic reality. Assumptions that once appeared bold now risk becoming liabilities.

In a conversation with BusinessDay last week, a financial economist from Johns Hopkins University outlined two corrective steps: First, ramp up oil production to cushion lower prices. If volume rises as prices fall, some fiscal shortfall could be offset.

Second, curb non-productive public spending. “Costs that don’t stimulate economic activity such as National Assembly perks, State House travel, and excessive maintenance of the Presidential Villa should be reviewed,” the economist said.

“Cutting such costs can help restore public trust, especially in tough times.”

However, the track record is mixed. Nigerian governments have often responded to budget gaps not by trimming excesses, but by requesting supplementary budgets that raise spending without boosting revenue.

Bottom line

The government’s next move will be decisive. A timely revision of its assumptions, paired with spending discipline, could help Nigeria weather the storm. But doubling down on hope may only deepen its fiscal troubles.